It looks like Hewlett Packard Enterprise might be having a datacenter networking revival.

The word on the street, as reported by the Wall Street Journal, is that HPE is getting ready to shell out $14 billion to acquire Juniper Networks, the company that played the gadfly for Internet routing and switching for industry behemoth Cisco Systems before Arista Networks took over that role in switching and is increasingly involved in distributed routing.

An acquisition could be announced as soon as this week, represented about a 35 percent premium over the market capitalization that Juniper Networks had before the rumors surfaced. As its fiscal 2023 year ended in October last year, HPE had $6.47 billion in cash and equivalents in the bank. So it will have to borrow some money or float some stock to get the dough to do a deal to takeover Juniper, which has been rebounding a bit in recent years and is still a player in datacenter routing.

HPE has a long history in Ethernet switching and made its own ASICs and equipment for many years, and in November 2009, in the pit of the Great Recession, the IT giant formerly known as Hewlett Packard acquired switch maker 3Com for $2.7 billion to fuel its datacenter aspirations. At the time, HPE was beginning its quest to build an IBM-alike conglomerate that would sell hardware, software, and services in the datacenter, with its $25 billion acquisition of Compaq in 2001 and its $13.9 billion acquisition of services provider Electronic Data Systems in 2008. In 2015, HP spun out its software, services, PCs, and printers to create HPE, keeping servers, storage, networking, tech support, consulting, and financing for datacenter gear.

Like Cisco, Juniper was initially focused on datacenter routing when it was founded in 1996, just as the corporate Internet was beginning its explosive buildout, and Pradeep Sindhu created a way to make routers work on data packets, not just voice circuits. Over the decades, Juniper has created routing and switching hardware as well as network operating systems, software-defined switching applications, and security products and has amassed a huge portfolio of intellectual property. Sindhu went on to found DPU startup Fungible in 2016, which was reportedly sold its assets off to Microsoft for $190 million this time last year as that company did not reach escape velocity.

In recent years, Juniper has revitalized itself with an expanded wired and wireless LAN business and pushed hard into wide area networking across the core, metro, and edge, campus networking. Juniper has also added AI functions to network operations, and has even acquired Apstra to provide a commercial-grade version of the SONiC open source network operating system as well as an AIOps platform to automate the management of datacenter resources. It has not hurt Juniper that there is a resurgence in datacenter routing, which Juniper calls Automated WAN, as connecting multiple datacenters and regions as well as linking private datacenters to those owned and rented out by the IT giants as utilities. (They are not public clouds. . . .)

It is abundantly clear that networking is becoming more important in the datacenter and central to the efficient use of compute and storage, and it is also clear that the idea that networking will only be 10 percent or less of the budget of a distributed computing cluster is also in the past. Networking represents around 20 percent of the cost of a modern AI cluster, and we would not be surprised to see it go higher as low latency and bandwidth become more important.

This is a good reason for HPE to contemplate an acquisition of Juniper.

Another is the outstanding success that HPE has had with its Aruba Networks acquisition, which HPE did back in early 2015 when The Next Platform was founded for $2.7 billion. At the time, Aruba was pushing $729 million in sales, and in HPE’s fiscal 2023, Aruba accounted for $5.2 billion in sales, up 41.6 percent, and operating income of $1.42 billion, up by a factor of 2.6X. Last year, Aruba drove 7.9 percent of HPE’s revenues, but 39.3 percent of its operating income. Compute plus HPC & AI – which means all forms of compute – drove $15.35 billion in revenues in fiscal 2023, or 52.7 percent of all of HPE’s sales, but only drove $1.62 billion in operating income, or 44.8 percent of all operating income.

It is also worth remembering that HPE is now an innovator in high-end Ethernet networking thanks to its Cray acquisition, which gave it the “Rosetta” Slingshot ASIC that is at the heart of many pre-exascale and exascale systems these days.

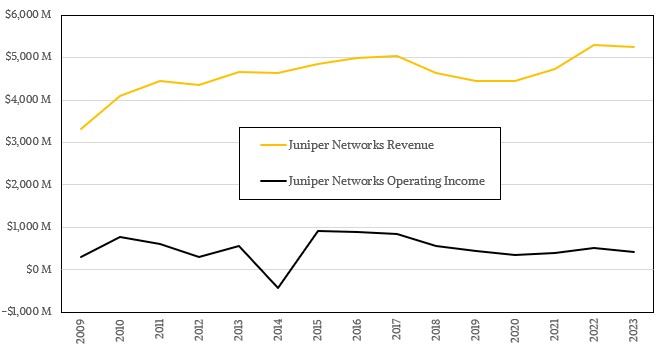

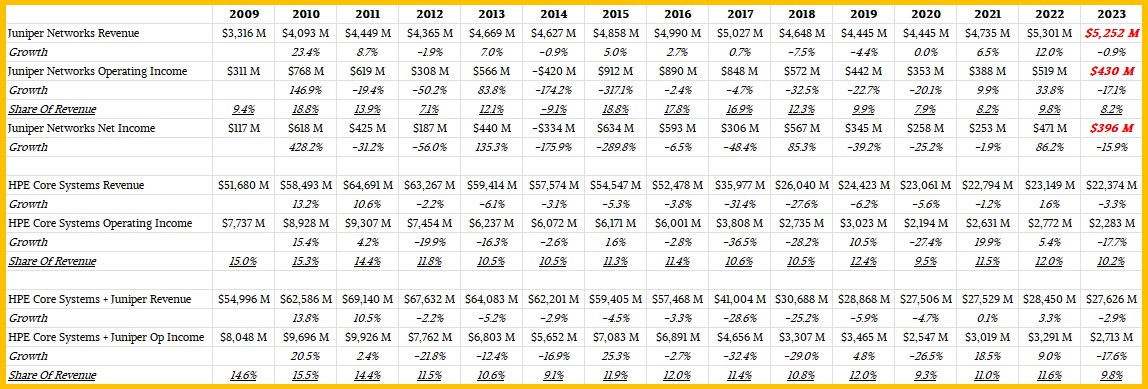

Anyway, here is how Juniper and HPE have fared on an annual basis since the Great Recession, and how the combined companies would look:

We think that companies should have to literally merge their financials when they merge their companies, as we have done as best we can given the fiscal year ends that are different for Juniper and HPE. We do not think that companies should get to book the revenue of acquired companies as “growth” unless they are in fact growing.

In the table above, we have estimated Juniper’s revenues, operating income, and net income for the fourth quarter ended in December – which the company has not reported as yet – based on guidance it gave back in October. It looks like Juniper shrank a bit last year. But, it also has $1.42 billion in cash in the bank, a massive portfolio of products and patents, and good prospects as networking is ascending in the AI era. Juniper and HPE fit together nicely, but don’t expect a big profit bump immediately – just as was the case with Aruba.

We shall see if HPE will be a networking player again. It sure would make 2024 more interesting.

Having worked at various companies in IT over the years and in particular one which did telephony ATM and Frame Relay gear, I’ve been part of several acquisitions. They generally don’t go well unless the higher ups know their stuff technically, and can winnow the wheat from the chaff from the smoke being blown up their keisters.

In my case, we had a major product just about to be released, test instances in our customers were looking great. The future looked good for a company which basically dropped new models into the core of the network and pushed the old gear out to the edges. But kept the same management and provisioning software in place, which make changes like this trivial. Well, not trivial, but certainly less taxing.

Anyway, this startup with all kinds of golly-gee-whiz-bang powerpoint slides said their new switch would blow the socks off anything else, we just need some more cash to finish it. So the idiots in the C-suite bought them, cancelled our product and the had to cancel that new startup they just bought about twelve months later once they realized it was crap crap crap.

So my story doesn’t quite relate to this acquisition, but I can forsee alot of infighting on which product is kept, which is tossed and how many many many ways there are for this acquisition to go wrong, becuase the C-suite doesn’t have the technical chops to understand the issues and make logical decisions. I’m munching my metaphorical popcorn as I watch a train wreck coming to happen.

Color me skeptical about large mergers like this, especially when you need to take out large loans (and at what interest rate!) to finance the purchase. So cost cutting and “rationalization” of the portfolio will happen, and drastically I bet. Whcih will piss off customers. Maybe they don’t want to goto Cisco, but maybe they have to?

Hopefully I’m wrong.

The loan cost is kinda crazy, I imagine. Could be done with private equity, like Michael Dell did with EMC and VMware, and that did not turn out as hoped either. Well, except Dell and Silver Lake made some dough playing the Wall Street ponies.

In HPE’s defense, I think the Compaq deal saved the company, or at least the enterprise part of it. I always thought it was a good idea to marry the thing that printed money — the printer business — to the thing that thinks it does and never quite did — the 1U and 2U server business. HPE did indeed need a complete stack as it was trying to build, but it was just not possible to do so affordably. Some things maybe only build organically over a long period of time. I think Juniper and HPE are both grown up enough to do this, if they really want to do it.

I think it’s another stupid merger for merger’s sake. The Juniper C-suite will make out like bandits, so will the Juniper shareholders. But in the long term… I suspect it will end up poorly. At this level, a 1% payout to the C-suite is just so much money it’s crazy. They get out happy, the rest get screwed.

Your story sounded awfully familiar, could it have been the Ascend-Lucent-Nexabit triangle?

Could be…. 🙂

I Think about similarity between goals from Juniper and Aruba, objetive: market penetratation and become a real competition to Cisco. Welcome both, but that merger provided an advance algorithms from Juniper, that purchase by Aruba dont need now elaborate from zero and gain some precious: time to market !! But 13.000 M dollars its excesive, I wait that business dont become another faulty Autonomy Co.. Spirit of Apotheker CEO dont are now in it Hewlett Packard co. but “Chi lo sa? “.