No one like the R word, but we don’t shy away from data and calling it like we see it. And from what we can see from the most recent market research coming out of IDC, the Ethernet switch market has been in recession for two quarters now and very close to three. And that is despite the enormous demand for back-end networks for AI infrastructure.

Or, maybe it is because of it. We think this was the case for server spending since the GenAI revolution began in earnest at the end of 2022, and once companies had to shell out money to buy or rent GPU-laden machines, they did so by stretching their existing server fleets and stalling spending on shiny new iron just as Intel was ramping up its “Sapphire Rapids” Xeon SPs and AMD was doing the same with its “Genoa” Epyc 9004s. Which was unfortunate indeed for them and their ODM and OEM partners, who were counting on a server bump after companies the world over were bleeding down their overcapacity spending from the coronavirus pandemic.

Having said all of that, with the AI crowd eager to shift away from InfiniBand networks commonly used in HPC simulation systems and towards Ethernet, we expect a step function spending for high bandwidth, low latency Ethernet switches and related DPUs for controlling congestion and doing adaptive routing for AI workloads. So this is a temporary slowdown in this part of the Ethernet space.

It is hard to say what is going on with campus and edge networks outside of the datacenter, which took a big dive in the second quarter of 2024, according to IDC. And if you do the math on all of the tidbits in the statement that IDC put out and keep track of what it has said each quarter for the past several years – as we have done – then you can put together a picture of broad trends inside and outside of the datacenter.

By the way, we would have done this for the first quarter of 2024, but IDC did not put out a statement about the global Ethernet switch and router market the period ended in March. It would have normally released such Q1 2024 data in June. But in its Q2 report, IDC gave enough sequential data that we can fill in the gaps. Which is fun, and which we hope will be useful.

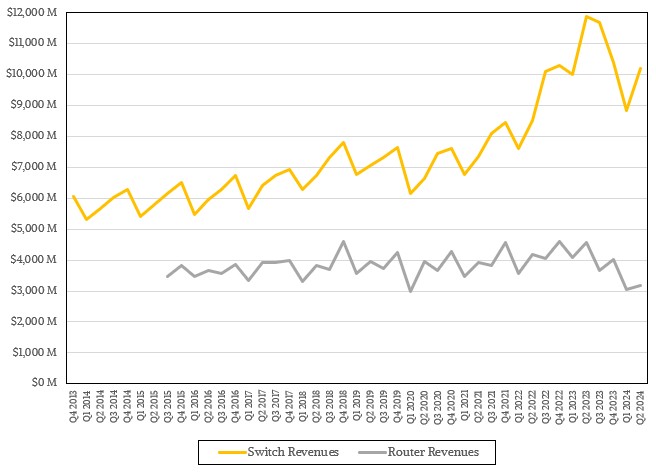

IDC says that companies worldwide spent $10.2 billion on Ethernet switching gear for datacenters, campuses, and edges in the June quarter, which was up 15.4 percent sequentially from Q1 2024 but down 14.1 percent year on year. Spending on Ethernet routers dropped by 30.6 percent to $3.2 billion.

The datacenter portion of the market, which is the one that we care about, did relatively fine, but growth has been anemic compared to historical levels in the past several years.

In Q1, based on our math with trends and historical IDC data, datacenters spent $5.26 billion on Ethernet switching, up 7.6 percent year on year and up 15.8 percent sequentially. And before you get all excited, the average growth rate for Ethernet switching in the datacenter is 17.1 percent Q1 2021 through Q2 2023, when things seemed “normal.” In Q3 2023 it was 7.2 percent, in Q4 2023 it was 4.4 percent, and in Q1 2024 it was 4.6 percent. This is not a recession, but it is slowing growth. (A recession is two quarters of actual decline, and sometimes economists and politicians say “negative growth,” which we think is perfectly asinine. And why is it not spelled assinine?) So there is something going on here that is slowing growth, as we pointed out above.

If you look out to the campus and edge part of the Ethernet switch market, you can see the recession very clearly. In normal times, the campus and edge market has averaged 20.2 percent growth, but in Q4 2023, IDC’s data, when you recreate it, shows that non-datacenter Ethernet switching revenues fell by 1.6 percent to $6.08 billion. In Q1 2024, they dropped by 24.2 percent to $4.3 billion, and in Q2 2024, they fell by 28.9 percent to $4.95 billion. (That was 15 percent sequential growth, which is something we guess.)

So there is the Ethernet switching recession at the moment. This may be a spending cut to help fund AI spending, or it may not be. Our hunch is that a desire to reallocate resources for AI is behind at least some of the spending cuts, but there is also political and economic uncertainty. You make do.

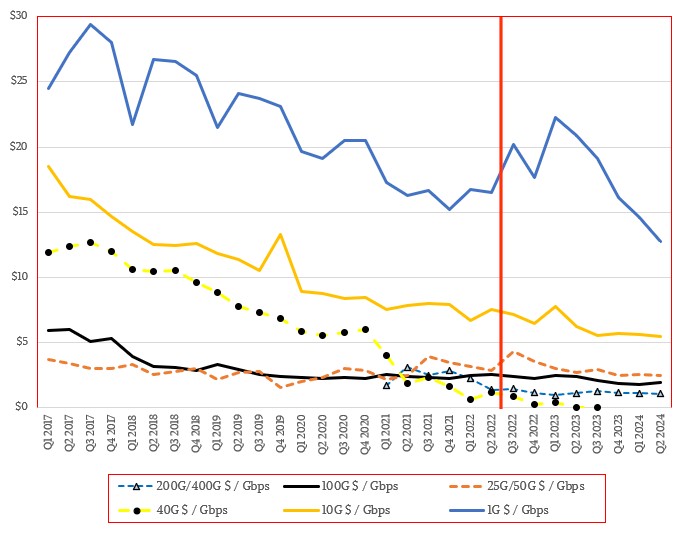

Spending on 200 Gb/sec and 400 Gb/sec Ethernet switches more than doubled in the second quarter according to IDC, and were up 35.7 percent sequentially, to what we reckon was $1.71 billion in Q1 and $2.32 billion in Q2. Spending on 100 Gb/sec Ethernet gear was down 1.7 percent to $2.83 billion, but up 13 percent sequentially from the $2.5 billion in spending in Q1. On the other end of the Ethernet spectrum, spending on 1 Gb/sec Ethernet switches was off 35.7 percent to $2.61 billion.

IDC is did not give out port counts or growth rates, and has not since the middle of 2022, so we do not have finer grained analysis. But we did our own projections on revenues inside these other segments of the market and took a stab at modeling the ever-decreasing cost per bit that companies require as they upgrade their networks. Based on our admittedly wildly speculative filling in the gaps on the IDC data, here is how the cost per bit might look out there in the real world:

Here is the amazing thing, and it is worth pointing out here. Speaking very generally, the cost per bit of 200 Gb/sec and 400 Gb/sec Ethernet switches (which are almost exclusively used in the datacenter) has been trending down from around $3 per Gb/sec of capacity in early 2021 to around $1 per Gb/sec here in early 2024. Ethernet switches at 100 Gb/sec speeds during their initial ramp were around $30 per Gb/sec and quickly busted down through $10 per Gb/sec and then eventually down to $5 per Gb/sec by 2017, and were around $2.50 per Gb/sec when the 200 Gb/sec and 400 Gb/sec devices first started rolling out. As best as we can figure, they are stalled at somewhere around $1.90 per Gb/sec.

And as the chart above shows, the cost per bit for older switch technology running at 1 Gb/sec, 10 Gb/sec, or 25 Gb/sec commonly used in campus and edge gear, is comparatively very, very high.

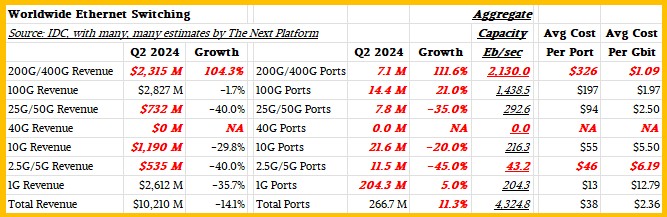

This table sums up the aggregate capacities sold by bandwidth and their relative cost per bit. There is a lot of witchcraft in these numbers, especially the port counts, but we do what we can with we have:

We just wish IDC would pout the data out like it used to in 2021 and 2022. We like to analyze data, not to spend so much time trying to fill in gaps.

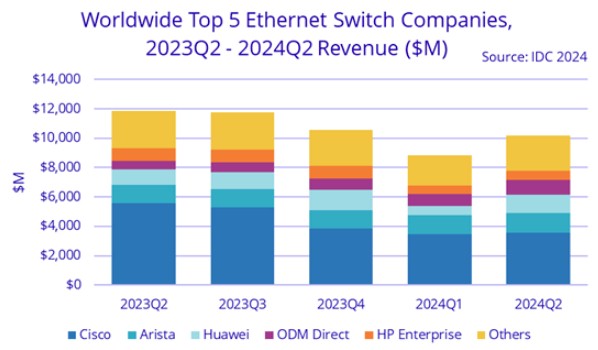

Here is how IDC presents to the most recent five quarters of Ethernet switch vendors for the top four vendors plus the ODMs as a group:

Those three quarters of Ethernet revenue recession stick out like three coins in a fountain.

We like our line chart better, which the top four vendors and Others as a group. When we have enough data, we will extract out the ODMs and plot them separately. Take a look at that Cisco Systems bump last year:

We don’t know what was going on precisely, but whatever it was, it stopped. We think it was Cisco being very aggressive trying to protect its campus networking franchise to try to blunt the attack by archrival Arista Networks, which has been trying to expand out to campus from the datacenter.

The ODMs are helping prop up the Others bigtime, but there are other vendors like H3C (the former Hewlett Packard Enterprise partnership in China) are doing pretty well, too.

In Q2 2024, Cisco accounted for a little more than a third of the Ethernet switching market, with $3.55 billion in sales, down 36.6 percent however. Arist was the number two supplier, with $1.38 billion in sales, up 12.4 percent and with $1.24 billion of that coming from the datacenter, up 15.9 percent. (We estimate Cisco had around $1.1 billion in datacenter Ethernet switch sales, but that is just that – and estimate.) HPE had $633 million in Ethernet switch sales in Q2, down 25.2 percent year on year but down 40.1 percent sequentially. HPE’s datacenter switch business is miniscule, at $87 million. Huawei Technology, the Chinese Cisco, had $1.23 billion in sales, up 15.5 percent but more than double from Q1. H3C, now the other big Chinese vendor, had $459 million in sales, down 3.7 percent.

ODM suppliers sold over $1 billion in gear into the datacenter, based on the IDC figures; we do not know how much, if any, campus and edge gear they build. ODMs had 19.1 percent share of the datacenter Ethernet switch revenues in Q2, and the ODM share is creeping up ever so slowly over time.

Server Spending Holds Up Despite Every Damned Thing

Our increasingly networked and compute-intensive lives are driving the server business, and despite the cornucopia of fear, uncertainty, and doubt that spans the globe, the appetite for compute as expressed in shiny racks of servers or metal pizza boxes or an occasional tower sitting in a closet or under a …

Ongoing Saga: How Much Money Will Be Spent On AI Chips?

Everybody knows that companies, particularly hyperscalers and cloud builders but now increasingly enterprises hoping to leverage generative AI, are spending giant round bales of money on AI accelerators and related chips to create AI training and inference clusters. But just you try to figure out how much. We dare you. …

Great Accelerations: Just How Much Will We Spend On GenAI Again?

Ever since the launch of the “Antares” MI300X and MI300A compute engines by AMD back in early December, we have been mulling over the spending forecasts for AI spending in general and for infrastructure and accelerators more specifically. With the generative AI marketing rocketing upwards on what looks like escape …

Be the first to comment