When you have to compile the revenue streams of thousands of major IT hardware, software, and services suppliers into the datacenter, it takes a bit of time to get that data, get it right, and then aggregate it for a datacenter market analysis. Which is why, here at the beginning of the third quarter we are only now getting final results for datacenter infrastructure spending from IDC for the first quarter of this year.

The good news is that the forecast for 2024 for spending on compute and storage in the datacenter is up, and up in a big way, and the projections for spending for the next five years are also higher than the last time IDC did its prognostications for compute and storage spending in the datacenters of the world.

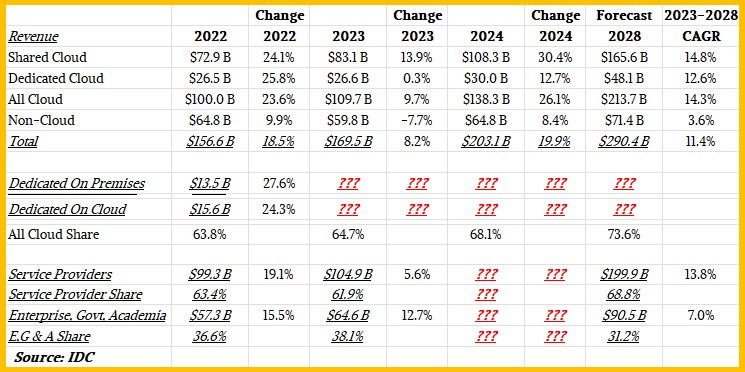

In the quarter ended in March, IDC reckons that a total of $54.4 billion was spent on compute and storage capacity around the globe. Some of that was spent on dedicated iron that will be housed in proprietary datacenters or co-lo facilities and amortized over time, and some of that was sold to shared clouds (where others will rent a slice of the machine) or in a dedicated machine (which can be located in a datacenter, co-lo, or cloud and where only one customer occupies a machine).

Important note: These revenue figures are factory sales of machinery to the end customers or to channel partners, not the rental income from the cloudy infrastructure. This is the value of machinery bought each quarter, and thus is an apples-to-apples comparison. (We would love to see, or figure out, a comparison of amortized annual revenues of non-cloud machines versus the annual rentals of shared and dedicated cloud machines. As far as we know, neither IDC nor Gartner have done such a comparison.)

This is an impressive $54.4 billion in spending, up 46 percent from the year ago period. We do not know how much of that money came from buying AI systems or renting them from the cloud, but we strongly suspect that somewhere around 40 percent of that was based on AI systems spending in one fashion or another – and the vast majority of that was for the rental of AI system capacity, mostly powered by Nvidia GPUs. The AI share of compute and storage spending could be even higher, approaching half of the total, we think. But IDC does not discuss this in its numbers – at least not publicly.

Drilling down into that spending a little, IDC says that companies spent $26.3 billion on shared cloud infrastructure in Q1 2024, up 43.9 percent from the year ago period. Spending on dedicated cloud infrastructure – what we might call hosted systems – was up 15.3 percent, but trailing the trailing 24 month average of $7.4 billion per quarter. Add them together, and spending on all cloud infrastructure – shared plus dedicated – rose by 36.9 percent to $33 billion flat. Non-cloud infrastructure – meaning normal systems acquisition – was up only 5.7 percent to $13.9 billion.

The big change we saw in IDC’s numbers this time around is that the figures for 2023 sales were rejiggered, with the split between shared cloud and dedicated cloud radically altered and the overall spending levels was also reduced by $800 million. That’s admittedly not much against a $108.9 billion aggregate spending level. But IDC did add $4.7 billion to the shared cloud spending levels in 2023 and took away $3.9 billion from dedicated cloud spending in 2023, and these are pretty big shifts.

When we see such big changes in a model, we have to wonder if it is a change in the model to increase its accuracy (meaning people’s behavior has not really changed) or if it is a new change in expected future behavior that is now reflected in the forecast.

There were even bigger changes in the compute and storage spending forecast in the datacenter for 2024. Early this year, IDC was projecting for $95.3 billion in shared cloud spending, $34.6 billion in dedicated cloud spending, and $57.9 billion in non-cloud (traditional standalone system) spending.

Now, IDC says there will be $108.3 billion in shared cloud capacity rentals worldwide this year, an increase of $13 billion and we think largely driven by massive AI spending, and a reduction in the forecast for dedicated cloud spending by $4.6 billion, down to $30 billion. Non-cloud compute and storage spending is expected to rise by $6.9 billion this year, and we think that is because enterprises will be buying AI systems as well as upgrading their existing fleets to make room for AI systems in their current space and power budgets. More efficient general-purpose servers unlock space, power, and budget for AI systems.

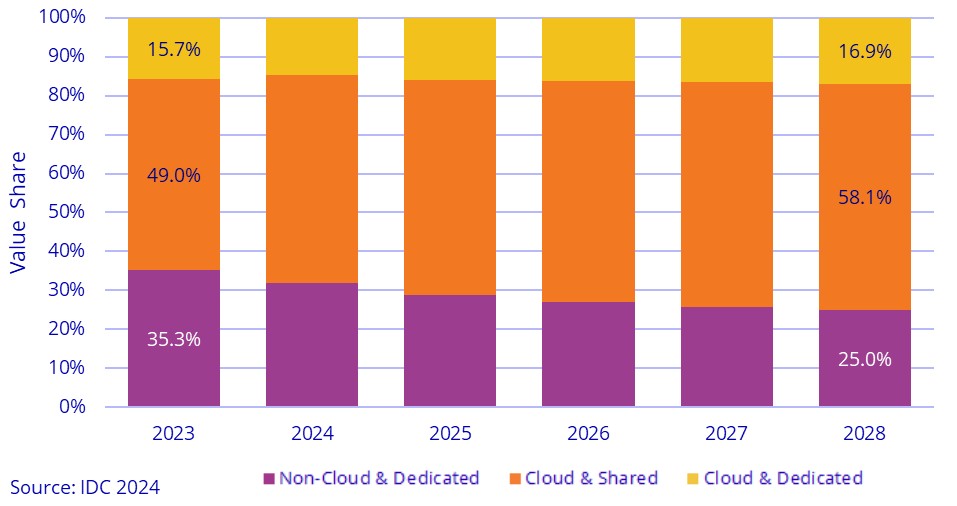

As you can see, cloudy infrastructure is expected to continue its embiggening slice of overall compute and storage buying. It was 63.8 percent of spending two years ago, 64.7 percent last year, is expected to be 68.1 percent this year, and 73.6 percent four years after that in 2028. It will take a long time to reach 100 percent if current trends persist, and they may not as current trends often do not.

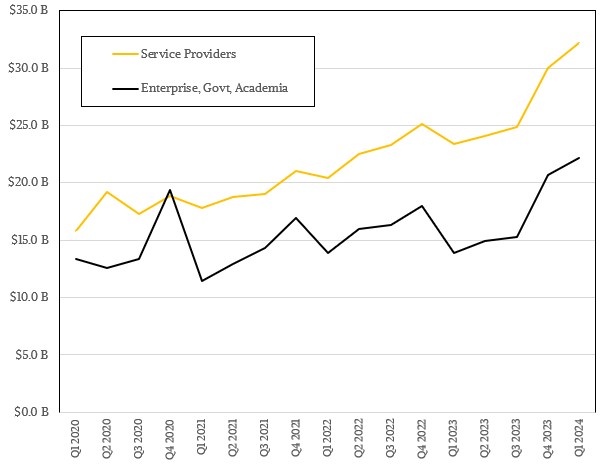

Roughly the same trend lines are happening if you look at the world of all service providers – hyperscalers, cloud builders, telcos, hosters, and other service providers – versus enterprise, governments, and academia.

The service providers as a group are not expected to see the same revenue share of overall systems sales, which is a bit peculiar. What that means is that the enterprise-government-academia organizations are setting up their own cloudy infrastructure, very likely to build sovereign AI systems but also other containerized platforms for running new applications and datastores.

It also means that some of the spending by service providers is for their own internal use to run their businesses, although how much is unclear.

Ethernet Switching Keeps Rising Despite Supply Chain Woes

Whenever demand exceeds supply, inflation is inevitable. And it is not at all surprising to find that in certain sectors of the networking space, the cost of bandwidth is flattening out instead of decreasing and in some cases is on the rise. And at least until the semiconductor market settles …

Quantum Control: More Than Meets the Eye

It is not difficult to oversimplify, even with something as complex and diverse as quantum computing, but these systems go far beyond mere qubits in deep freeze. Just like any computer, these machines have complicated control hardware and code in addition to the overall architectural and algorithmic features. With that …

With “Crossroads” Supercomputer, HPE Notches Another DOE Win

When you come to the crossroads and make a big decision about selling your soul to the devil to get what you want, it is supposed to be a dramatic event, the stuff that legends are made of. In this case, with the announcement of a $105 million deal for …

NVDA sales up $60B, DC spend on compute and storage up only $30B? Not familiar with the exact detials of IDC.

Without Nvidia, the server market would have crashed — and crashed hard — in 2023. AI has been propping it all up, and will continue to do so as “real” server buying takes time to build up steam.