As a founding member of the Ultra Ethernet Consortium, which has the express purpose of making Ethernet as good for AI and HPC clusters as InfiniBand but with the scalability and familiarity of Ethernet, Arista Networks wants to benefit mightily from the AI wave that is coming to enterprise datacenters the world over. And it also wants to expand its share of network wallet among its two largest customers – Microsoft and Meta Platforms – and use those marquee customers as a way to open doors and close deals at thousands of enterprise shops that will want to mimic whatever Microsoft and Meta Platforms do when it comes to AI.

It doesn’t hurt that Broadcom is fired up with its AI-tuned “Jericho3-AI” switch ASIC and that Microsoft and Meta Platforms and Broadcom are also founder members of the UEC.

Things are lined up nicely for Arista to benefit mightily by taking AI networking mainstream, essentially pitting Broadcom ASICs and its own EOS network operating system stack against Cisco Systems’ Silicon One ASICs and its own switches as well as those that the hyperscalers and cloud builders might make based on those switch chips. Oh, and both are gunning for Nvidia’s InfiniBand, which has the lion’s share of compute node interconnect on clusters that underpin GenAI and other kinds of machine learning. Even InfiniBand has to have a backup plan with its Spectrum-X combination of 400 Gb/sec Ethernet and BlueField DPUs.

Jensen Huang, Nvidia’s co-founder and chief executive officer, has quipped that InfiniBand networking represents about 20 percent of the cost of an AI cluster and boosts performance by about 20 percent over stock Ethernet switching (meaning not Spectrum-X), so InfiniBand is effectively free. But not so fast on that math. InfiniBand might pay for itself, and Spectrum-X might shoot the gap between stock Ethernet and InfiniBand for AI networks, but it certainly is not free. You still need to come up with the money to buy InfiniBand to squeeze that extra performance out of the Nvidia GPUs in a cluster. And it can be a lot of money.

How much? Well, Nvidia’s financials give us a hint. In the trailing twelve months ended in January, our model shows Nvidia having $25.97 billion in datacenter compute sales (that’s GPUs, a tiny amount of CPUs, HGX and MDX GPU assemblies, and DGX servers) compared to $5.53 billion in InfiniBand sales. The Datacenter compute sales rose by 2.4X over those twelve months compared to the prior twelve months, and InfiniBand rose by 3.15X. Ethernet sales actually dropped, and we think Arista and Cisco took bites out of Nvidia’s Ethernet business among the hyperscalers and cloud builders, and maybe for the sole reason that these big companies do not like to concentrate their supply chain risk.

But it is more than that. InfiniBand needs more switches than Ethernet to scale to 10,000 or more nodes. People argue about this. Some people say InfiniBand tops out at around 11,000 nodes (or GPU devices if you have one network interface per GPU, as AI clusters do), some say it is around 40,000 nodes (or GPIU devices). Companies are contemplating building training clusters with 50,000 to 100,000 accelerators for training and keeping an eye out for 1 million devices, according to the UEC. The hyperscalers and cloud builders have been begrudgingly willing to accept a non-Ethernet network for the AI clusters, and as we have pointed out before, Microsoft was eager early on and gave InfiniBand some of the multitenancy and security features that it was missing and that are part of Ethernet. But we do not think Microsoft and Meta Platforms, or any other company operating AI at scale, wants to pay the 20 percent premium for InfiniBand when historically they have been able to have Ethernet networking for under 10 percent of the cost of the cluster.

Cutting the network costs by more than half means each AI cluster can scale further because the network savings can be plowed back into compute. This is how the HPC centers of the world have operated for years.

Given all of the prognostications about AI spending that we have seen and picked apart – here is one at this link that talks about GenAI spending in particular between 2022 and 2027, here is one that models datacenter GPU spending from 2015 through 2027, here is one that models AI and non-AI server spending based on IDC data spanning 2022 through 2027, and here is yet one more that picks apart the very ambitious forecast that AMD has been making for $400 billion in AI accelerator spending by 2027.

So when Jayshree Ullal, co-founder and chief executive officer at Arista, said on the call going over the company’s fourth quarter of 2023 financials with Wall Street analysts that it was sticking to its forecast of a mere (relatively speaking) $750 million in AI-related sales by 2025, our head tilted the way a dog’s does when it hears a high-pitched whistle. That seems kinda low given the growth in overall AI spending we see forecast out there.

Sure, for large clusters, InfiniBand can be twice as expensive as Ethernet, but it yields lower latency and therefore higher GPU utilization so long as your cluster is in the sweet spot of InfiniBand’s scale as the traditional HPC systems of the world generally are. So for the same number of clusters, you would think the networking portion will drop as companies decide they can switch to Ethernet, for which they might sacrifice some latency for the sake of saving or more scale in compute and networking.

Let’s do some math. If AI servers are going to drive $100 billion in accelerator sales, that is around $200 billion in systems sales. Add Ethernet networking for $20 billion and flash storage for another $30 billion, and networking is around 8 percent of the total AI server TAM. Against this reasonable estimate – which does not include inference running on CPUs, which will be a big part of the market – $750 million by 2025 seems small given that Arista has around a 30 percent share of datacenter switch revenues at 10 Gb/sec and higher speeds.

A lot depends, it seems, on what the UEC does and how fast it does it.

But the prognosis is good, and Ullal gave some stats to back up a more aggressive stance with AI networking should this initial anecdotal evidence prove to be a trend.

“If I look at the last year, which may be the last twelve months, it is a better indication,” Ullal explained on the call. “We have participated in a large number of AI bids. When I say large, I should say they are large AI bids, but they are a small number of customers actually – to be more clear. And in the last four out of five AI networking clusters we have participated on Ethernet versus InfiniBand, Arista has won all four of them for Ethernet, and one of them still stays on InfiniBand. So these are very high profile customers. We are pleased with this progress. But as I said before, last year was the year of trials. This is the year of pilots. And true production truly sets in on the year 2025.”

Our model, which is based on a hunch and one data point, is that Arista had maybe $235 million in AI-related networking sales in 2023, and this grew by 28.5 percent to $302 million. This year, it might hit $387 million on the way to hitting $750 million in 2025. We expect for Arista to be pleasantly surprised to a much larger upside in 2025, but it is not the only Ethernet vendor looking to capitalize on AI and a lot depends on its ASIC choices and how they evolve over time. It will be a cold day in Hell when Arista uses Cisco Silicon One ASICs, we think. But sometimes staunch competitors bury the hatchet – and not in each other’s heads – because that is smart business. We shall see.

And with that, let’s drill down into he Q4 2023 numbers for Arista.

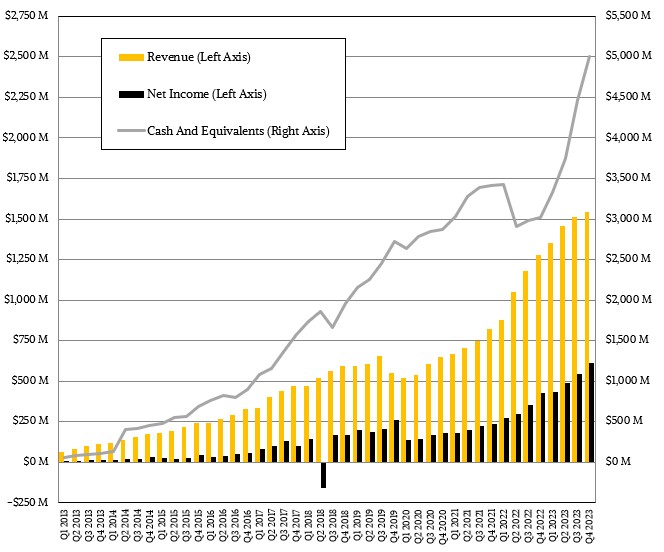

In the final quarter of the year, Arista’s product revenues rose by 19.5 percent to $1.31 billion and services revenues were up by 28.8 percent to $230.1 million.

Overall revenues rose by 20.8 percent to a record $1.54 billion. Software subscriptions came in a $31.8 million, up 38.9 percent, and software and other subscription revenues rose by 29.9 percent to $261.9 million.

Operating income for the quarter was $640 million and net income was $614 million, which is 39.8 percent of revenue. Both operating and net income grew around twice as fast as revenues, which is the kind of thing you want to see in a tech company.

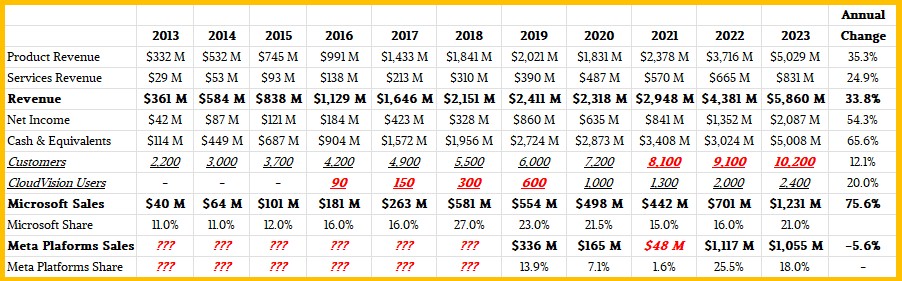

Here is a table showing all of the key metrics for Arista on an annual basis over more than a decade, including the rise of Microsoft and Meta Platforms as key customers:

Most tech companies should be evaluated on an annual rather than a quarterly cadence, this being a naturally choppy business, with weak first and third quarters, a relatively strong second quarter, and a usually big fourth quarter in the datacenter.

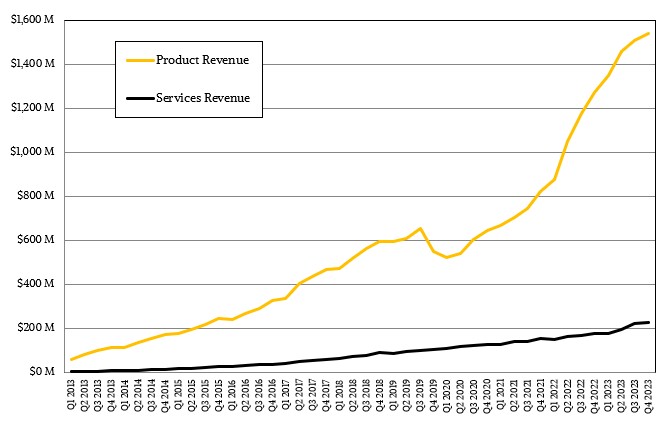

For the full year, product sales were up 35.3 percent to $5.03 billion and services revenues were up 24.9 percent to $831 million, for a total of $5.86 billion in sales, up 33.8 percent. This in an IT market that is undergoing a server recession outside of AI server spending and with hyperscalers and cloud builders having pulled back on spending in 2023 as well. The company brough $2.09 billion to the bottom line in 2023, up 54.3 percent and representing 35.6 percent of revenues. This is a very healthy net income to revenue ratio. Arista ended the year with just over $5 billion in cash, giving it ample room to make strategic AI and other acquisitions as it deems necessary – or even create its own ASICs should it come to that someday. We think Arista ended the year with over 10,000 customers and we know it has more than 2,400 customers for its CloudVision telemetry software.

Arista only tells us the details about its largest customers – that that account for more than 10 percent of revenues in any given period – at the end of each year, so we can now talk about that. Microsoft and Meta Platforms, who are pushing hard for Ethernet to evolve through the UEC, accounted for 21 percent and 18 percent of 2023 sales, respectively. That works out to $1.23 billion for Microsoft, up 75.6 percent compared to last year, and $1.06 billion for Meta Platforms, actually down 5.6 percent.

We have no idea how much of the spending at either company was for AI clusters or generic datacenter interconnects, but clearly most of the spending was not for AI or Arista would have said something about that because it is material to the business and the US Securities and Exchange Commission doesn’t like material things not being reported to shareholders. (Which is also why customers who account for more than 10 percent of revenues also have to be disclosed. It’s an SEC rule, not benevolence.)

As impressive as the sales to Microsoft and Meta Platforms were for Arista, it is the growth of sales to regular enterprises – mostly for the datacenter but increasingly, we think, for companion campus and edge networks – that is giving Arista a new vector on which to grow.

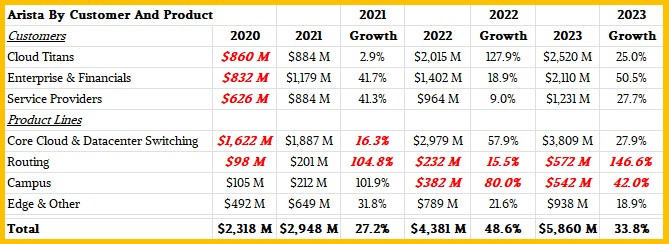

Here is our table showing the breakdown of Arista sales by customer type and product type over the past three years, derived by statements from the company and with gaps filled in or estimated by The Next Platform:

Growth among the Cloud Titans – what we call the hyperscalers and cloud builders – was muted for Arista in 2023, growing at one-fifth the pace it had in 2022 but still better than the pitiful growth it had in 2020 as Meta Platforms decided to skip the 200 Gb/sec generation of Ethernet in its networks.

Cloud Titans are still Arista’s biggest customer group, with $2.52 billion in sales, up 25 percent. And service providers grew at about the same rate (27.7 percent from 2022) to hit $1.23 billion. But enterprise and financial customers saw a 50.5 percent growth rate in 2023 as Arista burned down its backlog and more and more of these customers – many of whom are building their next platforms – seek many of the benefits that the hyperscalers and cloud builders are getting when they choose Arista to supply their switches and sometimes their routers. We shall see if the hyperscalers and cloud builders can outgrow the enterprise and financials in 2024. We think that enterprises want Ethernet for their AI clusters because they cannot absorb and manage something so different as InfiniBand, so don’t count the latter out as we move through 2024 and into 2025. The buying volumes of a reasonable share of 50,000 customers should outweigh those of eight customers.

When you do the math on what Arista says and has been saying about its products, you can see that routing is becoming as important as campus, putting pressure on both Cisco and Juniper Networks (soon to be part of Hewlett Packard Enterprise if that $35 billion deal happens). The edge is already a big part of the Arista business as far as we can tell, and it would not be surprising to see Arista to push hard in campus wireless networking, given the huge success and profits that HPE is getting from its Aruba acquisition from several years ago. And as we hinted out above, for the right motivations – let’s say Broadcom starts charging way too much for its ASICs, or Arista sees the need for an ASIC that can do switching and routing equally well as the Silicon One chips from Cisco show is possible – don’t be surprised if Arista puts together a team to create custom ASICs. Once Arista gets big enough, having that kind of control will become very attractive.

No one at Arista has suggested this is the plan, and the top brass at the company would likely scoff at the idea today.

So what? Andy Bechtolsheim created the Sparc architecture, and he is rich enough to do whatever the hell he wants whenever the hell he wants to do it.

Be the first to comment