The semiconductor manufacturing business is absolutely immense. To give the numbers some perspective, in 2024, chip makers generated revenues that were about three quarters of the size of the US defense budget and about two-thirds the size of the social services budget allocated by Congress. And spending on chip manufacturing is growing as more capacious devices are ending up in more products and new workloads – notably artificial intelligence – are driving whole new areas of incremental and now large spending.

Gartner has put out its annual casing of the chip business recently, and we have always taken a look at it out of the corner of our eye when it comes out, but we have not really put the public data set together over a long term and then analyzed it as is our remit here at The Next Platform. Now seems as good a time as ever, so we went back over the past decade of reports from Gartner and assembled the dataset of chip sales by vendor, filling in some blanks where some data is missing in the public reports. Thankfully, all of the major chip makers – and by this, we mean chip designers not the foundries that make the chips, which is how people have always spoken colloquially about these companies.

With the exception of Intel and Samsung Electronics, who operate foundries that have advanced processes, none of the other companies “making” chips but who are really designers, have foundries of their own. And of course, Taiwan Semiconductor Manufacturing Co is the world’s largest foundry and has no interest in becoming a “chip designer” that sells either through channels or directly to personal device or datacenter system makers. And in the case of Apple, which made the annual semiconductor maker rankings for the first time in 2021, the company designs its own chips and makes them for its own devices, which it sells to consumers and companies directly.

This is an interesting distinction, and we wonder how long it will be before Amazon Web Services, Google, Microsoft, Azure, Alibaba, Baidu, and Tencent make the list as “chip makers” given the substantial investments in CPUs and AI accelerators all of these companies are plowing into their datacenters. It cannot be long if Apple is making the list. And particularly with half of all compute engines being based on homemade Graviton Arm server chips and big investments in Nitro DPUs, Trainium and Inferentia AI accelerators for training and inference, and maybe some homemade network switch ASICs, AWS should make the top dozen before too long and be the first of the hyperscalers and cloud builders to make the list. Google and Microsoft are vying to be the second of the datacenter players to make the list. (And for all we know, they should have already displaced some companies at the bottom of the ranking.)

Let’s give you all of the data so you have it:

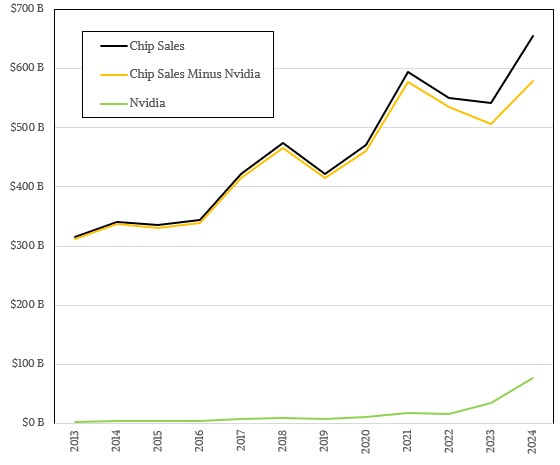

Semiconductor revenues in 2024 were 2.1X higher than they were in 2014, and even if you take AI juggernaut Nvidia out of the mix, revenues across all chip makers rose by 1.85X over those eleven years.

In 2024, chip revenues rose by 21 percent to $655.9 billion. We wish we had some idea of how many chip shipments were not last year, and a decade ago, but this is very hard to reckon. Public companies talk about their money and profits, but they are usually not very specific about their unit shipments.

The first thing to notice is that it is very hard to change a market this large. Even the explosive 120.1 percent growth of Nvidia’s chip sales during this GenAI boom doesn’t move the numbers by as much as it feels like it should. This makes it more clear:

Nvidia is the largest semiconductor maker in the world, which is one hell of an accomplishment, and it is not done growing unless the global economy flies up its own bunghole. And, frankly, given the nature of the AI workload to displace people and cut costs, AI adoption might be accelerated by a global recession, not stalled by it. (We have always contended that recessions accelerate transitions; they do not stall them.)

What is safe to assume is that Nvidia has the lion’s share of chip manufacturing profits, and that is because of its unique position as the compute and networking supplier for GenAI workloads. We can’t prove that, but that is out informed opinion. In fact, we think that TSMC and Nvidia account for the vast majority of the profits being created by the GenAI boom thus far.

The other thing you will not about the chart above are the boom-bust cycles for the memory makers, of which Samsung, SK Hynix, and Micron Technology are the biggest three. There are also spending spikes that are related to those boom bust cycles and compute engine cycles that often synchronize to drive that sawtooth pattern of annual chip sales we see in that chart above.

Here is another chart, which summarizes the chip revenues for the past eleven years for the top chip makers in the world:

The CPU and AI accelerator makers are shown with dashed lines, and the memory makers have markers on their solid lines. Broadcom is a solid orange line because it is really its own animal, and if Marvell was big enough to make the top dozen cut, we would see up there.

Given the trends and our own forecasts for revenue going out to 2029, Nvidia, which took over the top slot from Samsung in 2024, is going to be the world’s largest chip maker for a long time. It is not clear that Intel can grow, but we think that AMD can grow as being the alternative to Intel in CPUs and the alternative to Nvidia with GPUs.

Qualcomm does not provide much in the way of datacenter gear, and has played around here and there, but is not really interesting to us until it does. Ditto for Apple, which makes its own processors for its phones, tablets, and PCs but which has yet to make server CPUs and AI accelerators for its own workloads. Rumors abound that it is working on both, of course.

It would be interesting to see homegrown datacenter XPUs broken out separately here, with all of the datacenter chips lumped together, much as Gartner lumps all of the original design manufacturers (ODMs), who are the real manufacturers of systems installed by the hyperscalers and cloud builders, into a single ODM category in its quarterly server revenue reports. (IDC does the same.) It would also be interesting to see what share of chips go into end user devices, which ones are at the edge, and which ones are used in the datacenter.

Perhaps Gartner will indulge us in future reports.

Talking Silicon Photonics Signal And Noise With Andy Bechtolsheim

There is a lot of chatter this week about optical communications with the OFC2022 conference being held in San Diego. We have more than a passing interest here at The Next Platform in silicon photonics and co-packaged optics, and had a chat with Andy Bechtolsheim about what was happening in …

Interview: Post-Earnings Insight With Nvidia CFO Colette Kress

After Wall Street closed the markets for the day and Nvidia reported its financial results for the second quarter of fiscal 2025, we had the opportunity to chat with Colette Kress, chief financial officer of the accelerated computing giant. We wanted to get a better handle on how the delays …

What Faster And Smarter HBM Memory Means For Systems

If the HPC and AI markets need anything right now, it is not more compute but rather more memory capacity at a very high bandwidth. We have plenty of compute in current GPU and FPGA accelerators, but they are memory constrained. Even at the high levels of bandwidth that have …

Gartner has Apple’s 2024 market share as 3.1%, not the 1.0% in your spreadsheet. It seems to be wrong for the other years too.

Just an error in the equation in that row. Sorry about that. It is fixed now, and now we don’t have to worry about that for another decade or more. . . .