There are a lot of things going on in the datacenter and campus interconnect markets, but one of the weirder things we observe from the most recent market data coming out of IDC about the Ethernet portion of this market is that it is like a country music record being played backwards.

You know what happens in such a reverse song: The truck starts to run again, the dog comes back, and the girl comes back, too.

In the Ethernet version of a country song playing backwards, Cisco Systems is growing a lot faster than the market and Juniper Networks is growing almost as fast as the market, and Hewlett Packard Enterprise and Arista Networks are growing faster than the market at large. It’s like the last decade didn’t happen or something, and it is weird.

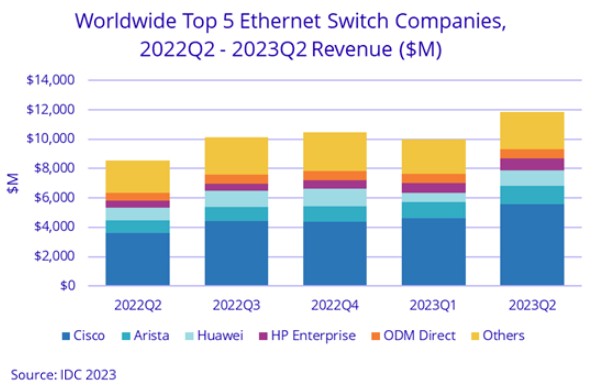

According to data on the Ethernet switch and router markets from IDC, in the second quarter of 2023, Cisco saw revenues rise by 55.3 percent to $5.55 billion, giving it 47.1 percent share of Ethernet switch revenues. Juniper Networks, which has not been among the top five Ethernet networking vendors for many years for more than a decade, had a 35.2 percent revenue rise to $342 million, giving it 2.9 percent share of Ethernet switching. Juniper is still not a top five vendor, but it is showing some life.

Arista Networks grew at a slightly faster pace than the Ethernet switch market at large, rising 42.6 percent to $1.22 billion, and Hewlett Packard Enterprise, thanks in large part to its Aruba wireless networking business, grew by an amazing 78.8 percent to $831 million. Huawei Technologies, despite export restrictions, managed to grow by 17.7 percent to $1.05 billion, its third quarter in the trailing twelve months where it broke through $1 billion in sales.

Here is the official IDC chart showing vendors over time:

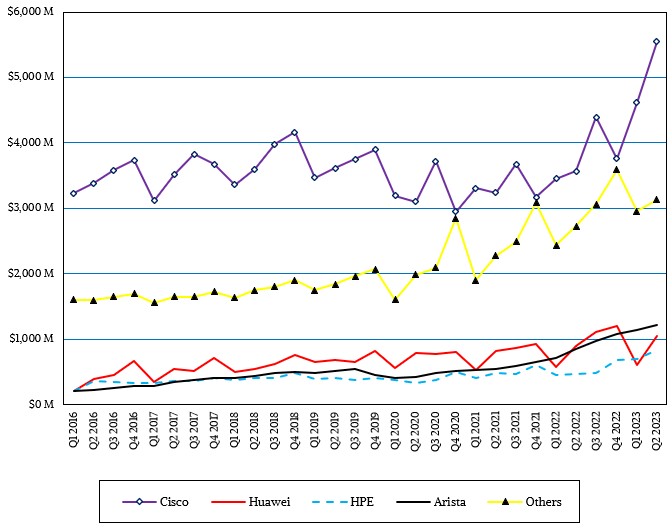

And here is ours, which has a longer time horizon and which is much easier to read:

Look at that Cisco uptick. Crazy, right? How much of this is driven by supply chain loosening up and fulfilling back orders and how much is based on adoption of switch gear based on Silicon One ASICs from Cisco.

It is interesting to see in the IDC chart how much direct sales by the original design manufacturers (ODMs) have grown in the quarter, with a 12.2 percent increase year on year and representing 12.6 percent of total datacenter Ethernet switch and routing revenues, or $1.49 billion. Collectively, the ODMs have a much smaller share of the Ethernet switching market than they do of the server market, where it is on the order of 50 percent, depending on how you want to count the semi-custom server businesses of Lenovo, Inspur, and Dell.

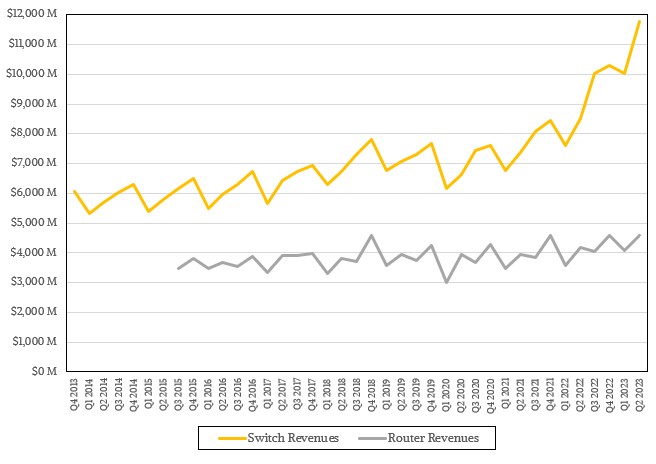

Add it all up and Ethernet switching in the aggregate accounted for $11.79 billion in sales in the June quarter, up 38.4 percent, and router sales squeaked out a 9.4 percent increase to $4.58 billion.

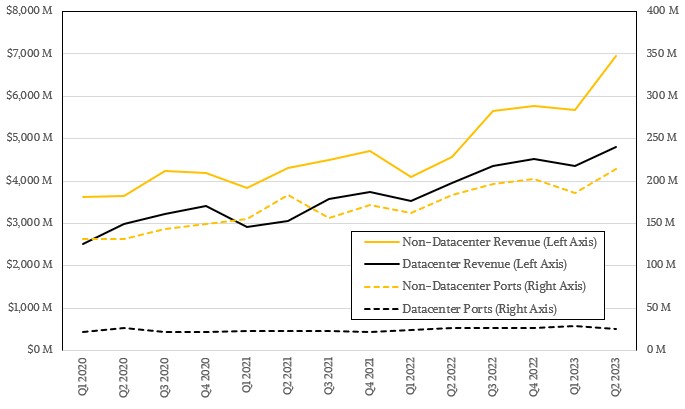

Not all is rosy, however. Yes, sales of Ethernet switches into the datacenter rose by 21.7 percent to $4.81 billion, comprising a relatively anemic 40.8 percent of total Ethernet switch revenues. And as best as we can figure, because IDC has stopped giving out port counts but we can work from historical data to reckon them, it looks like datacenter Ethernet ports were off 2.4 percent 25.8 million in the quarter, representing about 10.8 percent of total ports shipped, which is a few points shy of normal.

Sales of Ethernet gear for the edge and campus rose by a stunning 52.5 percent to $6.96 billion, and port counts shipped in Q2 2023 were up (we reckon) by 16.6 percent to 213.7 million ports. That is amazing, and so is the sales of gear that runs at 10 Gb/sec or lower speeds. In the long run, all of this campus and edge networking will put pressure on the datacenter, but if compute moves out to the edge and into the campus, maybe not.

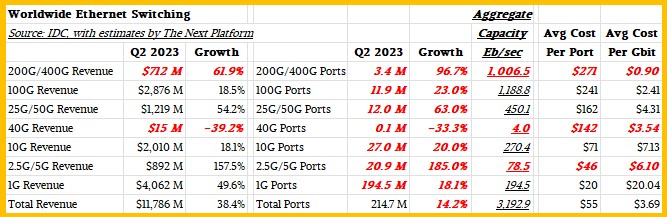

We love trying to figure out the aggregates of ports and bandwidth shipped each quarter based on the IDC data, and here is the summary table we have put together for Q2 2023:

IDC has stopped giving specifics about port counts other than rates of decline or increase, so we have to do our usual spreadsheet magic to fill in the gaps.

As usual, everything in bold red italics is an estimate by The Next Platform. Remember this is not the installed base, but new switch sales for the quarter. With switches sitting in the field for five, six, or seven years in the big datacenter operators and even longer in enterprises, governments, and academia, there is probably a mountain of some truly crufty stuff out there. But, in time, it will all be replaced, especially as the cost per bit comes down at an exponential rate for ever-more-capacious Ethernet switches.

The cost per bit does continue to drift down, but as everyone jumps up a bandwidth band as they upgrade, the pressure for that is not as great as you might surmise.

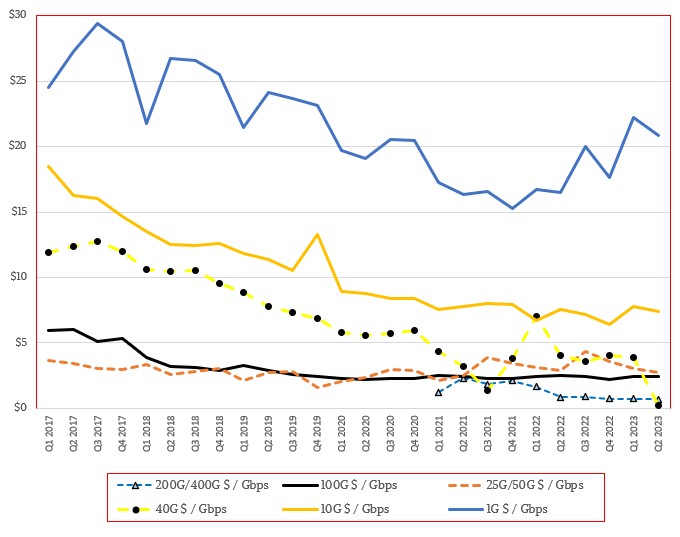

What is interesting to us is that the cost of a Gb/sec of bandwidth is 29.5X more expensive on a 1 Gb/sec switch as it is on a 400 Gb/sec device – just under $21 for the former and under three quarters of a dollar for the latter. Imagine, if you will, how low the cost per Gb/sec of 800 Gb/sec and 1.6 Tb/sec devices will be some years hence. . . . And yet, somehow, the 1 Gb/sec switching segment will still somehow dominate the Ethernet switch market. It is hard to imagine a time when 10 Gb/sec will be the dominant bandwidth sold in the world. But that day will come, perhaps before we all retire – and perhaps not.

We would love to see similar data for InfiniBand and other proprietary interconnects, and a breakout of sales of interconnects for AI and everything else.

“We would love to see similar data for InfiniBand and other proprietary interconnects, and a breakout of sales of interconnects for AI and everything else.”

650 Group does exactly this (at least for networking for AI and IB). They had a new report come out a couple of days ago

“And yet, somehow, the 1 Gb/sec switching segment will still somehow dominate the Ethernet switch market. It is hard to imagine a time when 10 Gb/sec will be the dominant bandwidth sold in the world.”

…20 Years ago I had multiple Sun E6500s each connected via 8 x 1Gbit (fiber) Ethernet connections to an EMC Symmetrix storage array. Perhaps at a cost of $5,000 to $10,000 per connection (2003 dollars). Load balancing I/O requests among those 8 exotic connections.

Perhaps my (3 years and younger) grandkids will see 10Gbit as their default network connections…Some day.

(Note: $1 in 2003 is $1.67 today)

Amazing, isn’t it?

Quite.