If Nvidia’s Datacenter business unit was a startup and separate from the company, we would all be talking about the long investment it has made in GPU-based computing and how the company has moved from the blade of the hockey stick and rounded the bend and is moving rapidly up the handle with triple-digit revenue growth and an initial public offering on the horizon.

But the part of Nvidia’s business that is driven by its Tesla compute engines and GRID visualization engines is not a separate company and it is not going public. Still, that business is sure making things a lot more fun for Nvidia as it starts taking a bite out of compute in the datacenters of the world.

The Real Tick Tock That Drives A Compute Chip Maker

Much is made of the fact that under former president Pat Gelsinger (who has been chief executive officer at VMware for a few years now) Intel came up with the tick-tock model of chip rollouts. With a tick, Intel shrinks the chip transistor geometries, from say 32 nanometers down to 22 nanometers, and with a tock, a new microarchitecture for the chip is rolled out on that perfected process. This worked brilliantly, but the real tick-tock is that Intel had a desktop chip business on which it manufactured its largest number of chips to perfect those manufacturing processes and core chip elements (call that a tick and while you are at it call it the Core chip business as Intel does) and then it could leverage that PC chip technology to create the Xeon family for servers, using even more mature manufacturing processes and esoteric elements added to the core and the uncore areas of the chip specifically needed for systems (call that a tock). The Xeon chips are inherently more profitable, which is why Intel’s Data Center Group has roughly 45 percent to 50 percent operating margins.

With its Tesla and GRID GPU motors now delivering material results for the past several years, this is a kind of tock to the ticking of Nvidia’s GeForce and Quadro graphics card businesses, which are just booming during the “Pascal” generation of GPUs. The profits on the Tesla and GRID products are considerably higher and so are the unit costs, so a relatively low volume of units can drive substantial revenues and profits for Nvidia, feeding back into the research and development for GPUs in general and for datacenter workloads in particular. This is a cycle every bit as virtuous as any one that Intel has ever demonstrated, and that is why the revenue and profit curves for Nvidia have been on the rise in its latest fiscal year – and why we think they will likely continue for the foreseeable future as workloads are accelerated.

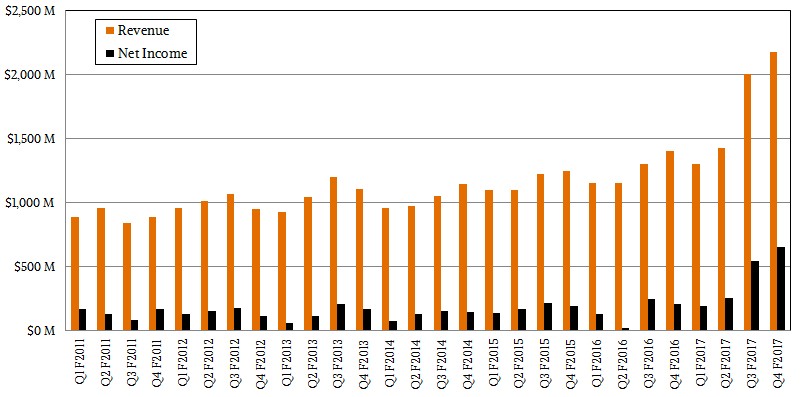

In the quarter ended January 29, Nvidia posted sales of $2.17 billion, up 55 percent, and net income rose by 216 percent to $655 million. For the full year, revenues were up 39 percent to $6.91 billion and net income shot up by 171 percent to $1.67 billion.

The company ended the quarter with $6.8 billion in cash and equivalents, plenty of money to continue to invest in its core GPU business and expand its compute business from simulation, modeling, and visualization to deep learning and database acceleration and on to the next big things like augmented reality, autonomous vehicles, and IoT.

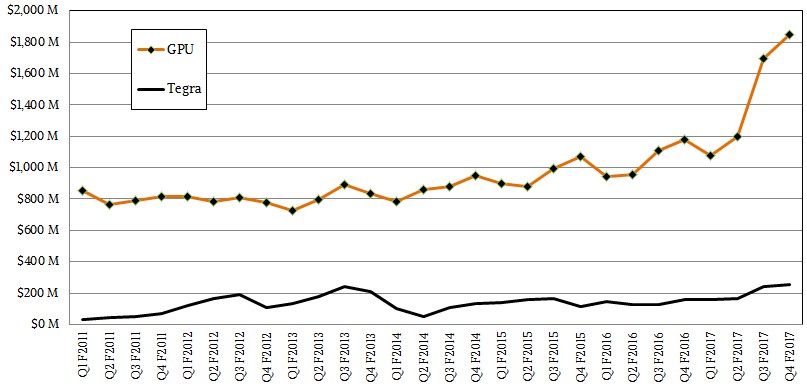

The core GPU business accounted for $1.85 billion in revenues, up 57 percent, and the Tegra embedded chip business, which combines custom ARM cores with cut-down Nvidia GPUs, drove $257 million in sales, up 64 percent.

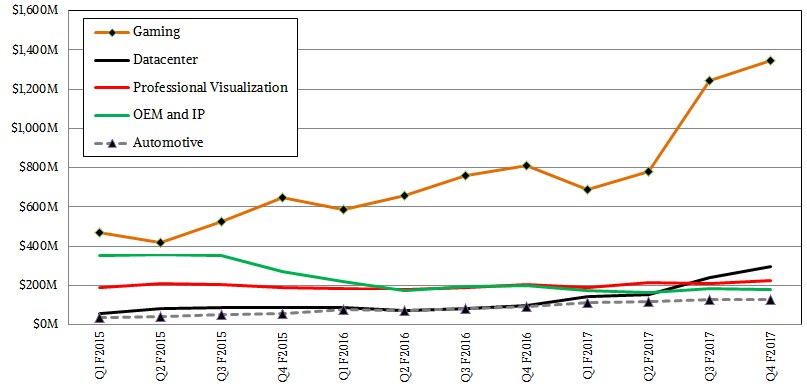

The only part of Nvidia’s business that was down in the fourth quarter of fiscal 2017 was its OEM and intellectual property division, which fell by 11 percent to $176 million. All other units were on the rise, thanks in large part to the Pascal generation of GPUs, which are hitting Nvidia’s various markets at a time when the appetites for GPU cycles are high and meet people’s personal or corporate budgets. The Professional Visualization division of Nvidia was more muted, with only 11 percent growth to $225 million, but that was in no small part due to the fact that Nvidia had not yet launched its Quadro GP100 card, which is at the heart of what Nvidia calls the “supercomputer workstation” and which was launched last week. If there is a Pascal effect – perhaps by Easter and Passover, which would be funny – for the Quadro line, it will kick in next quarter. Nvidia is in love with cars and autonomous ones at that because each card requires a supercomputer of sorts to drive itself and massive data analytics on the back end to train deep learning models and process telemetry from live cars as they operate. Nvidia’s Automotive division saw a 38 percent revenue jump, to $128 million in what is still very much a nascent market.

The star of the final quarter of the fiscal 2017 year was without question the Datacenter division, with revenues up by 205 percent to $296 million. That’s a more than tripling of this business over the fourth quarter of fiscal 2016, yielding a run rate of this business of $1.2 billion. Datacenter compute and visualization, as Nvidia counts it, drove 13.6 percent of total revenues for Nvidia in the quarter, up from 6.9 percent in the year-ago period. We think plenty of datacenters deploy GeForce and Quadro cards to do compute and visualization jobs from inside the glass house and Nvidia’s Tesla and GRID lines do not tell the whole story. But set aside how many hyperscalers and HPC centers use TitanX cards for compute for a minute and just look at the numbers. If you take the Datacenter group out of the Nvidia numbers, the company would have only grown by 44 percent instead of the 55 percent it turned in.

Nvidia does not break down Tesla sales distinct from GRID sales in its public presentations, but in a call with Wall Street analysts, Colette Kress, the company’s chief financial officer, said that the GRID business that is part of the revenue driver for the Datacenter division doubled year-on-year for fiscal Q4, driven by the education, automotive, and energy sectors. That implies that the Tesla compute part of this Datacenter division actually grew by more than a tripling if the overall business tripled. If you have a little fun with math here, if Tesla accounted for two-thirds of the Datacenter business in Q4 fiscal 2017, then GRID sales doubled to $99 million and Tesla sales more rose by 312 percent – more than quadrupled – to $197 million. If you assume that Tesla accounted for 75 percent of Datacenter sales in fiscal Q4, then GRID doubled to $74 million and Tesla rose by 270 percent (nearly quadrupled) to $222 million. That is a hefty Tesla compute business, for which about half is coming from deep learning jobs and half from traditional simulation and modeling jobs, based on past statements from Nvidia. By the way, the Datacenter division also books sales of the company’s DGX-1 systems, which combine Intel Xeons and Nvidia GPUs to make a fat compute node that is aimed initially at deep learning pioneers.

Looking ahead to the first quarter of fiscal 2018, Kress told Wall Street that Nvidia expected revenues of $1.9 billion, plus or minus 2 percent, and at that midpoint growing 46 percent year-on-year, and added that sales in the Datacenter group would grow sequentially but Kress did not say by how much. Somewhat more vaguely and presumably on a wider time horizon, Nvidia chief executive officer and co-founder, Jen-Hsun Huang, had this to say: “So these pieces, AI, high performance computing, cloud computing, GRID, and DGX, all in contribution, contributed to our growth in Datacenter quite substantially. And so my sense is that, that as we look forward to next year, we are going to continue to see that major trend.”

No market triples forever, of course. But there is plenty of room as simulation and modeling in traditional HPC adopts GPU acceleration, databases and other kinds of transaction processing get accelerated, and as deep learning is added to all kinds of applications. The quadrupling in the Tesla business could, with some lumpiness thanks to the buying habits of hyperscalers and HPC centers, continue for some time, then will settle down to tripling then doubling then growing at 50 percent then 25 percent then the IT market at large. Precisely how Nvidia will fit to that curve remains to be seen. But no technology escapes that curve, even those that define it like the X86 processor that has as it rose from the desktop and jumped to the glass house in the past 25 years. When all is said and done, the Tesla business could easily be the size of the gaming part of the Nvidia business, and drive half of the company’s profits some years hence. It will be fun to see if that happens.

Now, all eyes turn to the “Volta” VP100 GPU for Tesla compute.

RELATED STORIES

The Case For IBM Buying Nvidia, Xilinx, And Mellanox

Pascal GPUs On All Fronts Push Nvidia To New Highs

Nvidia CEO’s “Hyper-Moore’s Law” Vision for Future Supercomputers

How Nvidia’s Own Saturn V DGX-1 Cluster Stacks Up

Deep Learning Drives Nvidia’s Tesla Business To New Highs

Not Just Tesla the whole car market should double this stock soon .