It is just plain weird to be attending an SC20 supercomputing conference virtually and to not be going to the IDC – now Hyperion Research – morning breakfast speed forecast just a little bit hungover. (OK, sometimes quite a bit hungover, and thank you ever so much for all those years of greasy food and hot coffee.) But Hyperion did it virtually this year, and we could all see it without squinting so much, and in fact, you can see the full presentation at this link if you register.

As you might imagine, the coronavirus pandemic is top of mind at Hyperion these days, and we all want to know what impact this is having on the HPC business. And Hyperion chief executive officer Earl Joseph dove right in.

“We have spent the last six to nine months trying to understand what is really the COVID-19 impact in the overall HPC market,” explained Joseph. “We have done a lot of surveys, and about a quarter ago we thought the impacts were going to be extremely severe and now we think they will not be quite as bad.”

Most of the raw semiconductors coming out of the fabs are not delayed, which stands to reason given how automated fabs are and how clear they are in terms of air and surfaces. But once chips leave the fabs, there are all kinds of delays with circuit boards, components, assembly, and such. There are also, we know, some delays in getting products designed, which will have impacts in the future. Things will slip a few weeks to a few months – one example we know about is the Power10 processor from IBM, which is running a few weeks behind but still on track for late 2021. The delayed product shipments today are going to have a current and future impact on recognized revenues, and people not being able to attend conferences and in-person meetings also has an impact on the HPC sales pipeline. And Joseph expects that the low-end of the HPC market, where systems cost $100,000 or less, will be adversely impacted by this coronavirus pandemic impact for several years.

The upside with COVID-19 is that there is some funding to support increased spending to fight the virus, as we have reported throughout this crisis, and there is also a chance that spending of HPC systems on the public clouds could also counterbalance some of the declines. But through the first half of 2020, Hyperion thinks that the HPC market has already declined by 11.5 percent and for the full year the company’s prognosticators believe it will decline by around 14 percent. So it will be a little worse on the backend of the year.

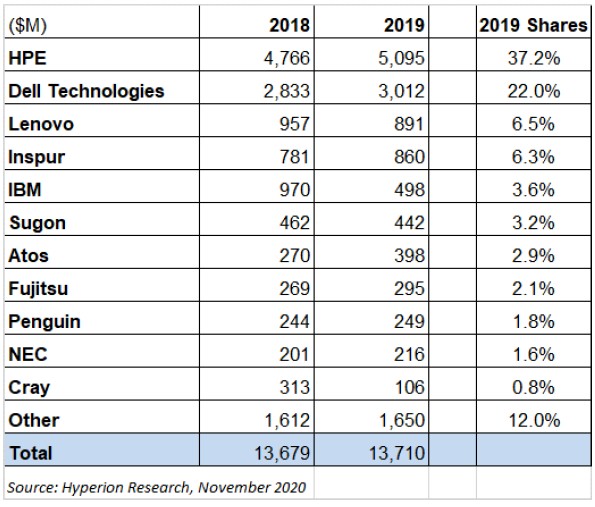

To put some numbers on that, sales of HPC servers in 2018 and 2019 were around $13.7 billion, both record-breaking years in terms of revenues but only 0.23 percent growth between 2018 and 2019:

There is a mix of Cray numbers within the Hewlett Packard Enterprise numbers in the 2019 figures, and to get a sense of how the aggregate HPC server business has grown and how much share the combined Cray and HPE businesses are doing, you have to add them. If you do that, HPE/Cray had $5,079 million in sales in 2018 and $5,201 million in sales in 2019 and thus grew 2.4 percent and has 38 percent of the market – the largest share by far. Call it more than 10X as fast growth as a relatively flat market. And clearly as revenues are being recognized for exascale systems out in 2022 and 2023, it is going to have a hell of a bump. It is unclear what the impact will be on HPE/Cray in the nearer term, and we won’t really have a sense of it until the year ends and Hyperion and Intersect360 put out their market research and HPE reports its financials. It is helpful to remember that HPE bought Compaq to get a similar share in raw servers only to have the dot-com bust and then 9/11 happen and a very aggressive Dell come up from the bottom and match its market might over the decade that followed. Market share has some inertia, but it is not an impenetrable fortress.

To be precise, Hyperion currently expects for HPC server sales in 2020 to drop by 13.6 percent to $11.85 billion. That is $1.86 billion wiped out, gone, bye-bye, and the question we have is will this be universally applied across all vendors? It is hard to imagine that IBM doesn’t lose more market share, but this will only be a tiny piece of the loss. Lenovo could keep declining as Europe gets a bit more protectionist and China is fostering intense competition from Inspur and Sugon that Lenovo also has to face. Atos will likely grow, and Fujitsu will see a bump as revenue from the “Fugaku” system ay RIKEN is recognized. Given that, it means others will be hit harder than we might otherwise be thinking, with Fugaku having a list price of $910 million, depending on the exchange rate between the US dollar and the Japanese yen.

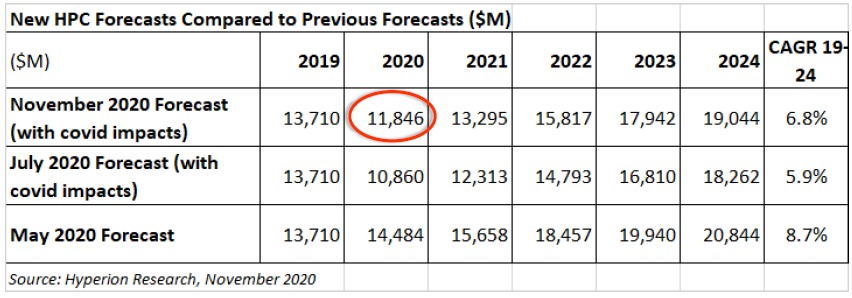

Below is the current November HPC server spending forecast from Hyperion and the ones from May and June:

We find it a bit perplexing that Hyperion did not have any COVID-19 impacts in its May forecasts, but that is a kind of baseline with 5.7 percent growth. If you do the math, Hyperion was originally projecting that between 2020 and 2024 inclusive – meaning five years over 2019 levels – that an incremental $4.79 billion in HPC spending would happen. That’s very nearly an entire HPE/Cray. And in the May forecast, that incremental spending, again inclusive across those five years, was a mere $1.65 billion. In the new forecast that incremental spending above the 2019 baseline across those five years inclusive is $2.44 billion. That means $2.35 billion in spending – something on the order of five or six complete exascale-class systems – has been removed from the market. And considering the many exascale systems that are part of this forecast and that governments will not cut spending on, that means the rest of the market is going to be hit very hard.

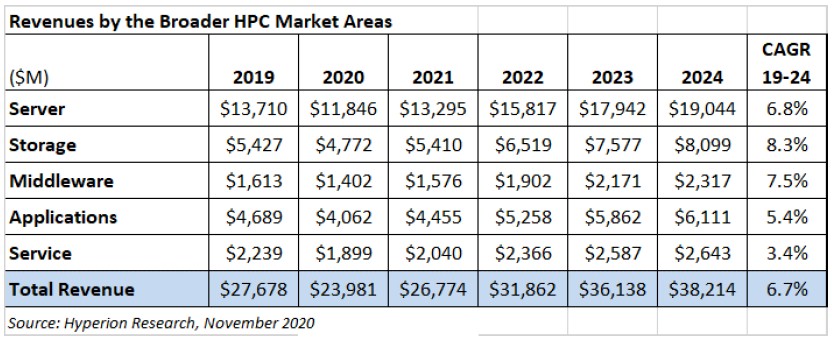

Here is the on-premises HPC spending forecast from Hyperion for all classes of spending, including servers, storage, middleware, applications, and services:

There is a pretty bad 13.4 drop in 2020 to $23.98 billion in overall HPC spending, but then it just grows and grows.

Those pre-exascale and exascale deals have a lot of their own application software development costs, but let’s ignore that for the moment and try to figure out how much of an impact pre-exascale and exascale spending has on the overall market.

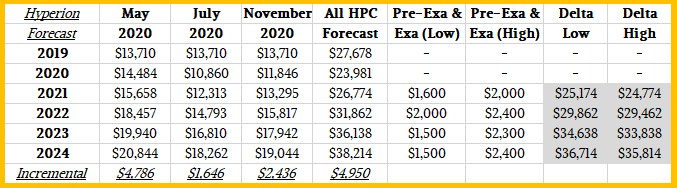

By Hyperion’s own reckoning, between 2021 and 2026, between 28 and 38 pre-exascale and exascale systems with somewhere between $10 billion and $15 billion (rounding) in revenues (including hardware, software, and services). In the 2021 through 2024 years, which is the period of the forecast for general HPC sales above, there is a possible range of spending that looks like this:

If you do the math on these models as we have done above, it assumes that at the midpoint of the pre-exascale and exascale spending collectively for each year that the growth of the HPC business (again, this is on-premises spending only) outside of this is pretty aggressive. It comes to $24.97 billion in 2021, and grows by 18.8 percent to $29.66 billion in 2022 and then grows by another 15.4 percent to $34.24 billion by 2023, with a tapering off of 5.9 percent growth in 2024 to $36.26 billion.

That is a lot of growth for a market that is undergoing huge transitions. We are not saying that anyone can predict this better, but we are saying that we have entered an era of widening statistical uncertainty.

Look at it this way: There has never been a better time for massive investments in systems to help anchor the HPC business a little. And we hope it stays that way. And before this is all done, there may be a very large HPC cloud business picking up some of the slack that is not seen in this on-premises HPC sales data, as Joseph correctly pointed out in his presentation. And if these pre-exascale and exascale deals do not all get fully funded because the economy goes on the skids, they are somewhere between 5 percent and 7 percent of the market. We need to worry more about the broader HPC market than the upper echelon.

The only way to truly predict the future is to live it. And that we will, and we shall see.

Ayar Labs Brings National Lab Architects And Industry Leaders Together To Talk Disaggregation

If you think HPC architectures have changed rapidly in recent years, brace yourself for the future when things will be moving at light speed. As scientific workloads have grown more variable and demanding, and applications like AI have brought large but fluctuating data demands, tightly coupled systems have been stretched, …

Will HPC Be Eaten By Hyperscalers And Clouds?

Some of the most important luminaries in the HPC sector have spoken from on high, and their conclusions about the future of the HPC market are probably going to shock a lot of people. In a paper called Reinventing High Performance Computing: Challenges and Opportunities, written by Jack Dongarra at …

TSMC Makes The Best Of A Tough Chip Situation

If you had to sum up the second half of 2022 and the first half of 2023 from the perspective of the semiconductor industry, it would be that we made too many CPUs for PCs, smartphones, and servers and we didn’t make enough GPUs for the datacenter. Or rather, Taiwan …

Be the first to comment