Back in March, when we wrote up Intel’s Integrated Device Manufacturing 2.0 strategy put forth in the vaguest of terms by then-new chief executive officer Pat Gelsinger, we quipped that Intel might be wishing as it launches Intel Foundry Services that it had some of its older fabs around with which to build a client base.

Not every chip – indeed, by volumes, not most chips – needs to be etched using the most advanced nodes. And the remaining foundries in the world do a pretty good job squeezing every last dollar out of those old fabs, which helps to pay for the new ones and gives a pipeline of customers for those new fabs in the future.

On July 26, Gelsinger and Ann Kelleher, general manager of technology development, are going to be hosting an event called Intel Accelerated that will talk about process and packaging roadmaps for “upcoming leadership products.” And if the rumors are correct that Intel is working behind the scenes to buy Globalfoundries from its owner, Mubadala Investment Company, which is the investment arm of the oil producing nation of Abu Dhabi, Gelsinger will probably want to make the announcement of the acquisition of Globalfoundries the same day.

The Wall Street Journal has caught wind of a potential deal for Intel to buy Globalfoundries for $30 billion, and one that Globalfoundries itself might not even be aware of. (Globalfoundries denies it is in talks with Intel on such a deal, but that does not mean Mubadala Investment Company is not talking to Intel.) That $30 billion price tag is significant because back in early April the rumors were going around that Mubadala Investment Company was going to take Globalfoundries public – during the height of the chip shortage crisis that would no doubt inflate its value even though its most advanced processes are stuck at 14 nanometers – and raise somewhere between $20 billion and $30 billion.

If anybody has a bunch of older fabs that are still cranking out the chips and brining in the dough, it is Globalfoundries, and frankly, the company’s business will snap right into that of Intel with the only overlap being at the 14 nanometer processes that both companies are still using in relatively high volume. It is probably a safe bet that Intel’s 14 nanometer process is better than that of Globalfoundries, the latter of which was used to make AMD’s first generation “Naples” Epyc 7001 processors and the memory and I/O hub chiplet in the second generation “Rome” Epyc 7002 and third generation “Milan” Epyc 7003 processors as well as IBM’s Power9 and System z15 processors.

Intel has had plenty of trouble getting to 10 nanometer and now 7 nanometer processes, and Globalfoundries had its own issues with 10 nanometer manufacturing and tried to jump directly to 7 nanometers with a two-pronged immersion lithography and extreme ultraviolet lithography approach, and then pulled the plug on the whole thing back in August 2018. Much to the surprise of IBM, which in June of this year, as the Globalfoundries IPO rumors were gaining steam and as IBM had enough supplies of its Power9 and System z15 processors to meet any future demand, launched a lawsuit against its former chip partner over chip roadmap failures. That lawsuit is a big enough deal that Intel will have to find some way to settle it, but it if can acquire Globalfoundries and possibly gain IBM as a secondary foundry partner, that would be an interesting turn of events. IBM and Intel are already working together on research and development for 7 nanometer and smaller transistor geometries and have both done fundamental research to bring nanosheet transistors to market, which will be an important factor in the coming years.

After Globalfoundries tore up IBM’s chip roadmap because it did not have the money or time to make 10 nanometer or 7 nanometer manufacturing work, IBM shifted to Samsung as its 7 nanometer foundry partner for its Power10 and System z16 processors. While we presume that the high end Power10 chips are set to come out sometime this fall, we have no idea how tough it might be and if Samsung is any good at making complex server chips, which are different from making memory, flash, and low-end client chips. What we can tell you is that the Power10 and System z processors are running later than expected, and this may have been a contributing factor in IBM not being able to win the two big exascale supercomputer deals at Oak Ridge National Laboratory and Lawrence Livermore National Laboratory, which together account for $1.2 billion in spending.

The IBM-Globalfoundries lawsuit is probably going to get ugly, and particularly so since Globalfoundries was paid $1.5 billion by Big Blue to take over its Microelectronics chip foundry business and to provide a ten-year roadmap for Power and System z processors. The deal also included technology and people, much of whom have been sold off. GlobalFoundries sold IBM’s former East Fishkill fab to ON Semiconductor for $430 million in April 2019 and sold its custom ASIC business to Marvell in May 2019 for $650 million with an additional $90 million potentially coming in, and then sold off some other assets that IBM says tally up to $1 billion. Accountants and lawyers will argue over this, and a jury will decide. Unless Intel buys Globalfoundries and settles the case IBM has brought.

It may or may not be a coincidence that AMD and Globalfoundries just renegotiated their wafer supply agreement through 2024, and AMD now is released from its exclusivity clauses in its contracts with Globalfoundries. Now, anyone can make the I/O die at the heart of the Epyc architecture, which by the way is not helped by being shrunk. Signaling and other I/O circuits perform worse when you shrink them, not better, which is one of the reasons why it has been a challenge creating monolithic dies with ever-shrinking transistor geometries.

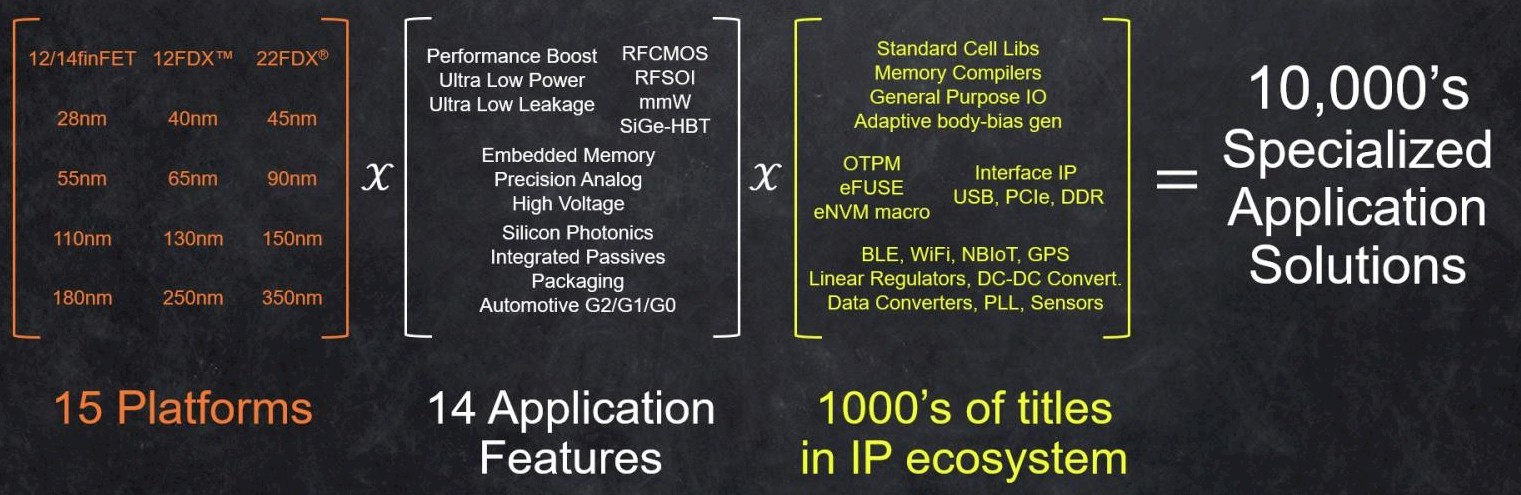

What does Intel get if it buys Globalfoundries, and it is worth all of this hassle and money? For one thing, it gets some fabs and a slew of process nodes and technologies that are useful and driving revenue from lots of existing customers. These are all things that Intel needs. The “innovation equation,” as Globalfoundries calls it, looks like this:

In the five years between 2014, when it bought IBM Microelectronics, and the end of 2019, when it focused down to its current configuration, more than 1,500 chip designs had gone through GlobalFoundries, enabled in part by more than 100 ecosystem partners – tool suppliers, logic block design firms, and so on. Last year was a challenging year for many semiconductor makers because of ingredient shortages, labor shortages, and other supply chain issues, and revenues were only $5.7 billion, down from the $6.2 billion it reported in 2017. (Globalfoundries is not a public company, so we do not have complete financials to analyze.) The company is expecting a 10 percent or so increase this year, which should put it over and above those 2017 figures.

Globalfoundries has two chip factories in Singapore (one on older 200 millimeter wafers and one on current 300 millimeter wafers), two 300 millimeter fabs in Germany, and one 200 millimeter fab and two 300 millimeter fabs in the United States. In March of this year, Globalfoundries said it would pour $1.4 billion into expanding its fabs that would drive 13 percent output increase in 2021 and 22 percent in 2022, and in June as the semiconductor shortage was getting really crazy, the company said it would pony up another $4 billion to push a further ramp in 2023 for its operations in Singapore (where Chartered Semiconductor, another acquisition that Globalfoundries did back in 2010 two years after being spun out of AMD, was centered).

Sometimes you build a business from scratch and sometimes you buy one to build a foundation upon. With Intel wanting to be regarded as the second foundry option after Taiwan Semiconductor Manufacturing Corp, an acquisition of Globalfoundries – even for $30 billion, a 5X multiple over earnings – gives Intel a chance to really build this Intel Foundry Services business. According to data from IC Knowledge, which is cited by our friend Aaron Rakers at Wells Fargo in a recent report, TSMC has around 36 percent of wafer starts per month (WSPM) capacity across the foundries of the world, but Intel has around 18 percent and Globalfoundries has around 11 percent. The combined companies are within spitting distance with TSMC, especially if Intel starts counting its own chip manufacturing costs as revenue for Intel Foundry Services, which we think it will do. While people make a lot of noise about the advanced nodes because they are necessary for datacenter devices like CPUs, GPUs, DPUs, and other kinds of compute engines and network devices, a little less than half of the company’s revenues come from chips with 16 nanometer and larger transistor geometries. (To be specific, 5 nanometer is 18 percent of revenues and 7 nanometer is 31 percent.) That old stuff persists for a long, long time and helps pay the bills on the new processes. This is what Intel has been missing, and we said as much when the whole Intel Foundry Services idea was floated in earnest.

If Intel buys Globalfoundries, the payback is probably less than four years, given the political climate in the United States – where the federal government would no doubt like the deal and maybe even help Intel do the deal – and the ability of Globalfoundries to capitalize on the semi shortages plaguing the world.

We won’t be surprised if the deal goes down, and we still also won’t be surprised if Intel buys VMware to shore up its legacy X86 server business. The company is rich enough to do both deals as long as money is essentially free – which it is for now, at least. Both companies could be bought for stock. The question is this: Do Michael Dell and now Mubadala Investment Company want to be the largest shareholders in Intel? That is what these deals mean because it is highly unlikely that Intel can borrow the money to do the deals. Even if borrowing money is essentially free, stock market capitalization is also essentially free. Which is why Nvidia can buy Arm Holdings for $40 billion and AMD can buy Xilinx for $35 billion without borrowing to much actual money and taking on debt.

Different GPU Horses For Different Datacenter Courses

If the semiconductor business teaches us anything, it is that volumes matter more than architecture. A great design doesn’t mean all that much if the intellectual property in that design can’t be spread across a wide number of customers addressing an even wider array of workloads. How many interesting and …

HBM Gives Xeon SPs A Big Boost On Bandwidth Bound Work

If there is one bright spot in the Xeon SP server chip line from Intel, it is the version of the “Sapphire Rapids” Xeon SP processor that has HBM memory welded to it. These chips make a strong case for adding at least some HBM memory – or something that …

IBM Lays Its GenAI Foundation With Software And Services

When you are International Business Machines and you do corporate IT deals in 185 countries around the world, political and economic uncertainty is always a problem. And when you compound that with high interest rates, it can be tough to make some money. Luckily for Big Blue, there are product …

Really The Antitrust Regulators are about as effective in the US currently as a damp squib! So Much ineffective that Presented with the Standard Oil Of Ohio Trust the current US regulators would have done nothing there with that Trust’s many market abuses. Does the World need fewer Pure Play Foundry operators and more consolidation in the Technology Markets.

What about Fostering more competition by making sure there are at least 6 or 7 leading edge Foundry companies and many more trailing edge foundry companies and not fewer. I’m against any further consolidation in the market for fab services and GF needs an IPO and folks can invest that way. And Ditto for ARM Holdings getting an IPO instead of Nvidia turning that market into an x86 market Version 2.0!

Any info on where Intel currently fabs its silicon photonics chips?