It’s a great thing when an upstart supplier of hardware or software lands one of the hyperscalers or large public cloud builders on Earth as a customer. It is an instant validation of strategy and products, and that can open a lot of doors. But it is not necessarily a high profit endeavor, and companies count on leveraging that customer win – or wins if they are lucky – to widen out to smaller service providers and large enterprises that will pay (they hope) a hefty premium for their wares.

This has certainly been the case with Arista Networks, which is moving out of the upstart phase after a decade of commercial sales and which has been gradually deepening its engagements with a broader number of customers while at the same time expanding out from its initial datacenter Ethernet switching business based on merchant silicon out to campus switching and now datacenter routing. But when one of those hyperscale customers pulls back, it hurts. As does, we suspect, the increasing adoption of cross-platform switching and routing software stacks – which run on a number of different ASICs – from Arrcus, DriveNets, IP Infusion, Volta Networks, and others on whitebox switching and routing gear.

Without a doubt, Microsoft, which has been building its Azure public cloud at a feverish pace for more than a decade, has been the cornerstone customer for Arista Networks, and has been “a greater than 10 percent” customer, in terms of share of annual revenue, since the upstart was founded in 2008 by Andy Bechtolsheim, David Cheriton, Ken Duda, and Jayshree Ullal. Social network giant Facebook has also been a big customer in recent years, too.

Microsoft peaked at 27 percent of Arista Network’s revenues in 2018, and Facebook peaked in 2019 with 16.6 percent of revenues. Coronavirus pandemic or not, Microsoft and Facebook have been buying lots of infrastructure, but Microsoft cut its spending at Arista Networks by 10.1 percent in 2020, to $498 million, and Facebook cut it by 50.9 percent, to $165 million. Something is up. That is a $227 million hit to the top line at Arista Networks compared to levels if these two giants had kept spending at 2019’s rate. Facebook has apparently decided to skip the 200 Gb/sec generation, and that is part of the issue, but it will be moving to 400 Gb/sec gear.

The good news, no matter what is going on at Facebook, is that Arista Networks has been adding to its customer base at an increasing rate, rising from around 1,100 customers in 2011 (only two years after dropping out of stealth mode) to over 7,200 as 2020 came to an end. Last year was a challenging time for a lot of IT hardware and software suppliers, and Arista Networks was not exception.

Don’t be worried. Arista Networks has some of the smartest people in networking on the bridge, steering a course to take market share away from arch-rival and datacenter and campus networking juggernaut Cisco Systems, where all of the company’s founders have worked in different capacities over the several decades. And with $2.87 billion in cash in the bank, lawsuits with Cisco in the rear view mirror, and a return to more vigorous spending on deck for the first quarter of 2021, it is steady as she goes for Arista (which, you will note, has a logo font very much reminiscent of the Star Trek franchise.) This particular enterprise is on a 30-year mission, and it is more than halfway there.

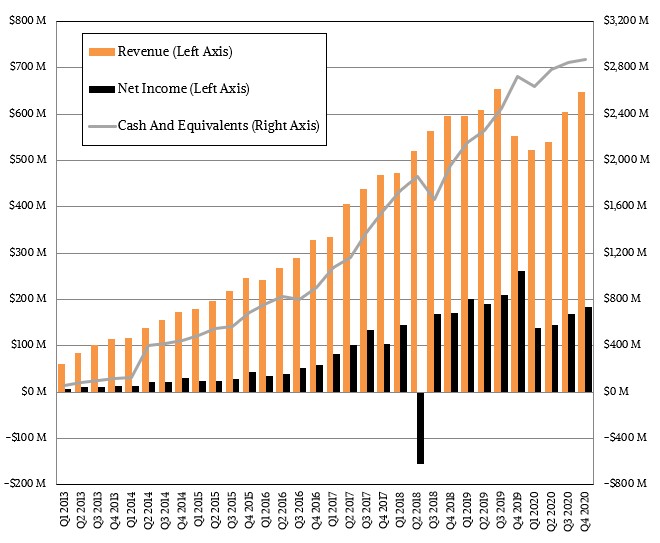

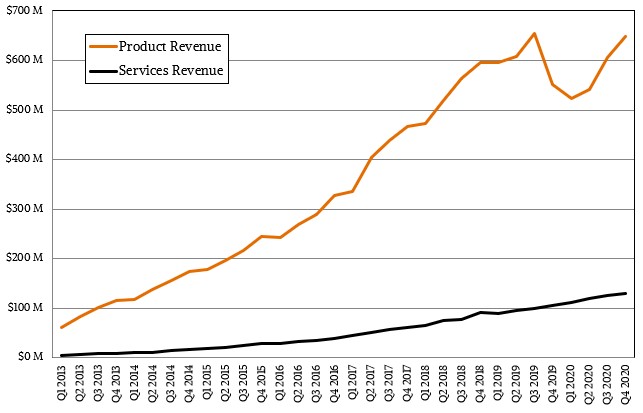

Let’s review the latest financial results out of Arista Networks and then let’s talk about that mission. In the quarter ended in December, Arista Networks posted $518 million in product sales, up 15.8 percent, and services revenues of $130 million, up 23.9 percent. Combined revenues added up to $648 million, up 17.4 percent. However, costs were up on all fronts – some is due to supply chain issues most IT equipment makers are wrestling with, some is due to increased investments in research, development, marketing, and sales – and that drove net income down by 29.8 percent to $183 million.

This level of income – 28.2 percent of revenues – is absolutely consistent across several years of Arista Networks’ recent history, and if anything, Q4 2019 was considerably more profitable than is typical, thanks to a $73.5 million benefit for a refund on income taxes from the US government, making for a hard compare this time around. The company added $149 million to its coffers as Q4 2020 came to a close, and that is a win.

Drilling down into the business a little deeper, management at Arista Networks believes that somewhere between 60 percent and 65 percent of the company’s sales will come from its core datacenter switching hardware in any given quarter, with its software and services (both available as subscriptions) comprising somewhere between 22 percent and 25 percent of sales. (Perpetual software licenses, such as those for its Extensible Operating System networking variant of the Linux operating system, are counted in the hardware revenues to which they are tied.) That leaves somewhere between 10 percent and 15 percent of revenues coming from the new adjacencies of campus switching and datacenter routing.

Breaking it down by market sector and geography, somewhere between 35 percent and 39 percent of revenues came from what Arista Networks calls “cloud titans,” which is what we call hyperscalers mixed with large public cloud builders. (Some companies, like Google and Microsoft, are both, some like AWS are increasingly becoming both, and still others like Facebook are just hyperscalers and do not sell compute, storage, and networking capacity as a cloud offering.) Service providers, including the telco giants and niche cloud builders, represent somewhere between 25 percent and 30 percent of revenues, and the remaining 35 percent to 39 percent of Arista Networks’ sales comes from what it calls enterprises, and that is heavily skewed to financial services firms that have been its customers since Day One.

For the full year, product sales were off 9.4 percent to $1.83 million, services sales rose by 24.9 percent to $487 million, and overall sales were down 3.9 percent to $2.32 billion. Net income fell by 26.2 percent to $635 million, but again, that tax benefit in 2019 helped a lot here and made for a tough compare.

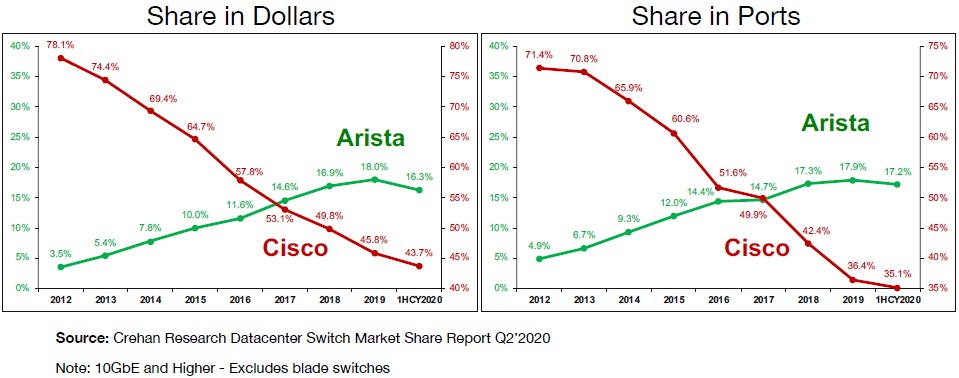

Arista Networks has certainly been taking a bite out of Cisco. Look at this data from Crehan Research, which shows revenue and port count for datacenter switching sales from 2012 through the first half of 2020:

Cisco has been bleeding market share in revenues and ports, and Arista Networks has captured about half that. The whitebox switch vendors have captured most of the rest, we think. There is some chance that Silicon One is helping level off this bleed rate – time will tell. And if customers start pushing for Silicon One ASICs, the two companies could bury the hatchet and Arista Networks could port EOS to Silicon One and deliver its stack on these ASICs for both switching and routing. There is bad blood between these two companies, but not so much that they won’t make money and not so much that Cisco would love to cut off the oxygen of Broadcom just a little if possible. That is, after all, what Silicon One is supposed to do.

“Despite a turbulent 2020, especially with cloud titans, we believe Arista is going to emerge stronger with more diversified products and customers,” said Ullal on a call with Wall Street analysts going over the figures. The company expects revenues of between $630 million and $650 million in Q1 2021 and for gross margins to range from 63 percent to 65 percent of revenues – which is about as good as it gets in the IT hardware racket.

“The networking industry is undergoing a metamorphosis from point silos or places in the network to a seamless cognitive cloud network that is data driven,” Ullal continued. “Arista is helping customers with their digital transformation to this data-centric, cloud-first paradigm. As we experience the explosion of users, devices, and IoT – with more video, more mobility of workloads and workflows – the boundary between all the locations, whether it is your office, cloud, home, teleworker and transient user, is really blurring into elastic workspaces. We believe Arista is well-positioned to address the data-driven networks for these client-to-cloud workspaces. We are powering some of the world’s largest datacenters and cloud providers as a trusted partner. And this expertise that we have gained has helped us modernize networking to a software-driven cognitive experience.”

Arista Networks got its start when 10 Gb/sec Ethernet switching started to take off in earnest a decade ago, and started out on merchant silicon (PivotPoint and FocalPoint) from Fulcrum Networks (acquired by Intel about a year later) and “Trident” StrataXGS ASICs from Broadcom. Since then, Arista Networks has adopted the “Helix and “Jericho” and “Tomahawk” ASICs from Broadcom, the XPliant ASICs from Cavium (now part of Marvell), and the “Tofino” ASICs from Barefoot Networks (now part of Intel, too) in its datacenter switches; the Jericho ASICs, which have deep buffers instead of high bandwidth, and their companion Qumran fabric interconnects are ganged up to make routers. It would be surprising to see Arista Networks ever adopt Cisco’s Silicon One ASICs for either routers or switches, but Innovium Teralynx ASICs are an option for extreme bandwidth aimed at hyperscalers.

In the call with Wall Street, Ullal said a few interesting things. First, there were six EOS releases across 40 switch and routing platforms in 2020, and 800 features relating to routing were added to the software. Moreover, Arista Networks added more than 200 customers just for routing last year. The company now has over 1,000 customers using its CloudVision telemetry software, which is a few years old. As for the cloud titans, Ullal attributed the issue to delayed qualifications for 400 Gb/sec Ethernet gear. Ullal expects to see 200 Gb/sec and 400 Gb/sec ramps at the hyperscalers and cloud builders – she did not name names – in the second half of this year. So far, only 75 customers have rolled out 400 Gb/sec equipment among the more than 7,200 customers. A little more than 1 percent, and a little more than 98 percent to go . . . .

We will be watching this new battle over datacenter routing – and the ongoing war for datacenter switching – with great interest.

As for the campus switching market – which is only significant to us because it gives Arista Networks a revenue stream outside of the datacenter – Ullal said the target was to have at least $100 million in sales in 2020, and the company apparently exceeded that target.

Supply Chain Easing Creates Ethernet Switching Boom

There are a lot of things going on in the datacenter and campus interconnect markets, but one of the weirder things we observe from the most recent market data coming out of IDC about the Ethernet portion of this market is that it is like a country music record being …

Like A Drumbeat, Broadcom Doubles Ethernet Bandwidth With “Tomahawk 5”

If there is anything that hyperscalers and cloud builders value more than anything else, it is regularity and predictability. They have enough uncertainties to manage when it comes to customer demand that they like for their systems to behave as deterministically as possible and they like a steady drumbeat of …

Innovium Stays On Broadcom’s Heels With Teralynx 8 Switch Chips

There is a relentless hunger for bandwidth in the largest datacenters of the world as well as a desire to flatten networks and thereby reduce latencies and the cost of the networks that interconnect servers and storage to provide modern applications. In the past decade, competition has been good in …

Be the first to comment