If the server and storage markets are bellwethers for the underlying strength of the economy, as we at The Next Platform believe, then the global economy has been perhaps more healthy than other indicators might have been pointing to. There is always a several month lag in the shipment and sales data for servers and storage, so we won’t really have a sense of what is going on right now until the end of the autumn. But through the quarter ended in June, the markets looked pretty good, all things considered.

The analysts at IDC recently released their market trackers for servers and storage for the second quarter, and we like to look at them at the same time to get a sense of how these increasingly interconnected aspects of the systems space are doing. It is hard to tell a server from a storage array sometimes – you end up counting drive bays in the system, explains IDC storage analyst Eric Sheppard, and making the best estimations about if a machine is compute-intensive or storage-intensive when it sells.

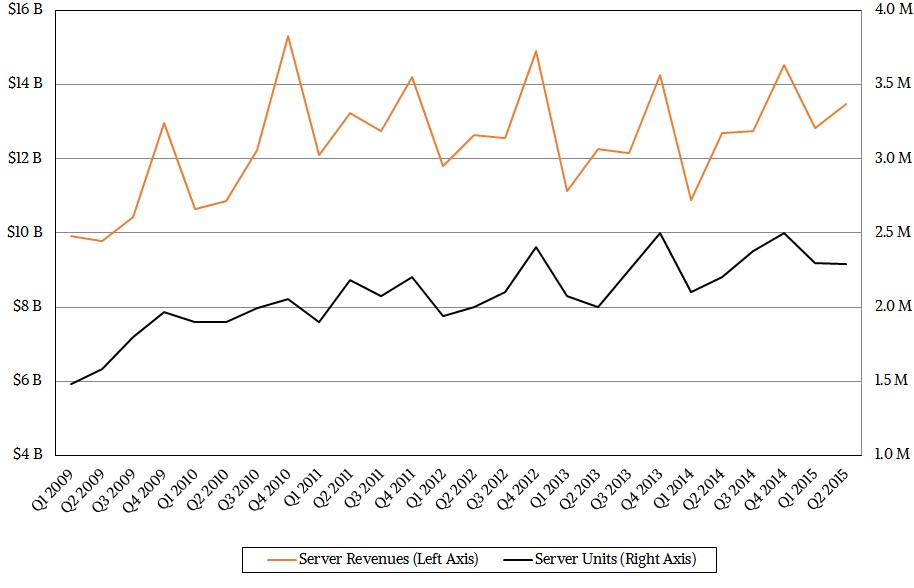

On the compute side, IDC reckons that the world consumed $13.48 billion worth of servers in the second quarter, and increase of 6.1 percent compared to the year-ago period. Server shipments across all types and geographies rose by 3.2 percent to 2.29 million machines, more or less flat with the first quarter of the year.

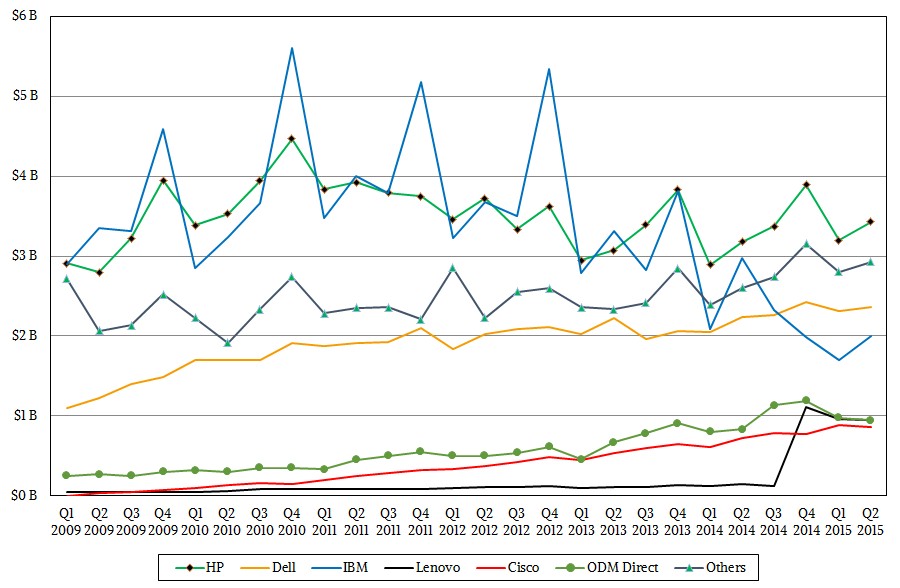

The top seller in the market for the past several years has been Hewlett-Packard, which substantially increased its lead over IBM once Big Blue sold off its System x business to Lenovo Group last fall. HP booked $3.43 billion in server sales in the second quarter, up 7.7 percent and growing faster than the market at large. Dell, now ranked number two, grew slightly slower than the overall market, with a 5.9 percent bump to $2.36 billion. Thanks to the uptake of its Cloudline servers aimed at hyperscalers and its Apollo machines aimed at HPC and enterprise customers, HP grew its density-optimized server business by 118.7 percent in the quarter, says IDC. ProLiant rack machines saw a 10.5 percent rise in revenues, and that means towers probably had soft sales. Dell’s blade server business – yes, enterprises and some HPC shops still buy blade servers – grew by 38.7 percent in Q2 and was that company’s bright spot in terms of growth.

IBM was the third largest revenue server seller in the quarter, with just under $2 billion in sales, and had a 32.9 percent revenue drop thanks mostly to the System x divestiture to Lenovo. But not all of that revenue went automatically over to Lenovo, which grew by a factor of 6.5X to $949.2 million for server sales in the second quarter. All of IBM’s competitors in the systems space seem to take a little piece out of the IBM-Lenovo deal. Cisco Systems is one of those beneficiaries, with sales up 19.3 percent to $866.7 million in the quarter. While the Unified Computing System platform has grown phenomenally in the past several years, its growth has been cooling and eventually – perhaps in a year or so – its growth will be closer to the market as a whole.

A very interesting part of this server market is the ODM Direct part, which IDC has been tracking for several years. In the quarter, those original design manufacturers who create and build systems on behalf of hyperscalers, cloud builders, and some enterprises, have outpaced the overall market and come to represent a large part of the shipments in many quarters. In Q2, ODM Direct vendors in the aggregate accounted for $942.6 million in revenues, up 12.9 percent and growing at more than twice the pace of the market at large. ODM server revenue growth cooled in the quarter, and frankly has been cooling for the past four quarters from a high of 44.1 percent growth in the third quarter of 2014 and has been wiggling around $1 billion per quarter in machines.

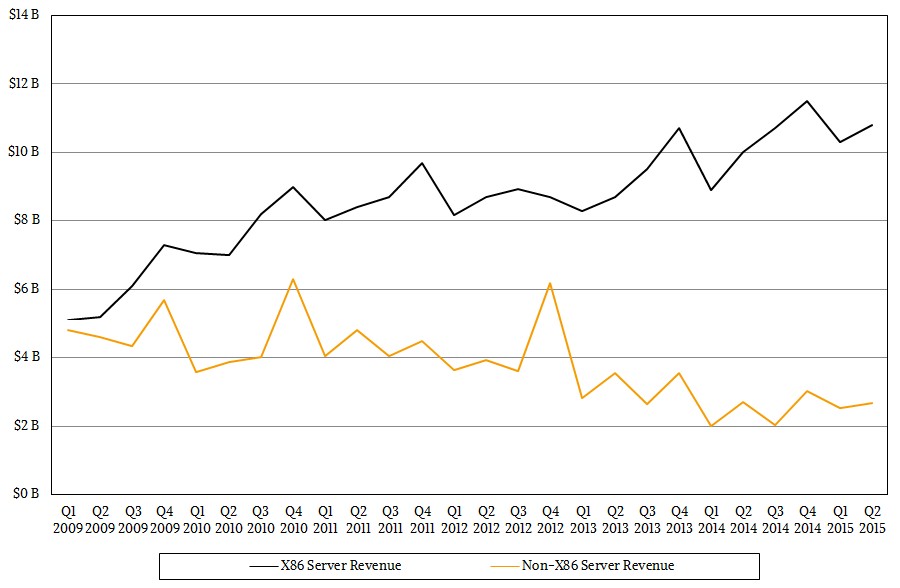

The X86 server – by which is meant machines running Intel Xeon processors with a very minuscule portion of machines based on Opteron processors from AMD – continues to dominate the datacenter, accounting for 99.1 percent of shipments (2.27 million machines) and 80.1 percent of revenues ($10.8 billion) in the second quarter. Intel keeps trying to push down the price of compute because it believes that, according to Jevons Paradox, that making a commodity like compute even cheaper it can actually boost the amount of capacity it sells and thereby increase its revenues and profits. (We shall see in the laboratory of the real world precisely what the appetite for elastic capacity is. We remain skeptical that this can go on forever, even with burgeoning datasets and new use cases.)

IBM’s Power Systems machines found their footing in the second quarter with modest declines and the System z mainframe upgrade cycle continued, helping to buoy sales of non-X86 systems, which nonetheless had a 1.4 percent revenue decline. ARM-based servers are just a blip on the radar at this point, and while many are hopeful that ARM server chips can provide compelling value and advantages in the datacenter, this idea has not yet been put to the real test. The ramp could begin early next year, or fizzle out because the software has still not caught up to the hardware.

On the storage front, the ODM Direct vendors continue to be truly and dramatically disruptive, although sales of traditional external disk arrays are holding up better than many might think.

In the quarter, customers worldwide consumed 30.3 exabytes of storage systems, a 37 percent boost in capacity over the year-ago period, but revenues rose only 2.1 percent to $8.8 billion. The rise of server-based storage with open source object, file, and block storage is having the same effect on storage as the Linux revolution from the early 2000s had on servers.

IDC reckons that ODM Direct vendors creating minimalist, dense server-storage hybrids had 25.8 percent revenue growth in the quarter, to just over $1 billion in sales, but amazingly, these ODMs accounted for 13.3 exabytes of total capacity shipped. The ODMs had an 11.5 percent revenue share, but a 43.8 percent capacity share. This is the level that the ODMs have had, with some wiggling up and down, for the past year and a half. The cost of a terabyte of storage on a traditional array from EMC, IBM, HP, NetApp, and so forth has been falling from around $875 per TB in the first quarter of 2013 to around $459 per TB in the second quarter of 2015, but the price the ODMs are charging has been falling at about the same rate, from $119 per TB in Q1 2013 to $76 per TB in Q2 2015. That six-to-one price difference is driving the capacity sales for ODM gear, which is used to store the coolest data, generally in object formats.

Traditional external disk arrays accounted for $5.67 billion in revenues in the second quarter, down 3.9 percent. While this market is not going away, it is under extreme price pressure – particularly as more workloads are virtualized and server SANs from Nutanix, VMware, SimpliVity, and others are gaining traction and obviate the need for real SANs. IDC believes that server-based storage (from ODMs as well as from hyperconverged vendors like those mentioned above) accounted for $2.1 billion, up 10 percent.

Cloud Is The Dominant Platform Consumption Model – So What?

If The Next Platform is about anything, it is about chronicling the tectonic changes that affect the IT landscape. Ditto for the prior decades of work by the co-editors before the launch of this publication nearly seven years ago. We have been watching the cloud change the distribution and consumption …

IT Spending Projections Go Negative For 2020

“When the facts change, I change my mind. What do you do, sir?” It is not clear if either Winston Churchill, who among other things was First Lord of The Amiralty, Secretary of State, AND Chancellor of the Exchequer before becoming Prime Minister of England during World War II, or …

IT Spending Prognostication During The Great Infection

The Great Infection is unique among recessions in that it is essentially a self-imposed economic downturn, not the result of over-exuberance or excess optimism or greed, but by a spikey ball of fat that is not alive but is more like a self-replicating biological machine that only knows how to …

Be the first to comment