Low margins, an unpredictable cycle, expensive and ongoing research development efforts, a slavish commitment to processor upgrade timelines, and a market that will only ever grow so much—who wouldn’t want to be in the supercomputing systems business?

All kidding aside, the company known for its role as a foundation of the high performance computing market as we know it, Cray, has stood witness to these barriers year in and out, unyielding against the slings and arrows of outrageous fortune, but only ever just profitable enough. And while the financials might look chaotic from the outside, Cray’s business appears well under control and poised for growth.

During the company’s call to go over first quarter results for 2015, Cray CEO Peter Ungaro cast a bright outlook for the year, projecting $715 million in revenue by the end of the year as a few major systems in particular come to acceptance fruition in research, oil and gas, and weather modeling. Between 2016 and 2018, a new influx of cash will hit the company’s books from the CORAL procurements and the much-anticipated 2018 delivery of the next-generation Cray “Shasta” system rolls into Argonne National Lab’s upcoming Aurora supercomputer.

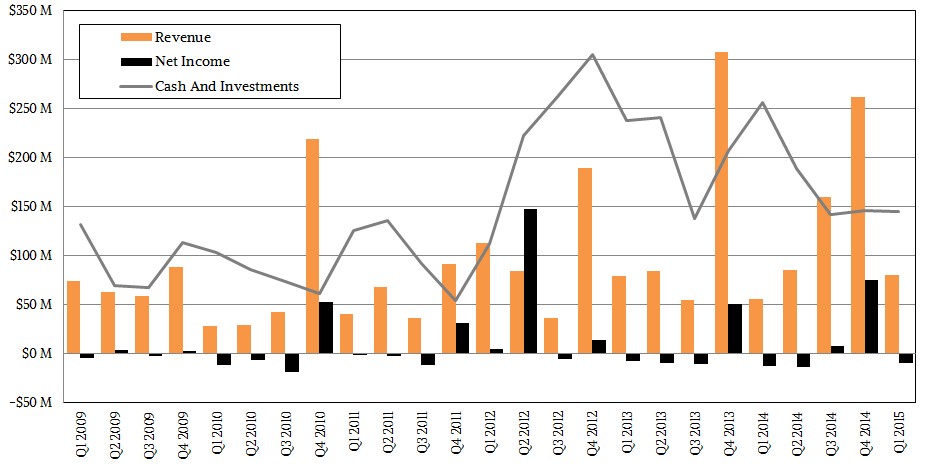

For those who follow the HPC business, it is well known that Cray quarterly financials tend to be lumpy as they are fed and diminished by large contracts that send their quarter-to-quarter numbers on a roller coaster ride. To understand how Cray is performing, one has to take a yearly look to gauge over the long haul while holding some healthy skepticism about when massive systems might be accepted and thus put onto the books.

In many respects, the best way to paint a more accurate picture of Cray’s historical growth is to factor out the sale of its interconnect business to Intel in 2012, which injected $139 million into their books, causing a rather wild peak which can be seen in the chart below—one that outpaced its overall revenue in the quarter. With that removed, over the last six years, Cray has raked in over $2.3 billion in revenue, which sounds fantastic, but note that only $129 million of that was profit. In other words, just a tick over 5 percent of revenue over those years went to the bottom line as net income.

As is the case for every first quarter in Cray’s recent history, there is what looks like a big slump to the outside stock world, which is upended throughout the rest of the year before a big finish in Q4. Last year’s Q1 revenue was $55.1 million, which has jumped to $79.6 million for the first quarter of this year with overall gross profit margins for this past quarter at 30 percent compared to 33 percent for Q1 of 2014.

Think about those margins above for a moment. It might be better than what the hyperscale system makers are seeing (Quanta, as an example) but it is certainly nowhere near what IBM sees margin-wise for its mainrframes. In other words, it’s one hell of a tough business, but speaking of IBM, the fact that Big Blue killed off BlueGene (not to mention the Blue Waters fiasco) opened the door for Cray to walk in and see some real growth in recent quarters.

To be fair, a great deal of Cray’s growth over the years since Titan was accepted at Oak Ridge National Laboratory was the result of direct investments that never made it onto these charts, since they were DARPA funds pushed into the R&D arm of Cray to help the company put together systems like Titan. Without those funds feeding them for five years, especially since IBM systems were filling out the Top 500, Cray might not have such a strong stability story. But the good news is, however Cray funded itself before Titan was accepted, it worked and its roadmap ahead looks strong, especially with the recent big national lab contracts its has secured, including its role as the integrator for the 2018 Aurora system.

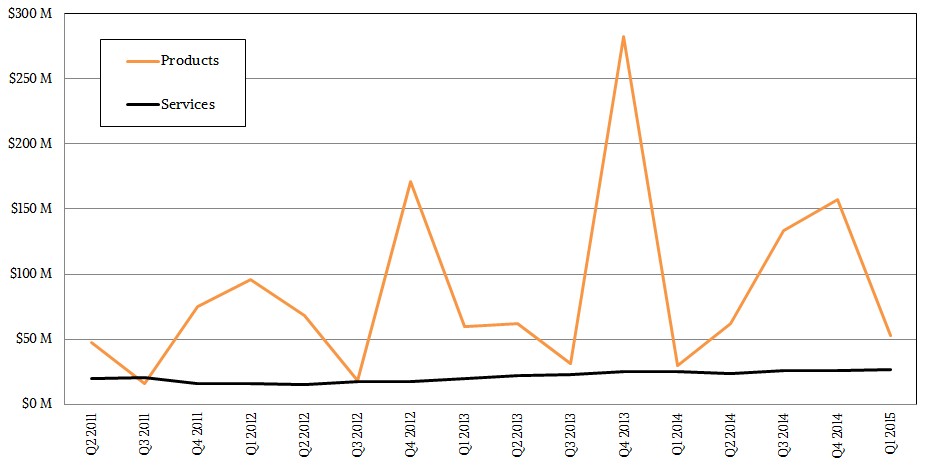

As one can see below, Cray has remained a product-driven company with a flat (and nicely predictable) services business. As noted previously, the spikes in products come with the big system deals (see that Titan peak?) but what’s noteworthy is that, no matter how far back one goes, this trend is the same–big peaks and big valleys with little in between for too long. A separate article about this will appear at some point where this is tracked in lockstep with Intel processor upgrades and announcements because these are no coincidences.

As one might recall, part of what is interesting about the Aurora deal is that Intel is the prime for that contract, with Cray backing it on the integration and software stack. Just as the weakening of IBM in HPC opened new doors for Cray, the company’s strong relationship with Intel is going to define its future in the near term. This is probably a lot less scary for Cray than when it was tied tightly to AMD’s Opterons for its high-end systems, but the delays on “Sandy Bridge” Xeons from Intel pushed out an entire quarter–even if it those Xeon engines were the key to some of the biggest, baddest systems Cray has built to date.

And all of this begs an important question. Cray knows full well what it means to be at the mercy of a chipmaker’s delays or problems. But if Intel is going to drive its business, how does Cray differentiate enough to stay viable and not just become what amounts to a servicing arm of Intel? Well, remember that huge number we shaved out of the revenue earlier? That interconnect business, which Cray sold to Intel in 2012 might have been the jailhouse key. And here’s where things get meaty. If Cray could get back to what it is truly geniuses at doing, which is innovative engineering, and could plug away at a new interconnect, the balance of power could change. At least to some degree since Cray would have another truly unique custom piece of the stack, which is absolute leverage in the high performance computing market.

It is not out of the realm of possibility to suggest that Cray is already hard at work on just that. But of course, take a look at the chart above and try to math out just how much of its revenue can be sunk back into the kind of labor-intensive, long-haul research and development that portends. Cray has interconnect wizard Steve Scott back in Cray fold and all the motivation in the world to continue differentiating on engineering (which begs the other question, how will the SGI, Dell, and HP server makers for supercomputing stack up if Intel no longer technically “needs” them)?

The other differentiating factor for Cray would be to push development for ARM processors, which is already happening via a research and development contract from the US Department of Energy under the FastForward 2 program. The purpose of Cray’s funding here is to explore how 64-bit ARM might find a fit in the supercomputers of the future with Cavium’s 48-core ThunderX ARM-based processors as a starting point.

In all of these cases, the clock is ticking. None of these are simple propositions—building a new interconnect, developing on an architecture that still lacks an ecosystem, especially for the demanding HPC environments of the future, and of course, it also takes time for the funds to free up following the acceptance of a number of pending systems at national labs between now and 2018.

This goes back to the point, which can be seen quite clearly in the charts, that gauging Cray on its quarterly financial history is little indication of its health. Rather, as many already know, it’s a historically lumpy financial road, with big spikes now and again followed by the expected declines.It is always interesting to watch the market respond to first quarter reports from Cray, which tend to send the stock price down as those who aren’t aware of the natural ebb and flow die off in droves at the sight of what looks like dire news. But Cray, as always, plugs away and delivers steady growth–at least as much as one could expect from a supercomputing company.

“We had a solid first quarter as we continued our strong run of new wins, including at Petroleum Geo-Services, which selected an XC40 and Cray storage to power its most advanced seismic imaging efforts,” Ungaro told Wall Street during the call to go over its first quarter results. “We also installed our first XC supercomputer in Poland at Stalprodukt, a leading advanced steel manufacturer. Looking toward the future, we recently outlined our plans for our next-generation supercomputer, code-named ‘Shasta,’ targeted for 2018. A Shasta-based system was selected by Argonne National Laboratory along with Cray storage and an XC system for the Department of Energy’s CORAL project, and we’re excited to be partnering with Intel to deliver these powerful new systems. This is a significant validation of our product roadmap as Shasta will deliver on our Adaptive Supercomputing vision to bridge the world of supercomputing with data analytics.”

In an ideal world there would be a way to break out the data analytics products and services line Cray is working to expand with its Urika massively threaded system, which has found a cozy home in some notable enterprise environments, including a mystery major league baseball team. So too would it be useful to see how the storage business contributes to the bottom line and how that has changed over time. While Cray gives bulk numbers for every lumpy financial year, the real takeaway here is that over time, there is a steady bit of growth–and based on what we are seeing now, the company is on track to really bump up revenues and net profit this year. What happens after the money hits from the Aurora and other systems after 2018 remains to be seen, but one could hope that Cray keeps pushing to get out from dependence on Intel to innovate on the interconnect, alternate processor, and software stack fronts.

The “hidden” point of that is simply that Intel just showed, with its prime contractor award on the largest U.S. supercomputer announced for the next few years, that the chipmaker doesn’t necessarily “need” its partners in quite the same way it used to. We have an in-depth on that coming Monday. Get your opinions ready.

Why Would HPE Buy Juniper Networks?

It looks like Hewlett Packard Enterprise might be having a datacenter networking revival. The word on the street, as reported by the Wall Street Journal, is that HPE is getting ready to shell out $14 billion to acquire Juniper Networks, the company that played the gadfly for Internet routing and …

At Long Last, HPC Officially Breaks The Exascale Barrier

Significant business and architectural changes can happen with 10X improvements, but the real milestones upon which we measure progress in computer science, whether it is for compute, storage, or networking, come at the 1,000X transitions. It has been nearly two decades since the “Roadrunner” hybrid Opteron-Cell was fired up at …

With HPC Humming Along, HPE Awaits Its AI Boom

The ProLiant server business is down in the dumps, and the storage business is in a slump. But petascale and exascale supercomputer deals based the combination of AMD CPUs and GPUs have filled in a lot of the gap. And Hewlett Packard Enterprise is now waiting, like all OEMs and …

Be the first to comment