It took a long, long time to convert the old IBM PC business acquired in 2004 into the dominant supplier of client devices in the world, but Lenovo is nothing but not patient and bypassed HP Inc in 2013 and has had the largest share of the market since that time. And now, according to the company, Lenovo has retaken the third place position in servers in the most recent quarter and is gaining share in a somewhat soft datacenter infrastructure market.

For the longest time, IBM was the dominant seller of servers, thanks to a combination of mainframe, RISC/Unix, and X86 server sales. Hewlett Packard Enterprise caught up with IBM in the late 1990s and had to buy Compaq in the early 2000s to hold that share. Sun Microsystems peaked in the early 2000s with the Dot Com boom and Dell had almost no server business at all at the time compared to these three companies, but has grown steadily, like clockwork, over the decades and IBM shrunk immediately and significantly in late 2014 when it sold off its System X X86 server business to Lenovo for a pittance. (Much as it did with its PC business.)

In server revenues, Dell caught up to and passed HPE in late 2018 just as Inspur caught up and passed Lenovo, pushing HPE down to number two for several quarters and pushing Lenovo down to number four. Dell and HPE continue to jockey for position and Lenovo and Inspur continue to as well, as far as we can tell from the limited data we get to see out of market researchers these days. (Both Gartner and IDC stopped making summaries of their server and storage sales data public in Q3 2021.)

This year, Lenovo opened up factories in Monterrey, Mexico and Budapest, Hungary and pushed hard with a new sales team and marketing strategy called NextWave, focusing on the – you guessed it – the next wave of hyperscalers and cloud builders and reaping big rewards in terms of server – and storage – sales.

We think companies that can use their market position to have better leverage over the semiconductor supply chain are doing better, and we also think it is no accident that Supermicro, which is based in the United States, and Lenovo, which is half American and half Chinese with a big presence and history in Europe thanks to Big Blue, are both skyrocketing in growth even as the server market is in a bit of the doldrums as 2022 came to a close and will persist perhaps through the first half of 2023. Inspur rode up the cloud expansions of Chinese hyperscalers Alibaba, Baidu, Tencent, but each of these companies have their own challenges and tend to binge eat and then digest. Having 25 megascalers buying most of the time is better than having three hyperscalers buying a lot at the same time and then slamming on the brakes for two quarters.

The NextWave strategy also includes what Kirk Skaugen calls ODM+, and it is an advantage that Supermicro and Inspur also leverage. Skaugen is president of Lenovo’s Infrastructure Solutions Group for more than six years and the former general manager of Intel’s Data Center Group and its Client Solution Group for many years before that. (And during some of what seemed, at the time, like Intel’s toughest years. But 2021 through 2025 will turn out to be harder than 2008 through 2012, which was no joke.)

“In a broad sense, the overall total available spend is probably down,” Skaugen explained on a call with Wall Street analysts going over the financial results for Lenovo Group’s third quarter of fiscal 2023 ended in December and in response to a question about capital spending by the hyperscalers and cloud builders having tempered budgets. “However, largely Lenovo is immune to those trends and I will give you some color on why. Obviously, we just announced a record in our cloud business. And for many quarters I’ve been talking about our new ODM+ model, where we’re delivering custom designs for the largest hyperscalers in the world. Those designs have been ramping for many quarters – and not just in the server space but we’re also expanding very aggressively into the storage space as well. So despite the fact that the total market of spend might be down, Lenovo has definitely known for many years and the last several quarters that we’ve gotten the designs for those motherboards, those systems, and those racks because we’ve been designing those in for the last year plus at least.”

Skaugen also said that Lenovo is also expanding its systems business by diversifying its CPU portfolio out beyond Intel Xeon Ds and Xeon SPs to include AMD Epyc X86 processors as well as Ampere Computing Altra Arm server CPUs. Skaugen also said that this is “fresh order load,” not just Lenovo having a backlog of server and storage orders that it can now fulfil.

And the ISG business is up on all fronts. Servers and storage set new records, according tp Skaugen, and the cloud and the enterprise/SMB segments both set records, and within storage, hyperconverged storage, cloud storage, entry storage, and midrange storage all set records. The business outside of China set records, and North America and Europe were “particularly strong” within this slice of the ISG business.

Whatever is going on, it is still going on here in the first quarter of 2023, and Skaugen thinks that Lenovo can deliver nearly 50 percent growth year on year in the coming quarters, driving share gains in servers and storage, while also expanding operating profits.

Lenovo has a ways to go to catch Dell and HPE, and Skaugen said as much. But that is clearly the goal, and having a Sino-American company with fairly local manufacturing in North America and Europe will help. Inspur will have a harder time replicating this, and Supermicro already does the same with operations in the United States, the Netherlands, and Taiwan.

Dell’s Infrastructure Solutions Group booked $38.1 billion in sales for the trailing twelve months through October 2022, which is the most comparable data we have at the moment. Lenovo just did $8.96 billion in its trailing twelve months ended in December 2022. In four years, if Dell stays flat, Lenovo will catch it just shy of $40 billion. If Dell grows at 10 percent, it will take a little more than five years for Lenovo to pass Dell if it can grow at, say, 45 percent per year.

Which vendor is limited in China? It ain’t Lenovo. Which vendor is selling into at least some hyperscalers and big cloud builders? It ain’t Dell.

Maybe IBM should have bought Lenovo and Red Hat back in 2015. . . .

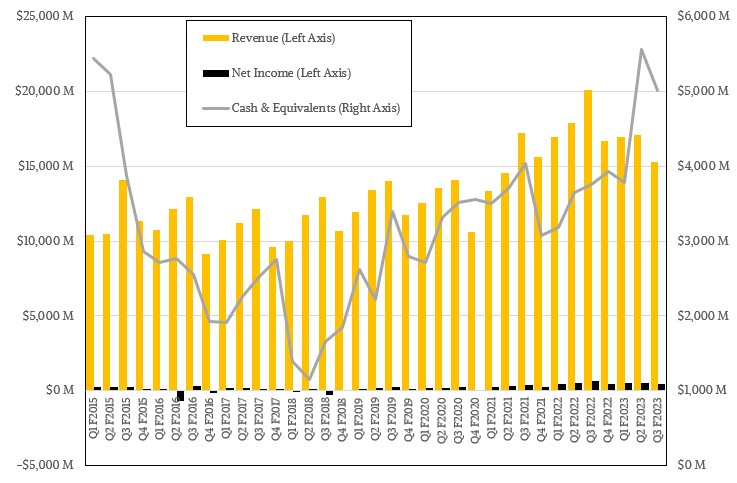

Anyway, in the quarter ended in December, thanks to a post-apocalyptic post-COVID collapse in the PC market, which we do not think will completely revive as many (including Intel) think it will, Lenovo’s revenues fell by 24.2 percent to $15.27 billion and net income was down by 31.7 percent to $437 million. (Net income as a share of revenue was 2.9 percent, which is not much lower than the average for the past two years.) Interestingly, Lenovo ending the quarter with over $5 billion in cash and equivalents, a third more than it had a year ago, so it has some maneuvering room to make investments in the years ahead. (But make no mistake, it does not have anywhere close to the kind of cash hoard that the biggest or richest tech companies enjoy. They are often sitting on one, two, or three quarters worth of revenues, and Lenovo is sitting on what is a 33 percent of a quarter’s worth of revenue in the new market and a 25 percent of a quarter’s worth of revenues in the pre-PC collapse market.)

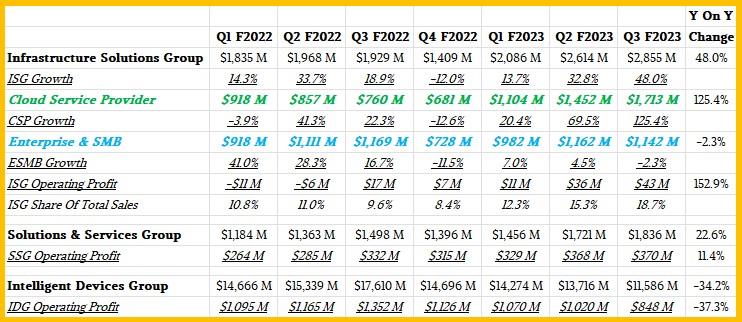

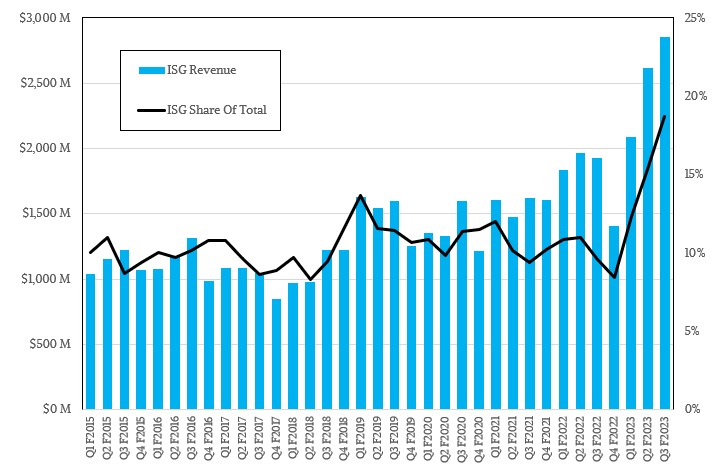

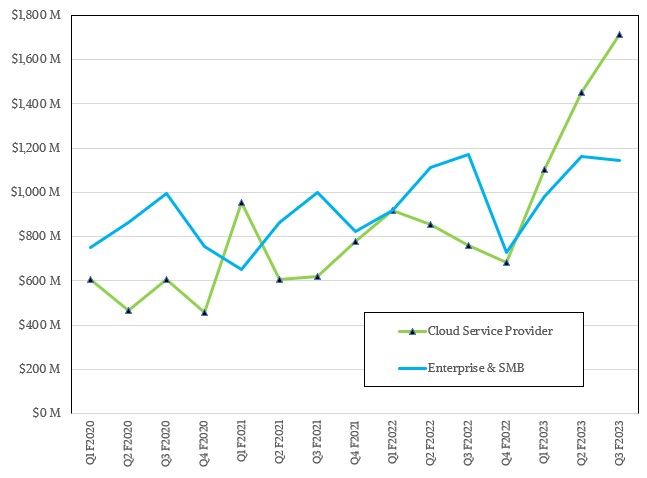

The Infrastructure Solutions Group had revenues of $2.86 billion, up 48 percent. Based on charts given out by Lenovo, we estimate that Cloud Service Providers represented $1.71 billion, up 2.25X year on year, and sales of servers and storage to Enterprise & SMB customers represented $1.14 billion, down 2.3 percent. ISG operating profits were up by 2.5X to $43 million – still very little money, mind you, considering the effort, but someone has to make our servers and storage, so send all of your OEMs and ODMs Thank You notes.

The profits will grow in the absolute as Lenovo grows the ISG business, but we doubt it can get much more profitable than it is. Lenovo’s competitors in China, North America, and Europe will not allow it and the competitive pressure will continue to be high.

Just ask Dell is this gets easier or harder once you are on top.

When Lenovo acquired IBM’s PC business in 2005, the action raised alarm because it potentially could allow the Chinese government access to confidential military data. Lenovo vigorously defended their independance.

Sadly, it was discovered in that shortly afterwards in 2008 an encryption chip was incorporated that relayed data back to China.

Then, the DoD had to purge IBM servers after that purchase for the same reason, as was done with Supermicro.

https://www.bloomberg.com/features/2021-supermicro/

Thus, I cannot endorse widespread growth in the server business for security reasons.