For the past five and a half years, which is not quite an eternity in the IT business but is something akin to a half of a generation or so, IBM’s revenues have been declining, quarter in and quarter out. As has happened many, many times in its more than century of existence, Big Blue, which used to be a peddler of meat slicers, time machines, scales, and punch card tabulators early in its history, has had to constantly evolve and reimagine itself.

The transformation that IBM had to undergo in the late 1980s and early 1990s was a near death experience for the company, and the dot-com boom allowed Big Blue to recover and become a behemoth of servers, software, and services and recover. But others grew faster in the dot-com era, and the emergence of hyperscalers and public cloud builders – often these companies are both – and their own brand of compute, storage, networking, data analytics, and now artificial intelligence are giving IBM all kinds of direct and indirect competitive pressures, despite some fine engineering work on its own in all of these fields.

That transformation, as is evidenced by the most recent financial results for the company, is far from over. The top brass at IBM is no doubt sick of waiting for this transformation to be accomplished, but the same could be said of its IT supplier peers. Dell liked Wall Street so much it spent a fortune going private and wants a bigger piece of the datacenter so badly that it paid a handsome sum for server virtualization juggernaut VMware and enterprise storage giant EMC, the latter of which we no longer have visibility it. Hewlett Packard Enterprise is in perpetual change mode, too. Oracle bought Sun Microsystems to become a player in the entire stack, but Oracle’s hardware business is also under pressure and it is trying to build up its cloud presence much as IBM is with SoftLayer/Bluemix. Dell and HPE just gave up on building their own clouds because they can’t compete, and VMware commissioned Amazon Web Services to carve out what is in effect an ESX-NSX-vSAN public cloud that VMware could sell. Cisco Systems, which made its mark in systems, especially with telco service providers, is trying to get a handle on this as the whole market tilts toward hyperscale and public cloud. This is a tough time to be in the IT business in many regards, and it is hard to squeeze a profit out of any of this IT stack except for CPU, memory, and flash hardware and certain pockets of systems software.

That doesn’t mean there isn’t innovation, and we do not mean to imply that IBM is not innovating. It is just harder to extract huge profits from an IT market that has lots of different options, and many of them open source code that might have higher risks but it generally runs on commodity X86 iron and is free to license even if the support contracts still cost money.

The fact is, even if IBM’s turnaround is frustratingly slow, at least it is not collapsing as the company was back in the early 1990s, until Big Blue was recreated as a system reseller with a neutral database, transaction processing, and middleware stack with a huge services arm that would integrate and optimize any system or process that companies threw at it. IBM has sold off all kinds of hardware businesses because they were inherently unprofitable for the company to stay engaged in, such as high-end printers, PCs, disk drives, and X86 servers, and it has hoped that its SoftLayer cloud and Power Systems machinery would grow in the market while the mainframe would stabilize and generate its extremely profitable pull-through of software and services.

No matter how IBM dices and slices itself, at its heart, it is still a systems company, although it is trying to move up the stack to more profitable cloud infrastructure, Watson-derived AI applications (many of them only available as hosted products on IBM’s cloud), and other data analytics and custom research engagements. It is not a bold strategy so much as a predictable one, given who IBM is, what it can do, and who its paying customers are.

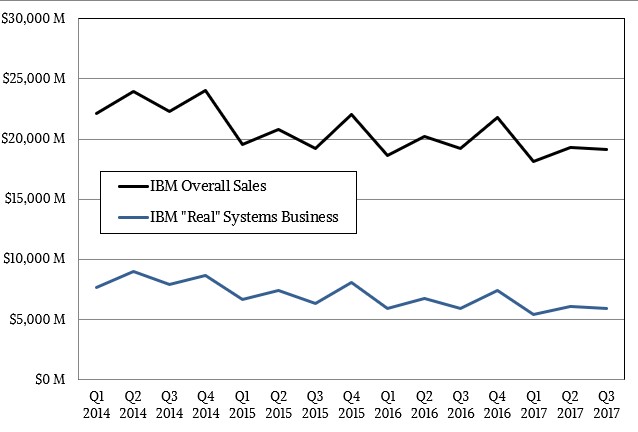

In the third quarter ended in September, IBM booked $19.15 billion in sales, down four-tenths of a percent from the year ago period, and net income was $2.73 billion, down 4.5 percent. For a decade or so before it had to undergo its latest transformation, IBM was able to grow revenues in the low-to-mid single digits and earnings per share by the single digits, which made its executives who got stock compensation as well as Wall Street investors very happy. But sooner or later, buying back the immense number of shares that IBM did for two decades to prop up those EPS numbers gets harder and harder to pay for, particularly when IBM has business units, like the System z and Power Systems divisions, that are not as large or as profitable as they once were and their replacements in the IBM portfolio, like Watson and Bluemix, have not yet filled in the gap completely.

And thus, IBM is in a holding pattern, yet again. But the System z and Power Systems upgrade cycles may save the day in the coming quarters and buy IBM some more time with a little more sales and profit. The System z14 mainframes, which were announced in July with new processors, started shipping in the last two weeks of September. Interestingly, the revenues outpaced the amount of compute capacity (as measured in the MIPS metric that originated with mainframes more than five decades ago), with revenues up 62 percent and aggregate MIPS sold or activated on existing machines up only 33 percent. The underlying cost of the new System z14 machines make up the bulk of the difference in revenues, and toward the tail end of the z14 product cycle, maybe three or four years from now, most of the MIPS sales will be to activate latent capacity on existing machines, not whole new systems or upgrades to them, which obviously cost more.

In the case of mainframes, a lot more. And because of that, IBM’s overall systems hardware business had a 14 percent increase even as the Power Systems business fell by 8 percent in the quarter. Martin Schroeter, IBM’s chief financial officer, said on a call with Wall Street analysts this week that high-end Power Systems running its AIX operating system had a revenue bump – we think because customers know that the future “Fleetwood” Power E970 and Power E980 machines are not coming until later in 2018 with the new Power9 chips, so they are buying Power8 machines now at what we presume are pretty steep discounts. IBM has been able to win some Linux system and cluster deals on Power8 iron, and Linux is now the default operating system on 20 percent of the Power Systems machines that IBM ships, up from a few percent a few years ago. (The number of machines shipped has fallen steadily, however, so this is as much about a decline in AIX and IBM i, Big Blue’s own operating systems on Power iron, as it is about the rise of Linux on Power.) It doesn’t look like the initial shipments of the Power9 server nodes for the “Summit” supercomputer at Oak Ridge National Laboratory or for the “Sierra” system at Lawrence Livermore National Laboratory had much of an effect on Power Systems sales in this quarter. We presume that more machines will ship in Q4, and that should help a lot. Along with a full-on mainframe ramp, it looks like IBM could have a pretty good quarter for systems as the year comes to a close. And the first quarter might look good, too, as more Power Systems iron is launched.

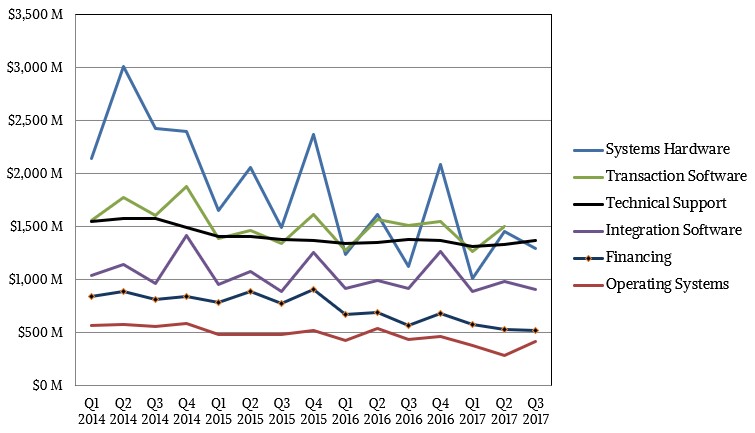

IBM’s storage hardware sales rose by 4 percent in the quarter, according to Schroeter. IBM did not say how much revenue this accounted for. Software defined storage, such as hyperconverged and parallel file systems, had double-digit growth, but is reported in the Cognitive Solutions stack. (Inexplicably, really. It belongs in systems, just like middleware does.) IBM’s operating systems business fell by 3 percent in the quarter, to what we believe was about $420 million, compared to $1.3 billion for systems hardware, down 3 percent and up 14 percent year on year, respectively. That yields a gross profit of $924 million for IBM’s reported systems business as we estimate it, up around 16 percent for the third quarter. Pre-tax income, now that the investments in the z14 and Power9 processors are largely done and some mainframe sales came in, were up by a factor of 2.5X to $339 million. It is hard to guess what will happen in Q4, but the odds favor a pretty big revenue jump for systems as IBM reports it.

We don’t think IBM’s classification of its own business really reflects how much business it does in systems, and that is why we go through the different divisions and estimate what share of their sales goes into the actual systems that IBM builds and sells. There are database and middleware programs, as well as tech support and integration and financing services, that are sold as a bundle with its systems – this is what we call IBM’s “real” systems business.

For these “real” systems figures, we take all of the systems hardware, operating system, and transaction software sales Big Blue has each quarter, plus 90 percent of its integration software, 75 percent of its technical support and financial revenues, and add it all up. In the third quarter of 2017, this number came in at $5.93 billion, down by the same four-tenths of a percent as IBM’s overall sales, and represented 31 percent of IBM’s overall $19.15 billion in revenues. We further estimate that the gross profits for this “real” systems business at Big Blue came in at $3.38 billion, down 2 percent, but still a healthy gross margin at 57 percent of revenues and, importantly, representing 38 percent of the company’s overall gross profits of $8.8 billion in the quarter. This may be a smaller business than it once was, but this “real” systems business is still quite large, and it will now be entering a new upgrade cycle that will give Big Blue some fuel to invest and expand its market.

It would be nice to see IBM actually embrace its own Power9 systems, with GPU acceleration, on its own cloud and actually build a hybrid cloud that offers to enterprise customers what it has built for Oak Ridge and Livermore.

Alternatively, why can’t IBM build the CPU-GPU cloud and just secure it and rent time on it to such HPC centers? Why is this not all one big, secure utility spanning many datacenters and regions, making money to help pay for its expansion. That’s what Amazon did when it created Amazon Web Services. So why not have IBM HPC Services? It used to be called Supercomputing On Demand, as you well know. But now, this time, IBM can actually make it happen. Why is IBM waiting? It cannot wait for Google and Rackspace to maybe embrace Power9 for analytics workloads. The profits will be in the running of the cloud and the economies of scale from building massive clouds. IBM, which got its start renting time on mainframes before a lot of us were born, should know this better than anyone. And building an AI-HPC cloud, as we are suggesting, means competing with some of its customers and also supporting standard machine learning frameworks. IBM did its own distribution of Hadoop, and maybe it needs its own variant of TensorFlow on Power-Tesla hybrids running at scale on its cloud.

Managing Infrastructure At Cloud Scale Without The Hyperscaler Propellerheads

As more enterprises embrace hybrid and multicloud strategies and begin to extend their IT reach out to the edge, scale becomes an issue. Red Hat, a longtime player in the datacenter thanks to its Linux distribution and related systems software, has worked hard over the past decade to establish itself …

Big Iron Will Always Drive Big Spending

Starting way back in the late 1980s, when Sun Microsystems was on the rise in the datacenter and Hewlett Packard was its main rival in Unix-based systems, market forces compelled IBM to finally and forcefully field its own open systems machines to combat Sun, HP, and others behind the Unix …

The Memory Area Network At The Heart Of IBM’s Power10

It must have been something in the cosmic ether. Apopros of nothing except the need to fill a blank page with something interesting back when we were analyzing IBM’s second quarter financials and considering the options that Big Blue has with the “Cirrus” Power10 systems it will be launching about …

You nail it when you pose the question “why not?” I can tell you some of the answer. What you are describing in a hyper-scale AI cloud geared for HPC and mainframe hybrids is a robotized self-learning machine matrix that would – if built – end of life several thousand jobs over at big blue.

This is the crux of the whole transformation issue with IBM, Cisco, Dell (with EMC/VMW), HPE, Citrix and a few more. In order to build a service systems series of platforms in an on-demand world, you have to write code that will allow the service systems to run themselves. AI injection is in some ways not too different than taking poison to kill a tumor. You know you are potentially sowing the seeds of your own demise in order to buy some more time against the thing that is immediately threatening to wipe you out.

AI is the top hiring area at Google, Amazon, Microsoft, Facebook, IBM and many more. Those people will invent the groundwork for making redundant tens of thousands, or hundreds of thousands of tech workers over the next decade. It’s already happening. Look at Citrix, for example.

The true terror on the IT side is that the machines being built and injected into clouds do not need much more in terms of hands-on human intervention. Microsoft can run a million square foot container data center with 10 or less people per shift.

As of the end of the year in 2015, IBM employed roughly 378,000 people worldwide. In five years, if IBM stays on the path it’s trying to take in cloud (and if it were to embrace your ideas as put forth here), there is a strong likelihood IBM would employ perhaps one-tenth of the number of people it does today. That means they could shed more than 300,000 jobs. The executives know this and they need to prop up the stock via buybacks for as long as possible so they can parachute out with their chunk intact.

Thus, the partial answer to your question: inside at IBM, it is employees who are slowing this transformation as the pray they can make it to retirement, or to at least build up enough time that they can get some larger severance down the road.

Change is indeed coming. It’s arriving as I write this. Reporting on the sunny, interesting side of this is one thing, but there is a massive human flip side to the AI cloud coin.

Cloud computing biz doesn’t only builds on economy of scale , but also on better utilization of hw . Large hpc system tends to utilize hw well , probably due the costs of setup . I think this is the reason cloud hpc is a niche market.

For the AI ondemand workloads the larger cloud providers already have the lead there , big company ibm won’t be able the compete with them .

Cloud computing biz doesn’t only builds on economy of scale , but also on better utilization of hw . Large hpc system tends to utilize hw well , probably due the costs of setup . I think this is the reason cloud hpc is a niche market.

For the AI ondemand workloads the larger cloud providers already have the lead there , big company ibm won’t be able the compete with them .

Cloud computing biz doesn’t only builds on economy of scale , but also on better utilization of hw . Large hpc system tends to utilize hw well , probably due the costs of setup . I think this is the reason cloud hpc is a niche market.

For the AI ondemand workloads the larger cloud providers already have the lead there , big company ibm won’t be able the compete with them .