Here is a question for you: If hypervisors are going to eventually be offloaded to a DPU attached to the server node by a PCI-Express link, is the server considered bare metal or virtualized? If the DPU is not physically present in the server but hooked to the server over a PCI-Express switch fabric, doesn’t the answer change?

Here is another question: Is a mainframe or Unix server running legacy applications in hardware or software partitions an example of “cloud” infrastructure or not? Or do you have to have other functions, such as metered usage and tracking, live migration, and other features to be called cloud infrastructure? And if these “non-cloud” servers and storage are not bare metal in the strict sense, what are they?

We don’t have precise answers to these questions as we ponder the latest statistics coming out of IDC concerning sales of cloud and non-cloud server and storage infrastructure, and the organization’s taxonomy does not make this clear. But we can see how IDC is characterizing sales of server and storage infrastructure combined, which is useful, and how much cloud infrastructure is being deployed in “dedicated clouds” used exclusively by enterprises (on premises or in co-location facilities) and how much is being deployed in service provider utilities that many call “public clouds” and that IDC calls “shared clouds.”

This is interesting data nonetheless, or we would not bring it up. Particularly since IDC and Gartner both decided last year to not make any of their server and storage market research available to the IT public any more. (Much to our chagrin.) This dataset, which is still available, gives us some insight, and is interesting in that it eliminates the redundancies in the old server and storage trackers from IDC. A lot of the servers were for storage, and if you added the server data to the storage data, there would be some double counting that made the resulting overall system market look bigger than it actually was. So this is also interesting inasmuch as we have a better sense of the hardware spending on datacenter infrastructure.

Sorting through all of this data and eliminating the duplication takes time, and so we are only now getting a look at compute and storage spending for the first quarter ended in March. Here is what the spending looks like for infrastructure hardware since the first quarter of 2020, a year before this spending model was first introduced by IDC:

Instead of talking about public cloud, private cloud, and non-cloud IT spending, the updated model talks about shared cloud, dedicated cloud, and non-cloud IT spending. Shared cloud means spending on infrastructure that is installed at cloud service providers that are multitenant and have thousands to millions of customers sharing that infrastructure. (This is not the value of the IaaS services sold by those clouds to customers, but what they bought in iron during the quarter.) Dedicated cloud can mean cloud-style infrastructure installed on premises in an enterprise or installed at co-location facilities. Non-cloud IT is all of that legacy stuff, and we are still awaiting clarification on precisely where the lines are drawn.

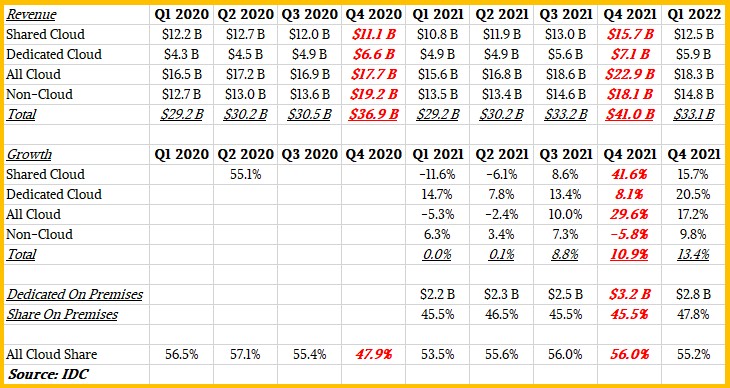

Let’s walk through the numbers. According to IDC, $33.1 billion in compute and storage infrastructure was sold in the world, an increase of 13.4 percent from the year ago period. Spending on shared cloud compute and storage capacity came to $12.5 billion, up 15.7 percent, while spending on dedicated cloud was only $5.9 billion, but up 20.5 percent. Of this dedicated cloud spending, a little less than half of it was for on-premises gear; the rest ended up in co-location facilities of some sort. Add it up, and total cloud infrastructure spending came to $18.3 billion, up 17.2 percent year-on-year.

Non-cloud infrastructure – all of that legacy stuff – still drives a lot of revenues, and accounted for $14.8 billion in sales in Q1 2022, up 9.8 percent. This part of the business is still growing, mind you, it is however growing slower than the rest of the infrastructure market and thus its share of the overall infrastructure pie is dropping.

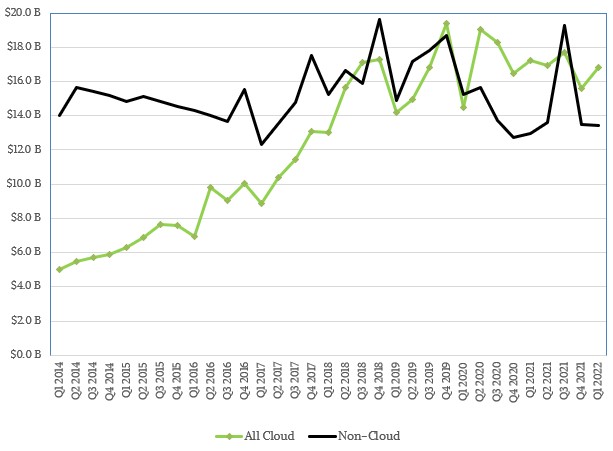

As you can see from the table, there is an ebb and flow to spending, with the fourth quarter being bigtime spending as it has been historically since there has been an IT business. What you can’t see from that table is just how jumpy and bumpy those spending trends are for cloud and non-cloud infrastructure. And so we dug out the old IDC data going back to 2014 and paired it with the new IDC data starting in 2020, and this is what it looks like:

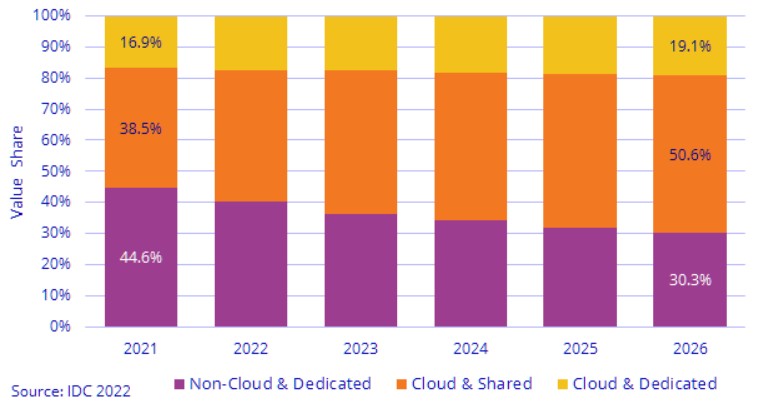

If you average the non-cloud spending out, it is somewhere around $16 billion a quarter, and to our eyes, the spending on cloud is a little bit higher. But both are wonky, with big swings quarter to quarter. That said, IDC has contended for years that spending on non-cloud infrastructure will represent a smaller and smaller piece of the pie, and here is the latest forecast out to 2026:

By 2026, IDC expects for shared cloud spending – what many people call public cloud but which we no longer do because the clouds are not public utilities, but privately run ones without the kind of government regulation as electric and gas companies here in the United States have to yield to because they are essentially monopolies in their operating regions – to finally break through the 50 percent barrier. Dedicated cloud will grow its share, too, to about a fifth of the market, leaving a little less than a third for non-cloud infrastructure spending.

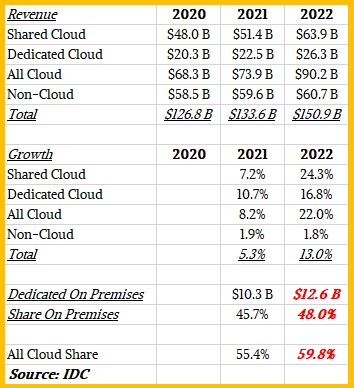

Looking ahead to the rest of this year, IDC supplied a forecast that encompasses all of 2022, which you can see below compared to shared cloud, dedicated cloud, and non-cloud IT spending for 2020 and 2021:

Shared cloud spending is expected to rise by 24.3 percent to $63.9 billion for all of 2022, and dedicated cloud spending is forecast to rise by 16.8 percent to $26.3 percent. Add it all up, and cloud compute and storage infrastructure will comprise $90.2 billion in sales, up 22 percent. And non-cloud compute and storage spending will even grow this year, rising 1.8 percent to $60.7 billion, if IDC is right. And that puts overall compute and storage spending worldwide across all deployment models and types at $150.9 billion, up 13 percent.

By the way, looking out to that 2026 forecast further out, spending on shared and dedicated cloud infrastructure together will comprise $145.2 billion, according to IDC, almost as large as the total datacenter infrastructure market in 2022. And non-cloud infrastructure will be driving $63.1 billion in sales – a tiny bit more per year but still growing, not declining at all.

What about the cloud internal? CSPs like Google, Microsoft etc. have substantial internal consumption that is not shared cloud.

Is that dedicated and cloud?

Dedicated cloud seems to be enterprise on-prem and colo. So not cloud internal which is a pretty substantial chunk and seems to be missing.

Hard to understand how “dedicated cloud” vs non-cloud is a meaningful distinction. It’s mainly about the OS installed, not the hardware. I mean, onprem vs colo would be more meaningful.

So we either have cloud (someone else’s computer, that is multitenant) and dedicated. But these report-writing companies need something to bulk up their report$…