“When the facts change, I change my mind. What do you do, sir?”

It is not clear if either Winston Churchill, who among other things was First Lord of The Amiralty, Secretary of State, AND Chancellor of the Exchequer before becoming Prime Minister of England during World War II, or John Maynard Keynes, legendary British economist who wrote The General Theory of Employment, Interest and Money during the Great Depression and encouraged national governments to spend into a downturn to avoid financial disaster, said that.

What matters more than who said that quote above is that someone smart said it. Conditions are definitely changing fast in the economies of the world here in the Great Infection, and that means a lot of leading indicators about those economies are going to change, too. Only two months ago, before the coronavirus pandemic broke out, IDC had been expecting for IT spending (in constant currency in 187 different geographies) to grow by 5.1 percent this year, and by February that had slipped to 4.3 percent. Only six business days ago, the economists and IT market researchers at IDC had pumped in new stats into their models and figured it was probable that IDC spending would grow by only 3.7 percent in 2020, with a pessimistic estimate of only 1.3 percent growth. We went through its stats and forecasts out to 2023 and a drilldown into spending levels by type – smartphones, PCs, servers/storage, software, and services on Tuesday last week. Here it is Monday the following week, and the IDC economists and IT market watchers are coming back with revised projections.

It’s not good news, but it is not awful, either. And remember – forecasters are not causing the decline, so don’t blame the messengers, including us. But that said, when we all read the forecasts, we react to them, and they have a note of self-fulfilling prophecy like all socio-economic phenomena do.

“Overall IT spending will decline in 2020, despite increased demand and usage for some technologies and services by individual companies and consumers,” Stephen Minton, program vice president in IDC’s Customer Insights & Analysis group, who has been tracking and forecasting IT spending for 22 years, said in a statement released late last week accompanying an updated and much more pessimistic forecast on IT spending. “Businesses in sectors of the economy that are hardest hit during the first half of the year will react by delaying some purchases and projects, and the lack of visibility related to medical factors will ensure that many organizations take an extremely cautious approach when it comes to budget contingency planning in the near term.”

The Worldwide Black Book on IT Spending that IDC puts together always includes an estimate of real global gross domestic product paired against IT spending in constant currency, and generally, whatever global GDP is, global IT spending is in the neighborhood of 2X that. And when things go bad, the 2X rule also often holds, in our observation of the data over the decades.

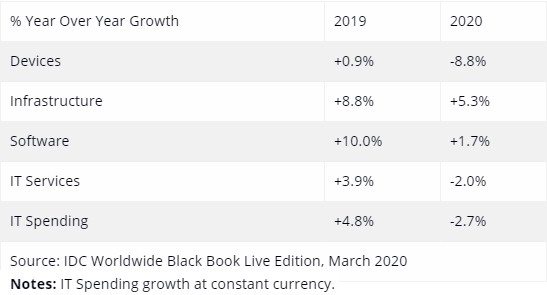

In the January forecast, Minton and his team were expecting real GDP to grow by 2.4 percent and IT spending to rise by 5.1 percent, as we have said above. And in February as the Great Infection was spreading and causing much economic consternation, the GDP growth rate for 2020 was cut down to 2 percent – no big deal really – but IT spending growth was shaved by much more, to 4.3 percent. At the end of March – which was two weeks after the data we cited from IDC was published in an interim update of the Worldwide Black Book – IDC took another look and reckoned that global GDP was going to actually shrink by 1.7 percent and IT spending was going to contract by 2.7 percent. That’s not as bad as the contraction we saw in the Great Recession back in early 2008 through early 2010. (I am talking about the IT spending recession there, the economic recession started in late 2007 and we began to come out of it in late 2009. Things in the IT budgets were not really fixed until a few years after that.)

Now, IT device spending – smartphones, tablets, desktops, and laptops – is going to get hammered, according to IDC. The PC market was already expected to be soft to down before this all happened, so if you need a new PC, this might be a good time to make a deal with your supplier. IDC is expecting for total infrastructure spending – including on-premises gear plus capacity bought by the public cloud providers plus revenue generated from their clouds, will rise by 5.3 percent.

“Hardware spending in general is always identified for rapid spending cuts during any economic crisis, as a means for enterprises to quickly protect short-term profitability,” Minton explained in a statement. “In previous economic crashes, IT hardware has tended to overshoot the economic cycle on both the downside and in the recovery phase. That’s because underlying demand drivers don’t change overnight, but the timing of purchases is shifted and delayed, and this can now be done even more quickly than in the past. What’s different now is that cloud is a bigger factor than it was in any previous global recession, and this should mean that overall spending is less volatile than in the last two major IT spending downturns.”

A thought: It seems to me that there is some double counting of revenue. To do this right, you have to amortize each wave of hyperscale and cloud server buying over three or four years and find out the spending at any given quarter and then amortize the on premises spending over four or five or six years depending on the platform to actually get a model of IT server and storage and networking capacity available. This is what we need to be tracking. Adding up public cloud infrastructure as a service spending with on premises server revenue each quarter doesn’t tell you anything about what is going on except as they rise and fall you can see changes. What we want to know is this: How much capacity is there, how much does it cost, how much is being consumed, and how are these all changing over time?

None of this IDC data really does this. It is better than nothing. Don’t get us wrong. But this is somewhere between sentiment and real data.

Here are the growth rates in IT spending by category from IDC, contrasting 2019 growth rates to those now expected for 2020:

Services spending just went south, and while software spending is expected to hold up – particularly thanks to the subscription model of pricing that has been in transition from perpetual licensing for the past decade – the growth rate is being cut by more than a factor of 5X.

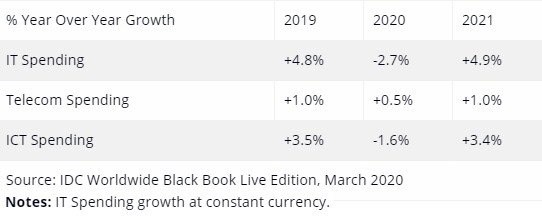

IDC also put some numbers out in the latest forecast to cover the broader information and communications technology (ICT) sector, which you can see here:

Telecom spending is going to hold up fine – we are more dependent on our broadband and cellular Internet and wireline and cellphone voice services with so many of us working remotely for the coming months. The total ICT market, again in constant currency, will fall by 1.6 percent to just under 4.1 trillion, and is expected to rebound to 3.4 percent growth in 2021. It is interesting to note that IDC is also focusing a return to “normal” IT spending in 2021, with a 4.9 percent growth rate, and “normal” telecom spending, with a 1 percent growth rate, in 2021 as well.

We remain skeptical but hopeful. With the current projections, somewhere around $275 billion in ICT spending is going to vaporize this year, and the gain from 2020 to 2021 will be just shy of $140 billion. That lost money in 2020 does not come back. If you compare ICT sales in 2019 to the forecast 2021, the growth is only 1.7 percent. If you add it up over where things might have been, somewhere around $215 billion in ICT revenues that might have been booked in 2020 and 2021 are gone. And it looks like IT spending will take a much bigger hit than that because telecom spending is actually growing.

There is a reason why people are going to call this The Lost Year, and there is every reason to believe these forecasts will be downshifted again depending on how long the Great Infection lingers.

The important thing for now is to be safe. We will sort this all out when we get through the pandemic. Of this, we are sure. So just be safe.

The Dance Between Compute And Network In The Datacenter

In an ideal world, there is a balance between compute, network, and storage that allows for the CPUs to be fed with data such that they do not waste too much of their processing capacity spinning empty clocks. System architects try to get as close as they can to the …

Datacenter Infrastructure Is Still Only Partly Cloudy

If you want to understand datacenter infrastructure and how the market for wares is changing, it helps to start with an absolute, top-down, all-encompassing view that brings together all server, storage, and switching revenues into a single bucket, eliminating the overlaps that occur when talking about these three different categories …

Just How Big – Or Small – Is The Quantum Computing Racket?

There is no question in our minds here at The Next Platform that quantum computing, in some fashion, will be part of the workflow for solving some of the peskiest computational problems the world can think of. What we have had our doubts about is if anyone can ever make …

Q; “What we want to know is this: How much capacity is there, how much does it cost, how much is being consumed, and how are these all changing over time?

IT (commercial) compute and mass market compute as in investment, use, displacement, replacement, supply and demand is tracked and can be estimated at the links below on data updated every week; each answer to each query can be estimated, imagined if not articulated from this base data which foretells the answer to questions 1) how much capacity, 3) how much is being consumed, 4) change over time.

Question 2, how much does it cost is known and can be estimated on CPU percent of various category system Bill of Materials; + 85% over OEM price of each CPU in said system or across infrastructure. That percent, the multiplier, must vary on the type of infrastructure, however, can be ascertained for every specific type of data processing and communications equipment and system infrastructure type. I’ll leave that to the various category experts

Pictures speak a thousand words;

https://seekingalpha.com/instablog/5030701-mike-bruzzone/5406075-intel-x86-q4-2019-channel-inventory-report

https://seekingalpha.com/instablog/5030701-mike-bruzzone/5400844-amd-q4-2019-channel-inventory-report

https://seekingalpha.com/instablog/5030701-mike-bruzzone/5429911-gpu-channel-inventory-today

Mike Bruzzone, Camp Marketing