The third quarter earnings season starts this week for the hyperscaler and cloud giants, and it is fortuitous that the economists and IT analysts at Gartner have updated their forecast for IT spending for 2024 and added an jaw-dropping forecast for 2025 and hinted at a brave new world of massive datacenter spending out to 2028.

AMD’s ebullient forecast for AI accelerator spending – and therefore overall systems spending – cooled a bit recently, as we reported last week, and Gartner’s is heating up and perhaps that will converge, along with forecasts by Nvidia, IDC, and Forrester to something that will approximate reality five business years hence.

As we are fond of saying, the best way to predict the future is to live it. In fact, it is the only way – and we are not even certain of that some days.

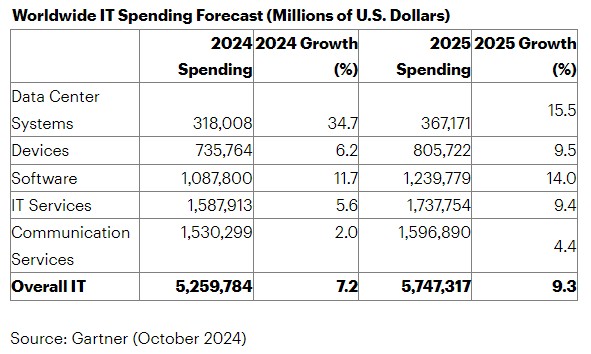

In its October forecast, Gartner expects for the world to consume $5.26 trillion in IT hardware, software, and services and various communication and networking services, an increase of 7.2 percent. And, as you no doubt expect, it is the spending on datacenter systems – servers, storage, and switching – that is driving the average way up and also creating drag-along spending increases for software and services for building generative and other kinds of AI systems.

With the data only in for two quarters of the year and the third quarter results coming out from the hyperscalers, cloud builders, and IT vendors over the next few weeks, Gartner put some big stakes in the ground, saying that datacenter systems spending would boom by 34.7 percent to just a tad more than $318 billion this year. The last time we saw growth like this, we had just seen system spending collapse in 2008 and 2009 and we pulled back out of that hole that we called the Great Recession. This is not a big recovery; this is real growth caused by a new market.

But don’t get carried away. As we enter the “trough of disillusionment” for GenAI in 2025, the spending increase will cool a bit but still around $50 billion in incremental spending on datacenter systems is forecast in 2025.

To be specific, Gartner is projecting that datacenter systems spending will grow by 15.5 percent to $367.2 billion. Spending on devices – PCs, smartphones, and tablets – is going to accelerate after being in the doldrums for years, and spending on enterprise software and IT services is also going to accelerate as well over the jumps seen in 2024, so Gartner is projecting that overall IT spending is going to rise by 9.3 percent to $5.75 trillion.

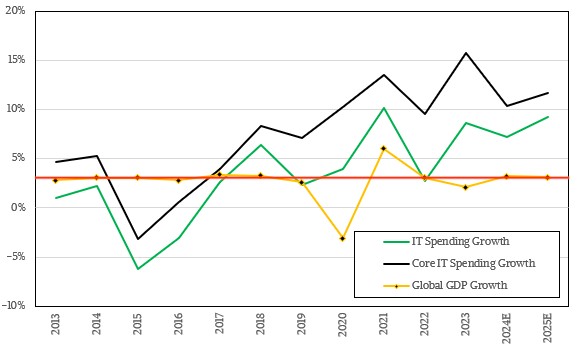

We like looking at longer trends, and so we have compiled the publicly available IT spending dataset from Gartner into a monster table and also updated the figures for 2023 and 2024 and added the forecast for 2025. And thus, you can see a trendline from 2012 through 2023 and the forecasts for 2024 and 2025 in one fell swoop. Take a look here:

We like to look at core IT spending trends as well, and have carved this out by adding revenues from datacenter systems, enterprise software, and IT services together to create a “Core IT” category that we think is a more accurate reflection of “real” IT spending. That is shown in bold blue in the chart above.

And to get some sort of grounding, we also like to plot the growth in overall IT spending and core IT spending against global GDP growth. We realize that this is not a perfect gauge of relative growth, given that the IT dataset is worldwide revenues converted into US dollars in a world where more than 180 countries have different currency exchanges, inflation rates, and GDP growth rates.

A couple of things to note here.

First, in this dataset at least, core IT spending always grows faster than overall IT spending grows, varying from a low of 1.3 percent in 2017 to a high of 7.1 percent in 2023. In 2024 and 2025, this delta in growth will actually be a little lower than average, which is just shy of 4 percent across the fourteen years shown.

Second, if you plot global GDP growth from the World Bank, including projections for 2024 and 2025, against overall IT spending and core IT spending growth, they are not always in lockstep. In 2015 and 2016, global GDP grew by 3.1 percent and 2.8 percent, respectively, but overall IT spending fell by 6.3 percent and 3 percent and core IT spending was down 3.2 percent in 2015 and up only 0.6 percent in 2016.

On average across the years shown, core IT spending growth tends to be 4.8 percent higher than global GDP growth rates.

While hardware gets all of the headlines, Speaking more generally, datacenter systems spending has been relatively flat over the past decade and a half. But the GenAI boom is changing that, as you can see:

Gartner has a fairly aggressive forecast going out to 2028, and it provided a little detail that helped us build a very crude model of AI and general purpose server sales.

First, Gartner said that it believes that between 2024 and 2028, the IT market will increase spending each year by around $500 billion, and will shoot through $7 trillion in spending by 2028. This is a lot of money. The company also said that demand for GenAI machinery will help server sales triple from 2023 through 2028, inclusive. If you assume a reasonable ratio of datacenter systems spending against that more than $7 trillion in overall IT spending – meaning that more of the GenAI boom starts being software and services and that hardware spending normalizes as performance and competition increases – then you might guess, as we did and for the sake of argument, that datacenter systems spending in 2028 would be somewhere around $449 billion.

This is an unprecedented amount of server spending, but still considerably less than you might infer as AMD has said it now expects $500 billion in datacenter AI accelerator spending in 2028. Assuming that GPUs and other accelerators (and not CPUs with matrix engines) represent the bulk of that accelerator spending, then that implies about $1 trillion in AI server spending. Add another $200 billion or so in general purpose server spending and that gets you to $1.2 trillion in all server spending, and add networking and storage and maybe you are at $1.6 trillion. (We still have trouble swallowing such large numbers as AMD is throwing around.)

In any event, here is the model we built for server spending, including a forecast out to 2028 with a companion compound annual growth rate between 2022 and 2028 inclusive:

Our assumption in this model is that exploding core counts in general purpose servers keep a lid on revenue growth, and thus the CAGR is essentially flat here. And so the remaining money is all AI servers. And we get a CAGR of 67 percent between 2022 and 2028 inclusive and AI servers representing 71 percent of total server spending in 2028 with those assumptions.

If AI systems somehow get magically cheaper – and we don’t think they will – then all that will happen is that the revenue stream will be smaller for all servers. We think profit levels from peddling servers will drop no matter what, but the Gartners of the world never talk about if anyone is making money selling iron. What we can tell you is that Intel, IBM, Nvidia, Microsoft, Red Hat, and AMD get most of the profits from selling systems over the past decade.

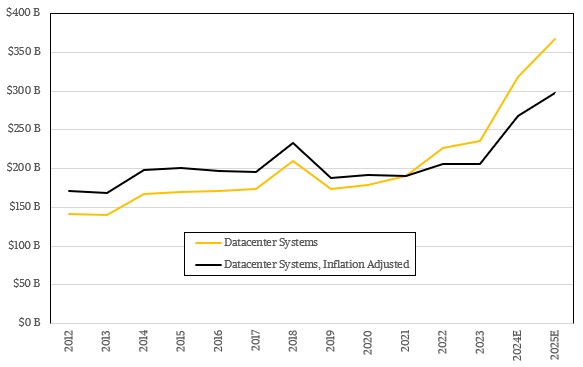

One last thing. Whenever you have a dataset that spans many years, you have to be cognizant of the inflationary effects of the US dollar and the price increases in products that drive that inflation. We can’t easily know precisely what inflationary effects happen with the commodity parts used in systems and the striking prices that embody these and other costs as OEMs and ODMs sell stuff, but we can infer it a little by inflation adjusting revenue streams like the ones that Gartner has assembled in its IT spending forecasts over these many years.

And so, we have been reckoning all of this spending against 2021 US dollars, using the Consumer Price Index (CPI) as our adjuster. And if you do that, you see the datacenter systems spending spin around the 2021 pivot point like this:

Inflation adjusters raise past revenues and lower future revenues due to inflationary effects. And what you see in the chart above is that datacenter systems spending, in terms of “real” spending power, was essentially flat between 2013 and 2024 with a big bump thanks to the hyperscalers and cloud builders in 2018.

And then, in 2024 and 2025, the forecast is for real spending to really jump a lot, thanks mostly to GenAI and to general purpose upgrade cycles gaining a little bit of steam. Mostly so companies can condense their server fleets to save power and space so they can add AI machinery, we think.

Pawsey Finds I/O Sweet Spots for Data-Intensive Supercomputing

When it comes to data-intensive supercomputing, few centers have the challenges Pawsey Supercomputing Centre faces. While the center handles its fair share of scientific workloads for Australian research, the radio astronomy user base, which is about a quarter of its compute cycles and nearly all of its archival storage, is …

Will Open Compute Backing Drive SIOV Adoption?

Virtualization has been an engine of efficiency in the IT industry over the past two decades, decoupling workloads from the underlying hardware and thus allowing multiple workloads to be consolidated into a single physical system as well as moved around relatively easily with live migration of virtual machines. It is …

Intel Gets Its Chiplets In Order With 6th Gen Xeon SPs

Based on what Intel has been saying for the past several weeks in various events, but especially the Hot Chips 2023 a few weeks ago and the more recent Intel Innovation 2023 extravaganza, the company’s foundry process roadmap and its server processor roadmaps are going to align harmoniously to make …

Be the first to comment