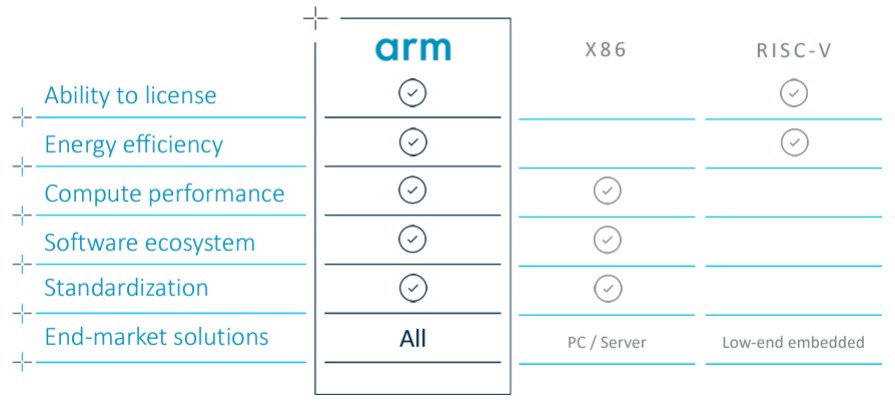

The only thing stronger than having absolute control, as happens in monopolies and oligopolies, is the strength that comes from numbers. Both are economic principles as well as technical ones, and they both come together powerfully in the IT sector in general and in the semiconductor industry specifically.

In this day and age, perhaps nothing demonstrates the strength in numbers better than Arm Holdings, which went public last fall but which is still 90 percent owned by Japanese conglomerate SoftBank. The Motorola 68000 and the IBM/Motorola PowerPC had their chances to take on all clients and embedded uses, but we summarily and quickly vanquished by Arm in the embedded space. PowerPC did their best to take over the datacenter, but the X86 architecture from Intel and AMD jumped from the desktop and beat them to the datacenter profits. Arm had the smartphone locked up from the very beginning, and X86 tried but failed there.

And now, we are in a world where Arm has become established in the datacenter, thanks mostly to the enthusiastic adoption of Arm by Amazon Web Services, first in its Nitro DPUs and then in its Graviton server CPUs, as its seeks to control more of the compute that happens within the world’s largest collection of servers and storage. And for much the same reasons, Alibaba has followed suit with its Yitian CPUs, Tencent with Zixiao CPUs, Microsoft with its Cobalt CPUs, and soon we expect Google to enter the Arm server fray with its “Maple” CPUs. Fujitsu, Nvidia, and Ampere Computing have all done their parts as well, creating unique designs that address the needs of the HPC and AI crowd, and the governments in Europe, China, and India are also supporting Arm designs for supercomputers and clouds. Meta Platforms looks like it will jump over Arm and go straight to RISC-V with its first homegrown CPUs.

Arm may not be the cheapest architecture, but it is arguably the least risky architecture on which to build any kind of compute these days. Which is why we are, as they say on Wall Street, initiating our financial coverage of the company. We will need to measure the success or failure of the RISC-V uprising in compute against something, and Arm is that something for we believe that a few stewards of the RISC-V architecture – it looks like Tenstorrent and SiFive at this point – will build licensing and royalty subscription businesses much like the one that the spun-out arm of the venerable British system maker Acorn Computers – Arm is really short for Acorn RISC Machines – to become the Arm that helped create the smartphone revolution and which has been trying to break into the datacenter since the Great Recession.

We have talked about the Arm architecture in its various incarnations long before The Next Platform was founded nearly a decade ago and with ever-increasing detail and attention since then, so nothing will change here as far as that goes here. (Head’s up: There will be a Neoverse disclosure of some sort in the next few weeks.)

We think Nvidia paying $40 billion to try to acquire Arm or SoftBank thinking that Arm should have a valuation of $60 billion was kind of ridiculous on the face of it when you consider the modest size and even more modest profitability that Arm has had over the decades. Yes, the Arm architecture it is ubiquitous. Yes, it has major advantages. Yes, it makes a very good living for several thousands of engineers and the thousands of more people who have created a very good RISC architecture and extended and evolved it brilliantly. But let’s not get carried away beyond the exorbitant valuations that the tech stocks have these days.

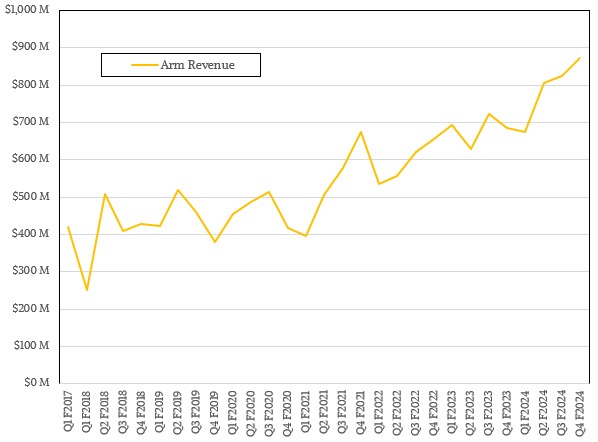

Here is the revenue trend for Arm between Q1 of its fiscal 2017 through Q4 of fiscal 2024 based on the mid-point of the guidance that the top brass at the company gave to Wall Street yesterday after the market close:

Arm will shortly break through a $4 billion annualized run rate, if current trends persist, and it may have a rosy outlook because the Armv9 architecture that debuted a few years back and that is now appearing in clients and servers has approximately twice the royalty price of the Armv8 architecture that preceded it. Speaking with Bloomberg Radio earlier today, Rene Haas, chief executive at Arm, said that the Armv9 architecture presented 10 percent of revenues in Q2, and that rose to 15 percent in Q3. The trend looks good.

But make no mistake: Arm is in a very tough business, and with RISC-V coming up and being truly open source, it can only push and pull so hard. The best thing to do is to shoot the gap between X86 and RISC-V and be the easiest architecture to deploy, and anyone watching would have to admit, the technology is sophisticated enough and the variety of options for an SoC are great enough that you can make just about anything you want out of the Arm architecture. And, hundreds of companies have done that, and it is a thing to behold.

We have nothing but immense respect and gratitude for this. Make no mistake.

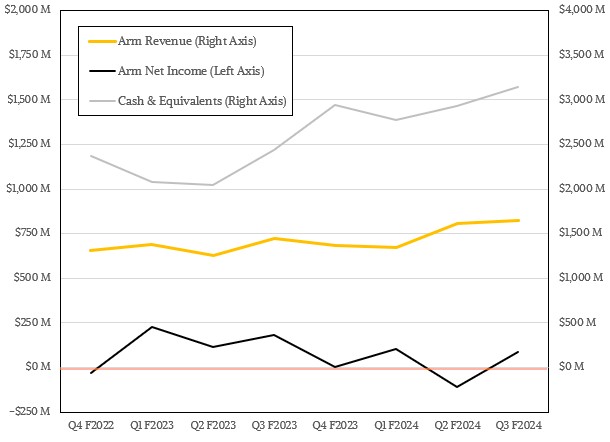

Let’s take the trailing eight quarters that Arm has talked about since it was preparing to go public and divulged in its recent financial filings. Between Q4 F2022 and Q3 F2023 inclusive, Arm has brought in $5.69 billion in revenues, but it has only brought $577 million to the bottom line. That is a mere 10.1 percent of revenues, and as the chart above shows and the table of salient financial and market statistics shows, two of those quarters had losses and one came pretty close.

This chip design licensing and royalty earning business is a tough and somewhat choppy one – like so many in the IT sector, to be sure. The S&P 500 Price/Earnings ratio is somewhere around 25 right now, and that implies that the stock of the average company in the S&P 500 index should be worth somewhere around 25 times its earnings. Arm is not part of the S&P 500, but the principle applies. As we go to press, after a shocking 50 percent increase in a single day thanks to a rosy outlook for its final quarter of fiscal 2024, Arm has a market capitalization of $79 billion. In the trailing twelve months, Arm made $85 million. So by this logic, Arm’s stock should only be worth $2.13 billion. These are perhaps not the best quarters on which to judge Arm, and maybe these tech companies deserve a better multiple. That $2.13 billion is not even covering the trailing twelve month revenues, which are a tad bit under $3 billion.

What this tells us is that Arm is not profitable enough – or consistently profitable enough – given its revenue stream. Which, quite frankly, is growing steadily but nothing like Nvidia or even AMD in the datacenter.

Let’s be more fair. Say Arm brings $200 million to the bottom line in its fiscal Q4 2024 ending in March against the midpoint of revenue. That would be 22.9 percent of revenue as profit, a killer quarter by any historical measure (but not its best revenue to net income ratio). That would justify a $7.1 billion market capitalization. The actual market capitalization today, as we approach market close, is 11.1X larger.

The “real” value of Arm is somewhere between these points, $7.1 billion and $79 billion, adjusted for the overall irrational exuberance of the stock markets in the United States, Europe, and Japan. (We don’t have the time to figure out that adjustment.)

Here’s a reality check. Nvidia has a market capitalization of $1,730 billion as we go to press, and in the trailing twelve months ended last October (its most recent annual period we know about), it posted $44.87 billion in revenues and raked in $18.89 billion in net income. Using the 25 P/E ratio for the S&P 500, Nvidia’s market capitalization should be around $475 billion. If you assume Nvidia will break $60 billion in sales for fiscal 2024 and have slightly higher profitability because the growth is driven by its datacenter business to yield $30 billion in net income, that P/E ratio implies Nvidia’s market capitalization should be around $760 billion. That is 2.3X times better than the S&P average. Why is Arm Holdings, relatively speaking, worth more than Nvidia again?

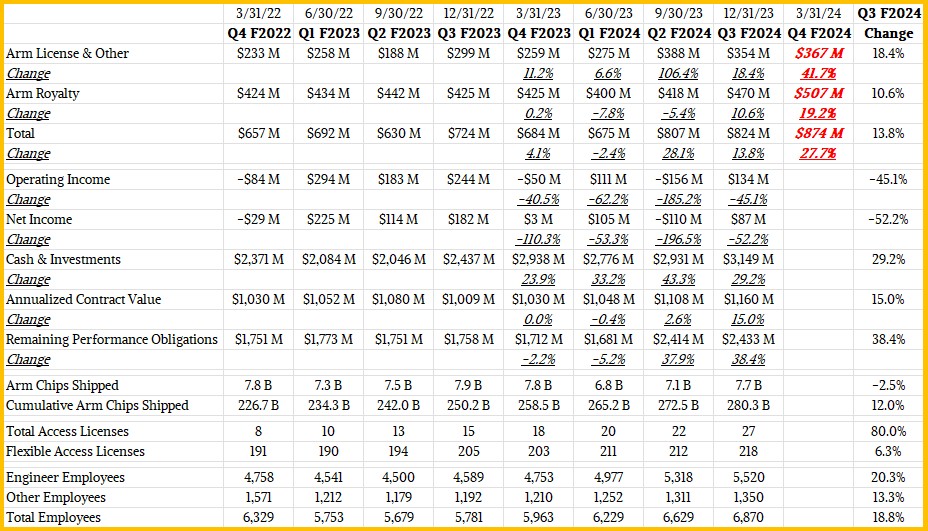

This is what is real. In the third quarter of fiscal 2024 ended in December, Arm posted royalty revenues of $470 million, up 10.6 percent year on year, and licensing and other revenues of $354 million, up 18.4 percent. Total revenues rose by 13.8 percent to $824 million. The company’s forecast for the March quarter, where revenues had dipped sequentially and it had barely made a profit at all ($3 million against total sales of $684 million), were rosier, with an expected revenue growth of 27.7 percent at the midpoint to the aforementioned $874 million. No one is silly enough to forecast net income; it could be anywhere between $100 million and $200 million, and even that is not suggestive of the range that is possible based on the limited past financials we have since Arm went public again last September.

If there is any good in this exuberance in the market capitalization of Arm, it is that the company has another financial lever it can pull in addition to the $3.15 billion in cash and investments that Arm has on had right now. Arm has plenty of financial means to keep on innovating, and this is a very good thing for the datacenter as well as the client and the edge.

The use of Arm servers is growing in the datacenter, and the impact is becoming material. This is something we have been waiting to see for a long, long time. Having an architecture in the datacenter that packs the wallop of 15 million developers and an immense stack of software. There were over 30.6 billion Arm chips shipped in fiscal 2023, and the aggregate shipments from Day One through Q3 F2024 is more than 280 billion chips. This ginormous ecosystem is why we have always believe that it was inevitable that Arm would come to the datacenter.

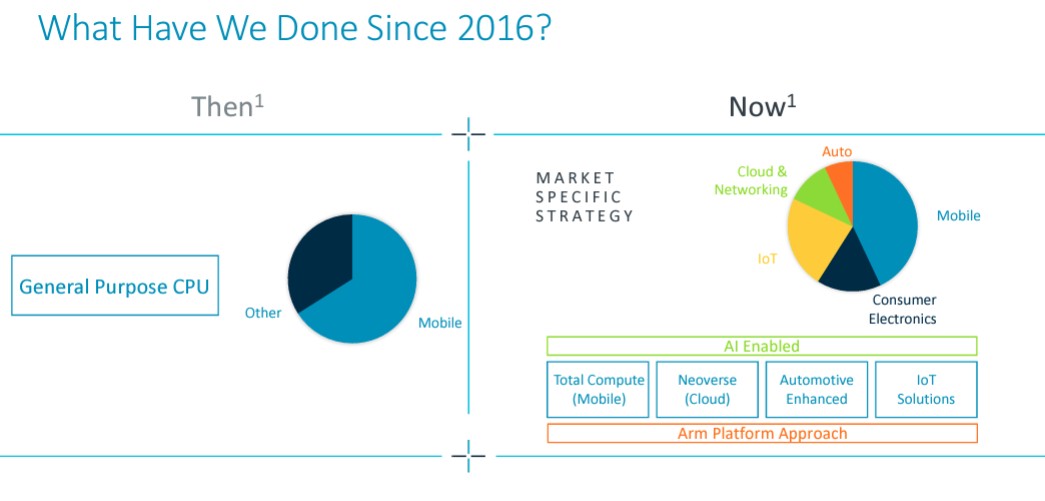

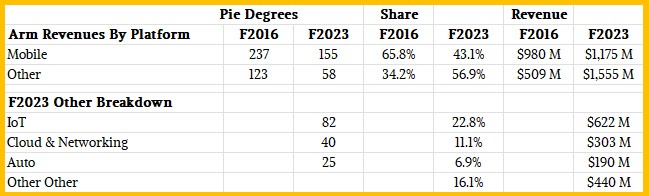

Arm doesn’t say much about the revenue streams from the various platforms that its customers build, but it did offer this chart in its most current financial presentations:

We know the revenues in those two fiscal years, and with a ruler to extend the radii in the pies and a protractor the measure the degrees, we can convert those pies to percents and figure out revenues by platform. Like this:

We know the revenues in those two fiscal years, and with a ruler to extend the radii in the pies and a protractor the measure the degrees, we can convert those pies to percents and figure out revenues by platform. Like this:

What we find most interesting is that Cloud & Networking Platforms represented 11.1 percent of revenues in fiscal 2023, and we cannot wait to hear what the share will be for fiscal 2024.

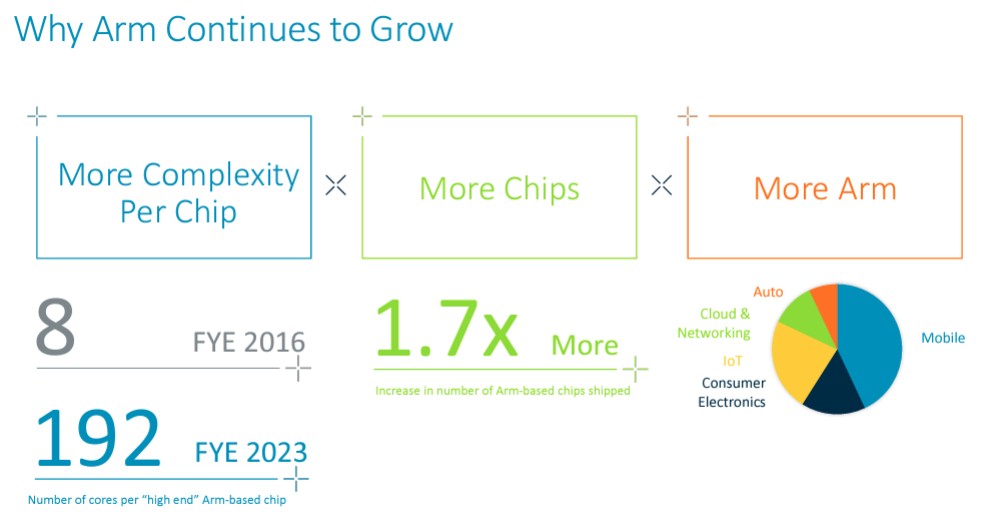

The thesis of why Arm grows, and we believe this absolutely, is that devices are using more and more content, the content is getting more expensive to license and pay royalties upon, and there are more companies doing the licensing, and these are all multiplicative effects:

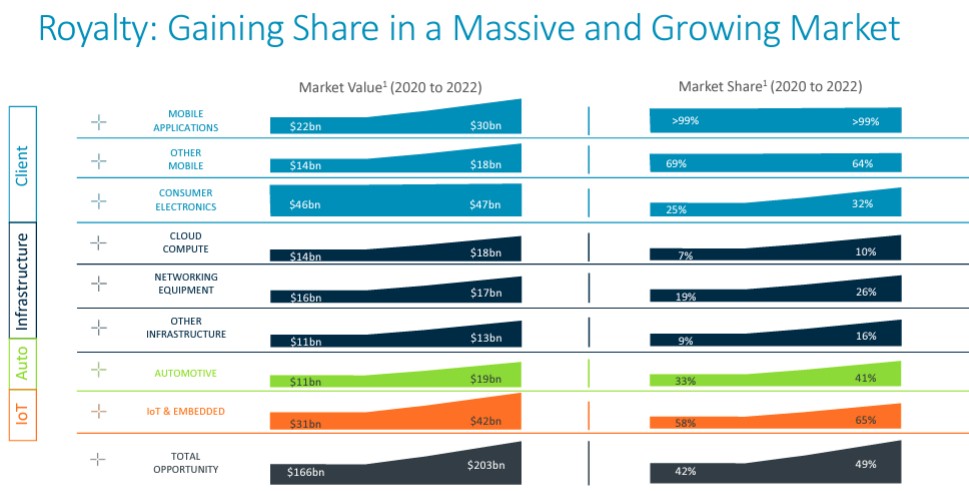

The total addressable markets for Arm’s royalties are also growing, as this chart shows:

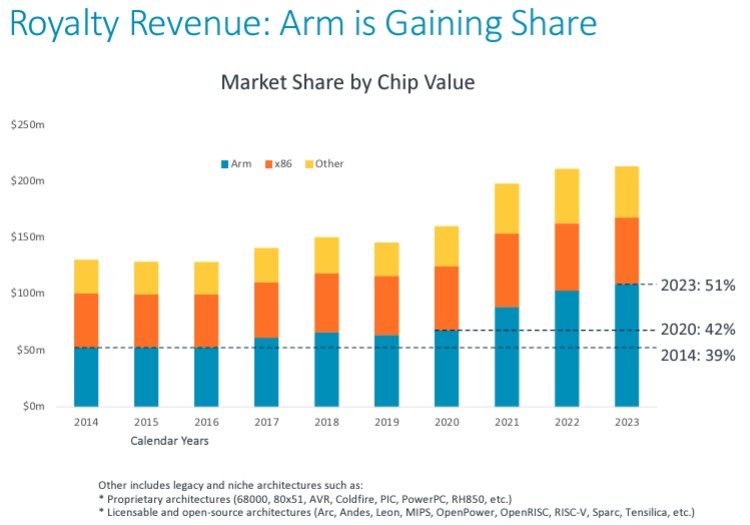

Arm is only at 10 percent of the royalty TAM in the cloud and networking area that represents the datacenter. (These TAMs are based on chip values, not on the royalties that Arm actually gets. This is also for calendar not fiscal years. So be careful mixing and matching here.)

Arm says that not only are the TAMs growing for its licensing and royalties, but its share of the royalty revenue is growing compared to other architectures across all kinds of devices:

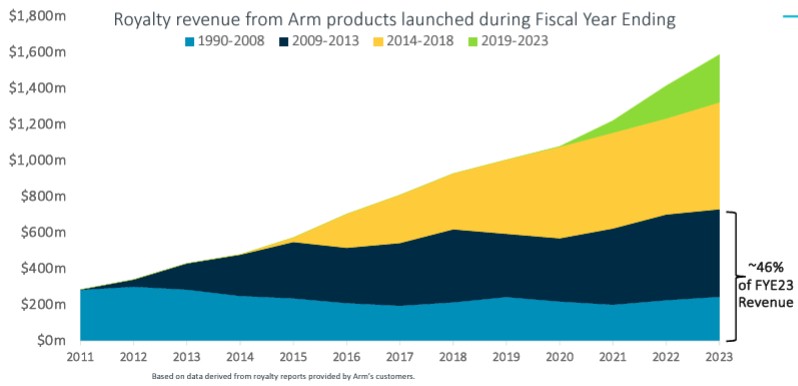

Here is the neat thing that makes a large portion of the Arm business like an annuity. Royalties keep on coming in on chippery that was designed a long time ago and that is still being used in embedded, edge, and client devices.

Servers tend to be on the cutting edge of the Arm architecture, which stands to reason. In fiscal 2023, 46 percent of the royalty revenue that came into Arm was for designs that were put into the field a decade or more ago. This is a kind of ballast to the Arm business.

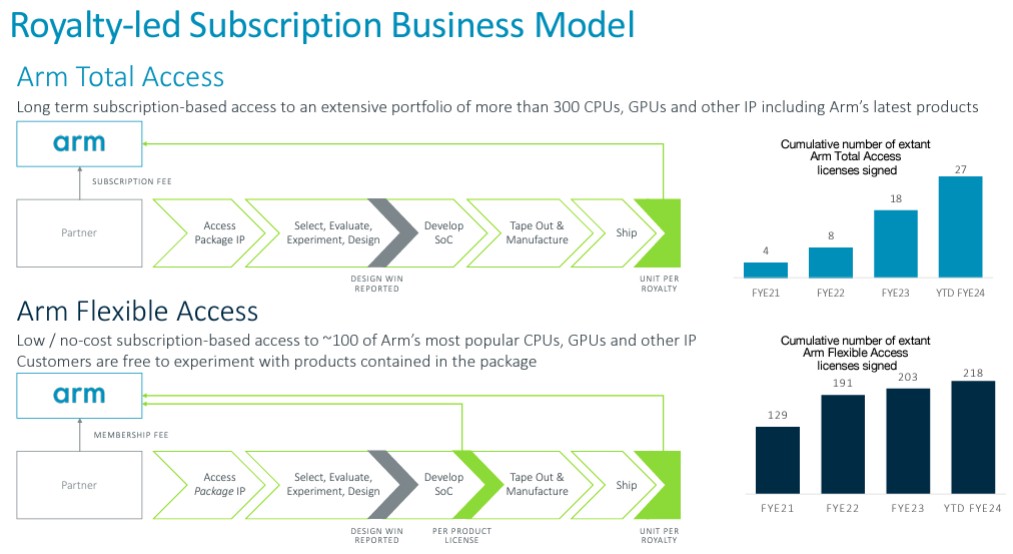

The other thing that is happening is that new companies are coming to the Arm architecture and existing licenses are moving from Flexible Access to Total Access licenses, which generate more revenues.

And even when customers take whole chunks of intellectual property from Arm to speed up their designs, which does not require the Total Access license, which allows Arm’s largest customers access to basically all of the Arm off-the-shelf IP but does not include an architecture license, they are going to pay a royalty stream on the devices they make and either use internally or sell. And, with the move to Armv9, those royalties are going to be 2X higher. (Arm still sells full architecture licenses as well.)

All of this will provide great stability to the Arm architecture and make it the safest bet if you want to create a compute engine for the datacenter in servers, storage, or switches. There will be plenty of money to continue innovating to try to stay ahead of the RISC-V pack. But we have no idea how making Masayoshi Son, the founder and chief executive officer of SoftBank, as rich as he has just become – again – makes any sense.

Ruminations About Europe’s “Alice Recoque” Exascale Supercomputer

Designing chips and shepherding them through the foundry and package and assembly is a complex and difficult process, and not having these skills at a national level has profound implications for the competitiveness of those nations. In many ways, Europe behaves more like a nation than not, and this is …

Gutting Decades Of Architecture To Build A New Kind Of Processor

There are some features in any architecture that are essential, foundational, and non-negotiable. Right up to the moment that some clever architect shows us that this is not so. What is true of buildings and bridges is equally true of systems and their processors, which is why we use the …

Who’s Going To Build The UK’s Homegrown Exascale Supercomputer?

The years-long run-up to the first exascale supercomputers was really a story about the ongoing competition between the United States and China. Who was going to get there first? How long was it going to take? How much of an advantage would the country with the first exascale systems see …

It’s great to see these positive results for ARM! Not too surprising given Apple (M1,M2,M3), Ampere (Siryn, Altra), Qualcomm (X Elite, Nuvia Oryon), AWS (Graviton), Alibaba (Yitian ), Fujitsu-Riken (A64FX, Monaka), Microsoft (Cobalt 100), NVIDIA (Grace, Jetson), SiPearl (Rhea1), and others (eg. Samsung mobile, Broadcom Raspberry Pi, Phytium Feiteng Tengyun, Huawei …) who’ve jumped into this arch’s fray, and also the recent help provided by CSS cut-and-paste design methods!

In my view, compared to ARM, for datacenter use, RISC-V is lagging in its J-extensions for dynamic languages (Java, Python, Javascript, and the likes) — it is a work in progress (challenging) as can be seen here: https://github.com/riscv/riscv-j-extension . Robbin Ehn recently provided an update, at FOSDEM ’24, with respect to OpenJDK, which both provides hope and also shows that the road ahead will be long it seems ( https://fosdem.org/2024/schedule/event/fosdem-2024-2327-unleashing-risc-v-in-managed-runtimes-navigating-extensions-memory-models-and-performance-challenges-in-openjdk/ ).

Meanwhile, even commodity ARM SOCs may include simpler support CPUs to help configure and manage some of their subsystems. The NXP i.MX8MQ (ARMv8, 4xCortex-A53, embedded-focused) for example has an internal Arc CPU to train its LPDDR4 interface, and an Xtensa CPU for configuration of its Cadence HDMI IP. Those types of functions functions could likely be performed by 32-bit integer-core RISC-V as well (IMHO).