Economic and technical forces have a kind of momentum that keeps them growing even as any new technology goes through its inevitable hype cycle from innovation to inflated expectations to disillusionment to deployment into productivity.

As far as Gartner chief forecaster, John Lovelock, is concerned, we hit the peak GenAI frenzy in the middle of 2023, and despite the increasingly massive investments in AI datacenters and the number of financial powerhouses and governments looking to get in on the deals, we have been sliding down into the trough of disillusionment when it comes to GenAI ever since. Lovelock hosted a webinar on GenAI spending and expectations for market adoption in conjunction with Gartner’s January 2025 update on global IT spending for 2024 and 2025, and gave some hints about AI spending and general purpose server spending for 2028 as well.

As usual, we are updating and plotting out the revisions for IT spending and also using the bullet points Gartner provided in its forecasts to come up with some datacenter spending estimates of our own. Use them at your own risk, but it will give you what we think might be the shape of things to come and all it cost you was the time to read it.

In the past, when looking at IT spending forecasts, we used to think of that as a way to gauge the increasing value of infrastructure and the people who run it and program it. But with GenAI, the investments are being made to augment the capabilities of people, and in some cases replace them. Which means that the fact that IT spending is on the rise does not mean that your paycheck will be getting bigger – even if you become a master of AI wizardry within your IT organization.

We last looked at Gartner’s IT spending forecast when it came out in October 2024, and the datacenter systems spending numbers for last year and this year are continuing to swell. Three months ago, Lovelock and the Gartner prognosticating team expected For datacenter systems spending – meaning servers, storage, and networking – to rise by 34.7 percent to $318 billion in 2024 and then grow another 15.5 percent to hit $367 billion in 2025. Growth was an anemic 4 percent in 2023, hitting $236 billion despite the first giant wave of GenAI server spending, which we reckon was about 3X higher than in 2022. About half of the budget for that GenAI spending came out of upgrade deferrals for general purpose servers, we think. (We will get into this in a moment.)

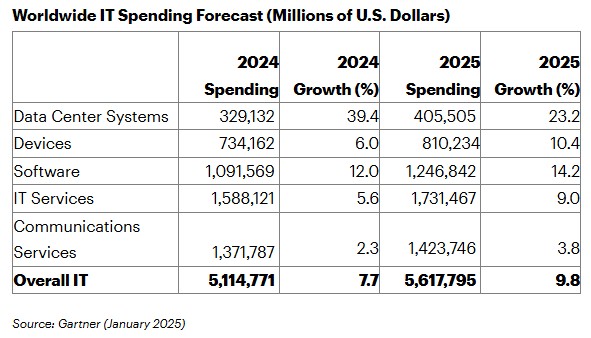

With the forecast announced this week, Gartner now thinks datacenter systems spending rose by 39.4 percent in 2024, accounting for $329 billion in server, storage, and networking spending for gear made by ODMs and OEMs. Looking ahead, Gartner is expecting for the datacenter to drive $406 billion in revenues in 2025, up 23.2 percent from last year.

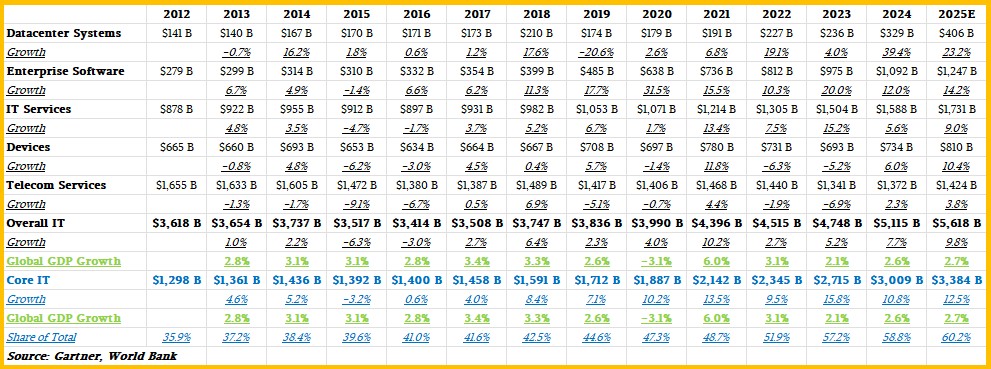

Here is the compilation of IT spending data from Gartner since we started tracking it in 2012:

If you need to read that in large font, click on the graphic and it will enlarge.

In the new forecast, spending on enterprise software wiggled up a few tenths of a point compared to the October 2024 forecast, but not enough to worry much about it. In the current forecast, Gartner thinks enterprise software spending increased by 12 percent in 2024 to $1.09 trillion and will rise by another 14.2 percent in 2025 to reach $1.25 trillion.

The forecast for IT services is about the same, too, with revenues up 5.6 percent to $1.59 trillion last year and an expectation they will be up 9 percent to $1.73 trillion this year.

Add these three up, and you get what we call the Core IT market. In 2023, Core IT rose by 5.2 percent to $4.75 trillion, and in 2024 it grew another 7.7 percent to reach $5.12 trillion. For 2025, Gartner expects the combination of these three – datacenter systems, enterprise software, and IT services – to hit $5.62 trillion, up 9.8 percent.

It is always interesting to contrast the growth in global IT spending with growth in gross domestic product for the world’s economies. Here is a pretty chart that does just that:

In general, and excepting the crash as the coronavirus pandemic kicked in and the bounce as we all changed our lives, GDP growth (the orange line) tends to be around 2.5 percent annually from 2013 through 2024 and including the forecast by the World Bank for 2025. There are times, of course, when IT spending declines, as happened in 2015, or doesn’t grow much at all, as happened in 2016. And 2019 and 2022 weren’t exactly barn burners for overall IT spending growth, either as you can see in the chart above. Overall IT spending growth is dampened by tepid sales of PCs, tablets, and smartphones.

However, Core IT spending growth (the black line) has been steadily higher than GDP, and rising in large part thanks to infrastructure investments during the pandemic and then GenAI boom.

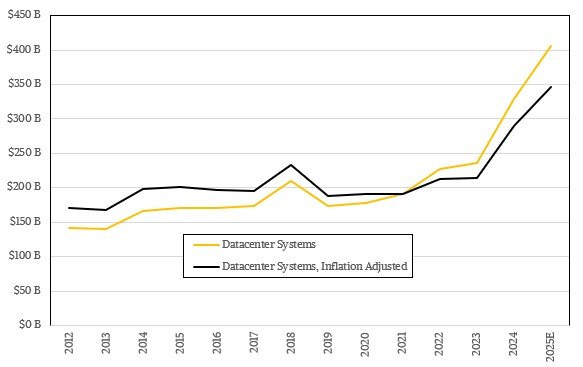

Now, you always have to be aware of real growth – meaning people are buying more stuff – versus inflation that looks like growth – meaning stuff is getting more expensive. Here is what happens if you inflation adjust datacenter systems spending over time with inflation as gauged by the Consumer Price Index, which both are based on US dollars. This is not a perfect way to see how much is growth and how much of it is currency exchange and inflation, but you get the idea:

As you can see, there was a big bump in real spending on servers, storage, and networking as a group in 2018 but otherwise, it has hummed along at around $200 billions a year of real effective spending (in this case as expressed in 2021 dollars, when we first did the inflation adjustment on the Gartner data). But clearly, in 2023, something happened, and that something was GenAI spending among the hyperscalers and cloud builders, and then in 2024, expanding out to increased spending by service providers, large enterprises, and HPC centers.

By the way, on the webinar walking through the numbers, Gartner did a straw poll of IT shops and found that the median price increase that they were facing to cover price increases for recurring expenses (hardware, software, services, licenses, and other contractual spending) was 8.5 percent for 2025’s budgets. So the price hikes in IT seem to be significantly worse than for the economy at large.

It Is Our Pleasure To Server

So what is all of this spending in the datacenter? We have been trying to reckon that for a while, and a few data points and a chart showed during the webinar helped us build a model off the Gartner data that gives a feel for what AI server, non-AI server, and storage and networking spending has been over time and out into the future. This latter bit – the future – is the thing everyone wants to know.

In the press release announcing the IT spending forecast, Gartner said this: “Spending on AI-optimized servers easily doubles spending on traditional servers in 2025, reaching $202 billion dollars.”

We would be the last one to throw stones about grammar, but we think this means AI server spending will be $202 billion in 2025 and non-AI server spending will be around half that. If you look at the chart shown during the webinar, it looks like total server spending was around $290 billion, which puts non-AI server spending at $88 billion. We know Gartner said that there was $329 billion in overall datacenter systems spending, which means if you subtract it out, you get $99 billion for storage and networking spending in 2025.

That’s one year.

Then Lovelock said on the webinar that AI servers would reach $312 billion in 2028, with traditional servers (what we are calling non-AI servers) reaching $126 billion. Gartner has said previously that the IT market will add $500 billion a year in overall spending, to break above $7 trillion in 2028. We added some witchcraft to the data in the table above, calculating the share of datacenter systems spending of the total IT spending over time, which was very close to 5 percent in 2022 and 2023 and grew to 6.43 percent in 2024 and is expected to hit 7.2 percent in 2025. We guessed the share it would be in 2026, 2027, and 2028 – it was an intelligent guess, we think, cresting at around 8.3 percent, plus or minus a wiggle, in 2027 and 2028. With that, we have a reasonable guess for datacenter systems spending.

After some other intelligent guesses about how storage and networking spending is changing over time and how non-AI servers are growing, we came up with this dataset, with our estimates and reckoned against that Gartner chart that, frankly, had some formatting issues that did not make it a perfect way to reverse engineer data points. Anyway, take a look:

A few interesting things. First, in 2025, Gartner expects that “service companies and hyperscalers” will account for 70 percent of server spending. Moreover, Lovelock says that the hyperscalers will operate $1 trillion worth of AI servers, but not as cloud capacity. Rather, they are going to be participants in the sale of vast AI models and the machinery will be used to make the models that we all will buy. “Hyperscalers are pivoting to be part of the oligopoly AI model market.”

And some model makers, we would add, are pivoting to be hyperscalers – xAI and OpenAI are cases in point.

What the table above shows is that about halfway through this year, two-third of the server revenue in the world will come from AI servers, up from a third of total revenue share for all of 2023. This is a huge change. And if our numbers make sense – and we think they do – then AI servers will crest at around 72 percent revenue share of all server spending in 2027 and 2028.

Amazing.

This is such a dramatic change it is hard to reckon. But even at these numbers, it is only $447 billion in servers 2028, which is far less than the $500 billion in AI accelerator sales that AMD is forecasting for 2028. That AMD figure implies somewhere around $1 trillion in server spending in 2028 if you assume the accelerators (mostly GPUs) represent about half of the revenues of a machine. It also implies somewhere around $2 trillion in cumulative AI server sales between 2024 and 2028 inclusive. Whatever AMD is talking about, Gartner does not think there is that much money in the market for AI servers.

The only way to find out for sure who is going to be right is to live it. And so, we will.

Expect Datacenters To Get Denser, Hotter, And Smarter

The datacenter industry today looks very different than it did a decade ago. A number of factors have emerged over the past few years: most recently, the proliferation of large-scale AI, but also the slowing of Moore’s law, and the nagging issue of sustainability. Uptime Institute expects a confluence of …

The Outlook For Infrastructure Is Cloudy – In A Good Way

If we are ever going to know what affect the coronavirus pandemic has had on the IT sector, we have to keep track of what was going on before the outbreak started to hit us hard in the first quarter of 2020. This is, in part, why the data we …

Datacenter Will Be AMD’s Largest – And Most Profitable – Business

Two and a half years into the global coronavirus pandemic we all have upgraded our home IT infrastructure. And after several fibrillatory interest rate shocks by the major governments to try to curb inflation in the world economy, spending on PCs has consequently taken a nose dive. And a glut …

With Gartner’s report, which companies will benefit the most worth investing in growth stocks?