History doesn’t really repeat itself, but it surely does use a lot of synonyms and rhymes, and sometimes, if you listen very closely, you can catch it muttering to itself.

It is with this in mind that we contemplate the recent data coming out of Mercury Research, which is the touchstone tracker of market share data for X86 processors for mobile and desktop PCs and when AMD launched itself into the server racket in 2003, it became the arbiter of official server share stats for the X86 server space.

After a six-year fight to get back into the datacenter, with an 11.5 percent shipment share of X86 processors sold into the datacenter in the first quarter of 2021 and a solid and credible roadmap against a staggering but recovering rival Intel, it is once again safe to bet on AMD processors in the datacenter with the Epyc line. And now we will see if AMD can meet the high water mark it set in the mid-2000s when it had 2.3X the market share that it currently is enjoying.

The Opteron chips set a very high bar for AMD to leap. The “Sledgehammer” Opteron processors were announced in the fall of 1999 and delivered in the spring of 2003 to great fanfare and a certain amount of resistance from server OEMs who were afraid of crossing Intel, which was nowhere as dominant as it is today, or rather was three years ago. The original Opterons were innovative in many ways, including having 64-bit processing and memory access, multicore designs from the get-go, HyperTransport interconnects, integrated DDR memory controllers, and integrated caches that sat on a ring instead of the frontside bus – a bandwidth limiter and therefore a performance limiter – employed by Intel.

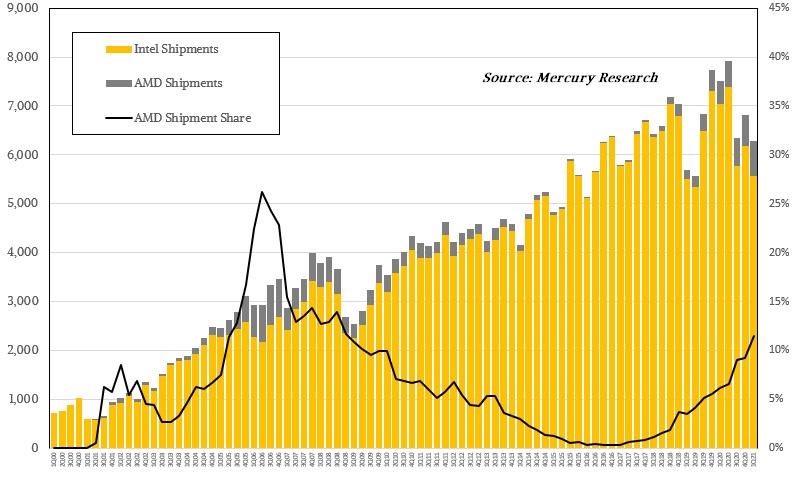

When the Opterons launched, X86 servers comprised about half of server revenues, and the shipments of X86 server CPUs were considerably smaller than they are today. Take a look at this historical chart based on more than two decades of data from Mercury Research to see just how much the server world has changed thanks in large part to hyperscalers and public clouds:

This data runs from the first quarter of 2000, which marks the beginning of the dot-com bust, more or less, and back then, well shy of 1 million server CPUs per quarter were shipping. Shortly after the Opterons launched in early 2003, thanks to the aggressive pushes by IBM and Sun Microsystems and Cray, particularly in the HPC arena that was so hungry for cheaper 64-bit compute (RISC and proprietary CPUs were relatively expensive), memory capacity, memory bandwidth, and I/O bandwidth, AMD quickly rose to 5 percent share of server shipments. Intel fought back as best it could between 2003 and 2009, when its Opteron-alike “Nehalem” Xeon E5500 processors launched into the gaping maw of the Great Recession, which made OEMs and now ODMs as well as their hyperscaler and public cloud customers a bit skittish at the same time that the Opteron line ran into some bugs and some architectural issues. The Xeon server revamp and the steady cadence of architectural advances and manufacturing advances from Intel essentially forced AMD from the datacenter, and the company walked away about a decade after the Opterons launched. The server shipments just kept rolling faster and fast, eventually compelling AMD to re-enter the server arena.

If you look at that chart above, the question you have to ask is what kind of curve are we going to get for AMD’s market share in the future? Is a new spike forming that will be as steep as we saw in the early years of the Opteron? In the second quarter of 2006 – which was nearly three years before the Nehalem Xeon revamp – AMD peaked at 26.2 percent share of server CPU sockets sold in a quarter. The rise was very fast, but the decline was about as steady and deadly. The climb during the three Epyc server chip generations, the first of which launched in the spring of 2017, has been a little more rapid than the Opteron decline, which is good. But it is nothing like the spike the Opterons saw as Intel hung on to 32-bit processing for Xeons as it tried to force people onto the 64-bit Itanium processors for servers.

Intel made a set of architectural blunders that gave AMD the opening for the Opterons and, as it turned out, it made a set of chip manufacturing blunders that would have also beset AMD if it had kept its foundry instead of spinning it out as GlobalFoundries and allowing itself to choose Taiwan Semiconductor Manufacturing Corp as its foundry. Think about that bullet AMD dodged. Imagine if it was trying to pick up the tab for a 7 nanometer EUV foundry, and then had to spike it as GlobalFoundries did back in August 2018. The mind reels. . . .

As it is, AMD has a very good partner in TSMC and has put very good processors into the field. If current trends persist, in about a year, AMD will be at around 25 percent market share, which is no doubt its goal even though Lisa Su, AMD president and chief executive officer, will never say that. Su pointed to the lower deck of 10 percent when the “Naples” Epyc 7001s launched four years ago, and there is no way she is going to point to the 25 percent upper deck for the “Genoa” Epyc 7004 or “Turin” Epyc 7005 processors due around 2022 and 2023, respectively. And for good reason. AMD’s share of the desktop and mobile PC market hovers between 15 percent and 20 percent most of the time.

It is almost as if markets like 80-20 distributions for major and minor players, but the server market may not play out quite this way. Intel may, as bullies say in elementary school, get “two for flinching.” Like this:

It is entirely possible that Intel’s server decline will be similar in shape and slope as its rise over the past decade, especially if the big public clouds and HPC centers of the world embrace the Arm architecture and do custom chips and AMD also keeps the heat on Intel, too, in the X86 arena. Markets also like 65 percent, 25 percent, 10 percent stratifications — or even 60 percent, 20 percent, 20 percent — when there are three players competing. And, and, and if Arm architectures start being a conundrum for AMD, it may even have to dust off its own Arm server chip efforts or pick up some Neoverse tech and take on Nvidia in the high-end Arm CPU sector for HPC and AI applications.

Stranger things have happened, and history keeps whispering about them.

Intel Aims For Zettaflops By 2027, Pushes Aurora Above 2 Exaflops

Just because Intel is no longer interested in being a prime contractor on the largest supercomputing deals in the United States and Europe — China and Japan are drawing their own roadmaps and building their own architectures — does not mean that Intel does not have aspirations in HPC and …

Ampere Gets Out In Front Of X86 With 192-Core “Siryn” AmpereOne

The largest clouds will always have to buy X86 processors from Intel or AMD so long as the enterprises of the world – and the governments and educational institutions who also consume a fair number of servers – have X86 applications that are not easily ported to Arm or RISC-V …

Nvidia Enters The Arms Race With Homegrown “Grace” CPUs

There has been talk and cajoling and rumor for years that GPU juggernaut Nvidia would jump into the Arm server CPU chip arena once again and actually deliver a product that has unique differentiation and a compelling value proposition, particularly for hybrid CPU-GPU compute complexes. And today, at the GTC …

It would so great to have a full on brawl between AMD, Intel and nVidia for CPU market share, as well as GPU market share.

AMD acquired Xilinx, so it doesn’t have to dust off an ARM design, it has them, shipping now. AMD will likely optimize it and we will see the fruits of the marriage in a couple years.

You are absolutely correct. I have no reason to believe that the Xilinx deal will be halted. So, once the deal is approved the sky’s the limit. I feel that 2 years after the deal is approved the two companies will create fireworks with new products being introduced. Cheers AMD and Xilinx Share Holders.

Counterpoint Epyc market share assessment;

Mercury Research is mistaken on AMD Epyc commercial market share evident reliance on Intel shipments. Mercury Research appears to rely on the erroneous INTC DCG revenue data to determine quarterly Intel shipments? Such an error is compounded on Mercury Research and AMD awareness of Epyc share relying on eBay channel inventory management tool Mercury Research and AMD also rely. Replaces Intel supply signal cipher quarterly by product category into future time INTC revenue and margin calculation tool industry and financial market relied 1997 through 2014 fading away entirely by 2016 on BK shutting supply signal cipher down on that SEC violation substantiating cartel operation at American Column and Lumber Company v United States, 257 U.S. 377 (S.Ct 1921).

On eBay channel inventory management tool, Epyc Rome / Milan v Xeon Ice Lake + Cascade Lake + CLr at what one can consider ‘current’ commercial market share;

AMD = 3.47% and Intel = 96.53%

Epyc Rome / Milan + Naples v Xeon Ice Lake + Cascade Lake + CLr + Skylake;

AMD = 2.09% and Intel = 97.91%

Decomposing Mercury Research q1 AMD Epyc ‘server share’ said 8.9% on Camp Marketing 1,005,180 q1 Epyc sold suggests 10,258,020 Xeon calculated $5.6 billion / net $546 is 79.4% off $1K Average Weighed Price for Cascade Lake full run.

Mercury presents a lower volume scenario I was unaware until this Next Platform report displaying long run assessment. Places q1 Xeon net on 5.5 M units at $1019 is a 61.6% discount off Cascade Lake 1K AWP in quarter.

Camp Marketing full market share report; commercial, workstation, desktop and mobile here;

https://seekingalpha.com/instablog/5030701-mike-bruzzone/5590014-amd-and-intel-cpu-and-amd-and-nvidia-gpu-market-share-on-may-8-2021

Mike Bruzzone, Camp Marketing

Hi Mike, thanks for sharing your views in here. You mention “ebay” which seems odd to me. I doubt the hyperscalers are buying their server infrastructure components from ebay, they probably purchase directly from AMD (or very close to direct), and most of them are building their own server equipment these days which means they are not buying pre-built commodity servers like in the old days. I may be mistaken with how things work in the server sales world, feel free to educate me. thanks!

E7 MP and E5 4-way still procured by Hyperscalers Next Platform Tim has done a cost : price analysis v Scalable lakes; no issue other than fully depreciated money making. CPUs available from eBay where Hyperscale and Cloud are both del credere broker dealers, traders and consumers. mb