Taiwan Semiconductor Manufacturing Co is the world’s largest and most advanced producer of semiconductors, and is therefore a “bellwether” for the semiconductor industry and, in turn therefore, a leading indicator of the entire IT sector that depends so heavily on semiconductors as its key driver.

A bellwether is supposed to be the lead sheep in a flock, and is called that because it has a bell around its neck so it can be identified by the shepherd and also by the sheep following it. It is not the bell that makes the sheep special, but rather the special sheep that correctly leads the pack that warrants the bell, which creates a virtuous cycle that helps manage the flock.

TSMC is then, perhaps, a super sheep and a hyper bellwether because it expects to be able to grow throughout a contracting semiconductor market here in the second half of 2022 and the first half of 2023. And the fact that TSMC thinks it can grow during a decline shows just how far ahead of the competition TSMC is when it comes to the etching and packaging of CPUs, GPUs, FPGAs, and custom ASICs.

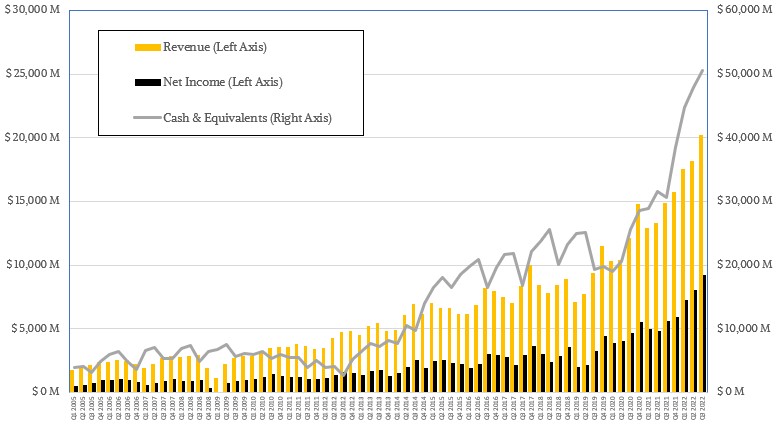

In the quarter ended in September, revenues at the Taiwanese foundry rose by 35.9 percent to $20.25 billion, and net income rose an even faster – and amazing – 65.1 percent to $9.27 billion, representing an incredible 45.8 percent share of revenue.

TSMC is throwing off the kind of profits that Intel’s Data Center Group did between 2010 and 2018, and if it was not so hard to build up the expertise in advanced chip manufacturing and so expensive to build chip factories, we would say such profits would sow the very seeds of competition. But in this case, the growth and profitability of TSMC over the past decade has had the opposite effect, compelling foundry after foundry to fold or focus on older processes. Which is how we are down to TSMC, Samsung, and Intel as the three foundries committed to the advanced chip making processes that are key to the compute and networking engines that are the very foundation of the datacenter. Four if you count the aspirations of China’s Semiconductor Manufacturing International Corp.

TSMC knows that it needs mountains of money to set the competitive pace in chip etching and packaging, and so the company’s top brass completely shrugged off the idea of instituting share buybacks with the stock being hammered over concerns about chip and chip making export controls imposed by the United States on China and a malaise in the gaming and cryptocurrency mining parts of the GPU business and the PC part of the CPU business. TSMC has no intention of doing share buybacks at this time, which shows it is a sane, long-term player and not looking to make a quick buck for shareholders as the Intels and IBMs of the world are apt to do. It is going to need every penny of its $44.3 billion cash and investment hoard, and then some.

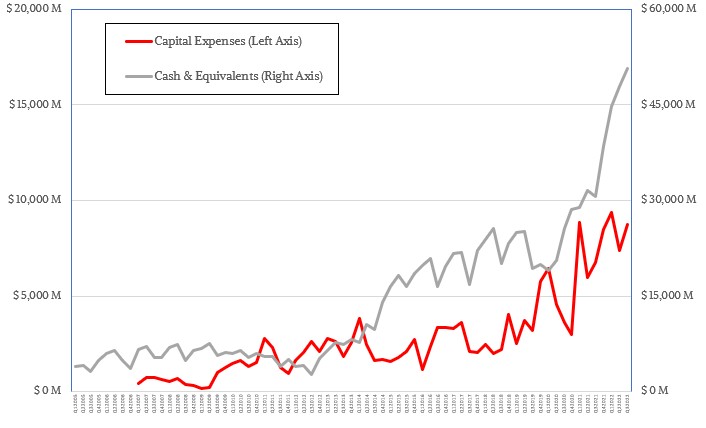

The cash pile is growing faster than the rate of inflation on the price of a fab (we think), so that is good. But all of that hard-earned money might only build three or perhaps four new fabs, and TSMC is building a new fab right now in Arizona in the United States and expanding one in Kumamoto in Japan and expanding two others in Nanjing and Shanghai in China.

You get what you invest in this world, and not a damned thing more – excepting the occasional lucky strike. And in Q3 2022, which was a jumpy one in the semiconductor industry, TSMC’s capital expenditures rose by 29.2 percent to $8.75 billion. The company paid out $4.5 billion in dividends in the quarter, and is sitting on $26.5 billion in debt in the form of bonds. Its balance sheet is about as strong as any we have seen in the technology racket.

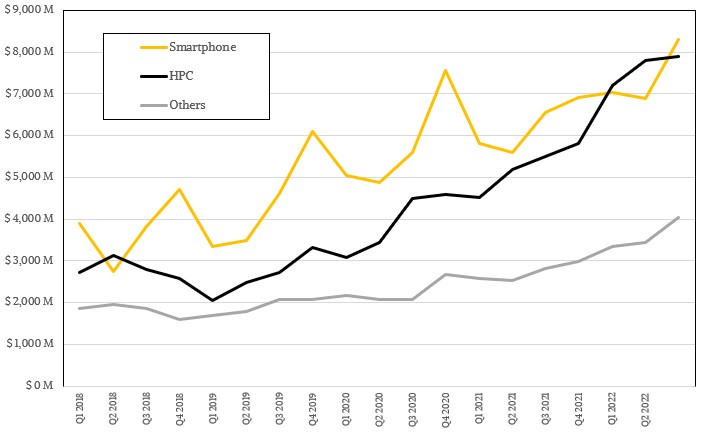

In recent quarters, thanks to the growth of what TSMC calls its HPC business – which includes CPUs, GPUs, FPGAs, and custom ASICs – has been growing a lot faster than revenues and much faster capital expenditures. This is what happens when you don’t indulge in tangential acquisitions and forget that you are an advanced foundry that has to hedge its technology bets so it can meet roadmap commitments. When Intel messed up its foundry roadmap, it only had one captive customer – Intel itself – to disappoint. If TSMC screws up, customers will start looking at Samsung and Intel, and if it screws up enough, they will abandon TSMC for Samsung and maybe after a few years Intel.

TSMC has had difficulty with some manufacturing nodes – 28 nanometers, 10 nanometers, and 3 nanometers – but it seems to have gotten its 3 nanometer processes under control just in time for it to start capturing the most advanced chip designs beginning next year.

On a call with Wall Street analysts going over the third quarter numbers, CC Wei, chief executive officer at TSMC, said that the growth 5N nanometer nodes used in the manufacturing of a lot of smartphones, CPUs, GPUs, and switch ASICs these days more than counterbalanced a slowdown in the 7N nodes used on prior generations of chippery, including a lot of PC chips that have seen a slowdown as the client device market has slowed dramatically in recent quarters. The N7 and related N6 refined process, in fact, will not be seeing the same foundry capacity utilization as has been the case for the past three years as this was the advanced node in production, and Wei said further that this slump for N7 and N6 production would persist through the first half of 2023.

“We believe the N7 and N6 demand is more a cyclical issue rather than structural, and we expect our N7 and N6 demand to pick up in second half 2023,” Wei explained. “Longer term, we continue to work closely with our customers to develop specialty and differentiated technology and are confident to drive additional waves of structural demand to backfill our N7 and N6 capacity over the next several years. The 7 nanometer family will continue to be a large and long-lasting node for TSMC.”

When TSMC says long lasting, it ain’t kidding. The company still makes chips using 250 nanometer and larger geometries, and chips using 16 nanometer or larger processes still make up 46 percent of revenue. These nodes persist, and get more profitable over time as they mature.

In the third quarter, 5 nanometer nodes accounted for 28 percent of revenues and 7 nanometer accounted for 26 percent; the shares of the older nodes don’t change that quickly, but 7 nanometer and 5 nanometer have clearly crossed in the night.

The HPC segment accounted for $7.89 billion in sales, up 43.3 percent, and chips the Smartphone segment accounted for $8.29 billion, up 26.7 percent. As you can see from the chart above, the HPC segment has been rising steadily, and we think will eventually permanently surpass the Smartphone segment as the top revenue generator for TSMC. The other segments, which include IoT, Automotive, Digital Consumer Electronics, and others are growing for the most part, but are still even collectively dwarfed by these two major segments.

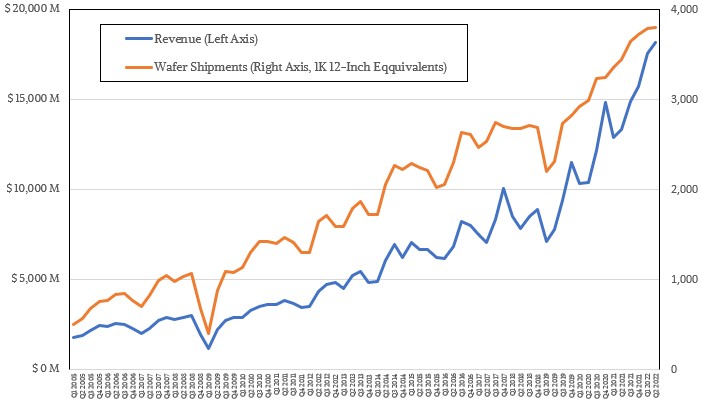

In general, there is a correlation between wafer shipments and revenues, but these go up and down at different rates. What can be said is that TSMC had wafer shipment declines in the second half of 2018 and the first half of 2019 and thus far, even with the slowdown in the overall semiconductor industry, TSMC is still kicking out millions of 12-inch wafer equivalents – 3.97 million, up 9 percent, in Q3, to be precise. That is a bit slower growth than in the immediate past three quarters, but it is still growth because, frankly, TSMC is the best foundry in the world and chip designers have very little choice but to go to TSMC if they want to push the limits on their designs with process.

Wei said that the 3 nanometer N3 process, which was giving TSMC some headaches a year ago, is on track for volume production later this year and that a “smooth ramp” was expected in 2023, driven by strong HPC and Smartphone segment adoption. Wei added that 3N demand exceeds supply because of foundry tooling constraints – which means pricing can be very profitable for the foundry – and that N3 process would be “fully utilized” next year and would in fact be higher than the 5 nanometer N5 process was in its ramp in 2020. The more advanced N3E process will represent a “mid-single digit percentage” of wafer revenues next year, and that some HPC and smartphone chip designs would be employing this kicker process. The number of tapeouts for the N3 and N3E processes is more than twice that of the N5 process at the same point in its history, and demand is expected to be strong in 2023 and 2024.

The N2 2 nanometer node is in the works after that, and all of these together are expected to drive the 15 percent to 20 percent annual revenue growth TSMC is planning for over the next several years.

But in the meantime, TSMC is focusing on what could be a prolonged downturn in semiconductors and how to avoid that.

“We expect probably in 2023, the semiconductor industry will be likely to decline,” Wei explained. “And while TSMC also is not immune, we believe our technology position, strong portfolio in HPC and longer-term strategic relationship with customers will enable our business to be more resilient than the overall semiconductor industry. And that’s why we say 2023 is still a growth year for TSMC and the overall industry probably will decline.”

That’s about as good as it gets, under the circumstances.

Intel Decides To Engineer Its Fab-Filled Future After All

Newly anointed Intel chief executive officer Pat Gelsinger held the coming out party for his strategy to get the world’s largest chip manufacturer and designer back on track, called “Intel Unleashed: Engineering The Future,” on Tuesday after the market closed. It was a strange echo of an essay we wrote …

Another Crazy Idea: Intel Might Buy Globalfoundries

Back in March, when we wrote up Intel’s Integrated Device Manufacturing 2.0 strategy put forth in the vaguest of terms by then-new chief executive officer Pat Gelsinger, we quipped that Intel might be wishing as it launches Intel Foundry Services that it had some of its older fabs around with …

Intel’s Chips No Longer Pay More Than Their Fair Share Of Foundry Costs

The biggest benefit that is coming from the separation of the Intel chip design and marketing business from its foundry operations is that Intel’s chip product groups no longer have to shoulder the totality of the immense costs of its manufacturing operations. The biggest downside is that they these chip …

Be the first to comment