As 2023 has progressed, the revenue growth projections at Arista Networks have inched up as its supply chain issues are getting resolved. Three months ago, Jayshree Ullal, the company’s chief executive officer, said that the company was raising its guidance to 30 percent growth, up from a 25 percent forecast that it gave out in January, and now, as it wraps up the third quarter ended in September, Arista is saying that it can actually grow by around 33 percent here in 2023.

Some of this growth is just the transition of enterprises from aging 10 Gb/sec ports to 100 Gb/sec ports, which are now cheap enough for regular companies to get a speed bump like that have not seen in maybe a decade and a half. (The Ethernet roadmap is supposed to move faster than this, but sometimes the bit hits the fan.) Some of it is the adoption of 400 Gb/sec and 800 Gb/sec leaf/spine architectures to build out AI and sometimes HPC clusters. And some of it is as datacenter interconnects, which lash compute and storage within regions of the big cloud builders and hyperscalers together, move from 400 Gb/sec to 800 Gb/sec backbones.

And Arista, which is somewhat akin to the Supermicro of networking in that it shoots the gap between the OEMs and ODMs, has been able to grow like crazy since it dropped out of stealth in 2011 as the flag bearer of the open networking and merchant silicon movements in datacenter networking.

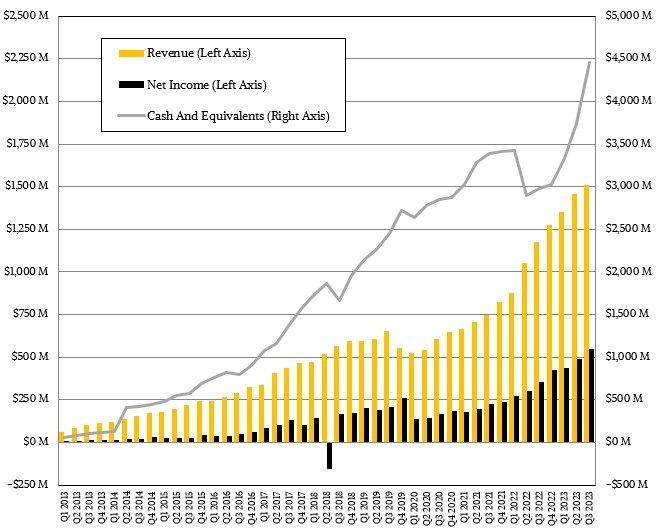

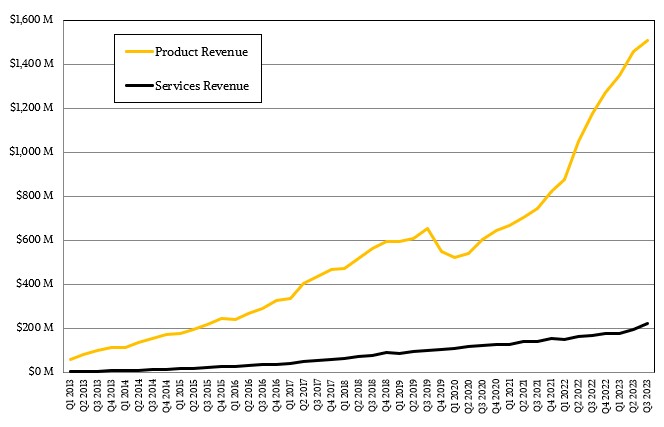

In the quarter ended in September, Arista had $1.29 billion in product sales, up 27.4 percent and services revenues of $223.9 million, up 33.2 percent. Add it all up and revenues were $1.51 billion, up 28.3 percent. Net income for the company was $545.3 million, up an amazing 54 percent year on year and comprising 36.1 percent of revenues.

That high ratio of income to revenue shows you the value of the software and services that Arista adds to the merchant silicon on which it builds its switching and routing platforms.

Software subscriptions drove $29.7 million in sales, up 25.2 percent, and the combined software and services category – which are both sold under a subscription-style pricing scheme like cloud compute and storage – comprised 16.8 percent of revenues and rose by 32.2 percent to $253.6 million. This subscription part of the Arista business has doubled in three years (we don’t have data all the way back into early 2020, but that is what it would look like if we did.)

Arista ended the quarter with $4.46 billion in cash and equivalents, which is a plenty big enough cash hoard to do all kinds of interesting acquisitions and to weather any potential economic storm that might tear the sails of economic activity in the datacenter. The company is still sitting on over $2 billion in customer purchase commitments, which is down from the $4.3 billion it had in the year ago period.

Those commitments were made, of course, because hyperscalers and cloud builders wanted to mitigate the risks in the IT supply chain and as a consequence they had to actually tell Arista what they were doing and what products they needed – and when. As the supply chain stabilizes, the visibility that Arista enjoyed during the pandemic and after it will return to the fog that it was used to for the first decade of its experience selling networking gear.

But for now, AI networking is so important that Arista will have some enhanced visibility in this area, and particularly as the members of the Ultra Ethernet Alliance (of which Arista is a founding member) work together to make Ethernet competitive with InfiniBand for AI networks and, of their goals are achieved, more scalable to boot.

AI is also now so important to Arista’s customers that it is merging sales of networking for AI clusters and sales of networking to what it calls Cloud Titans (what we call hyperscalers and cloud builders) together into a new category called the Cloud and AI Titans. What we didn’t know is that Arista had a very formal definition of Cloud Titan and it was that it had more than 1 million servers installed. And as it turns out, Apple was considered a Cloud Titan but apparently is not one anymore and is being degraded down to a Cloud Specialty category (presumably meaning fewer than 1 million servers in the fleet) alongside the Tier 2 service providers. Oracle, with its Oracle Cloud Infrastructure (OCI) cloud, is making big investments in AI and also apparently has a fleet with over 1 million servers and is now a Cloud and AI Titan and, not surprisingly, is also an Arista customer. It would be interesting to see if and how Oracle, which has been such an ardent supporter of InfiniBand for its database clusters over more than a decade and which has even been an investor in Mellanox, makes use of enhanced Ethernet for its AI networks. These Cloud and AI Titans are expected to comprise more than 40 percent of Arista’s sales in the coming years.

One last thing. If you do the math on Arista’s projections for 33 percent growth in all of 2023, then the company will bring in around $1.51 billion in sales in Q4 of this year – pancake flat from Q3 sales – and $5.83 billion for all of 2023. Beyond that, Arista is expecting a presumably more normalized “double digit” revenue growth in 2024 and the years beyond. Of course, double digit is intentionally vague, and can be anywhere between 10 percent and 99 percent growth. . . .

We will just have to see how it all plays out.

I love the idea of Arista and SuperMicro systems in any small(ish) HPC cluster for an engineering focused team. You want the fastest gear at the cheapest price and you don’t need all the feel good features of the HPE or Cisco crew, you just need the basics done well and which let you get the job done.

So many people seem to love Cisco or HPE/Dell since they’re terrified of making a purchasing mistake or getting outside their comfort zones.

I pushed the SuperMicro FatTwin systems about 8 years ago for my $WORK and they turned out great. Reliable, easy to manage, and without the crap extra features (like HPE wanting extra money for remove console AFTER the OS boots. Thieves they are!) which just get in the way at scale.

So if the big cloud guys are buying these, it tells you Arista is focussed on just the features needed to be useful and remotely manageable and scalable. Which is a great for even a small shop with just a few of them, since it frees up time for other more fiddly bits.

Well said, John.

Interesting analysis (and also the recent ones of AMD, AWS, Intel, TSMC, plus the 08/16/23 Supermicro)! I wonder if plotting some curves (eg. Revenue) in semi-log form (eg. log(Revenue) vs quarter) may help tease-out some of the factors contributing to those evolutions (essentially assuming an underlying exponential growth, and looking for deviations). The early-COVID boost in datacenters, late-COVID trough, current recovery, and imminent AI-related growth, might be more readily identifiable on such semi-log, relative to longer-term trends (or not).

There could also be some opportunity for multi-species modeling of the supply chain, maybe in Lotka-Volterra style, with fabs (TSMC, IFS, …), chipmakers (Intel, AMD, …), boxers (Supermicro, Arista, …), and eventual consumers (AWS, …). Fabs might be seen as autotrophs with others representing heterotrophs at higher levels of the “food” web. Inspiring stuff!