The era of Hewlett Packard Enterprise’s envious – and expensive – desire to become IT software and services behemoth like the IBM of the 1990s and 2000s is coming to a close.

The company has finalized its spinout-merger of substantially all of its software assets to Micro Focus. HPE has already spun out the lion’s share of its outsourcing and consulting businesses to Computer Sciences and even earlier had split from its troublesome PC and very profitable printer businesses. These were spun out together to give the combined HP Inc a chance to live on Wall Street and because PCs and printers, whether they are sold to commercial entities or consumers, naturally go together.

From this point forward, HPE will be a leaner, meaner datacenter hardware and systems software machine, and given the tectonic competitive pressures in the glass house and the immense purchasing power and technical prowess that the hyperscalers, cloud builders, and telecom service providers – what HPE calls its Tier 1 customers – can bring to bear, HPE may have to be a whole lot leaner that it is mean.

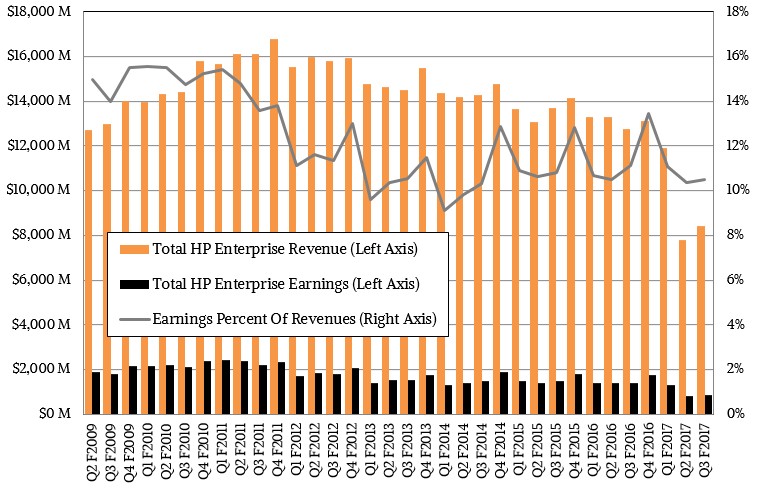

The company’s third fiscal quarter of 2017 ended on July 31, and just as it had completed the software spin-merger with Micro Focus, HPE put out the financial results for that quarter, and it is the last time we will see HPE’s software business, the one that was supposed to grow up into something that could compete with IBM’s Software Group, which has kept that IT giant profitable for the better part of two decades. HPE misunderstood how much of IBM’s software profits were driven by its own systems – although Big Blue never likes to admit it – and so it never did successfully create an analog to Software Group, with its immense gross margins. And so, HPE has hunkered down on hardware and related systems software and services, and damned near all of it acquired through its Compaq (and therefore also DEC and Tandem), 3Com, 3PAR, Aruba Networks, SGI, and now SimpliVity and Nimble Storage. The latter two deals, done this year, give HPE its own hyperconverged storage and a more modern, all-flash storage array, and SGI has contributed mightily to HPE’s server growth in the quarter, too, and its sales prospects in HPC and data analytics going forward. So did the exorbitant pricing for DRAM and flash memory, which helped prop up server revenues, but which also cut both ways in that HPE had to absorb the considerable extra costs for these core components of modern systems.

In the third quarter, HPE’s revenues rose by 2.6 percent to $8.21 billion, but taking out the effect of the spun-out software business to Micro Focus and nominal currency effects, then the core remaining HPE business had 6 percent growth and hit $7.5 billion in sales. This business will likely bop between $7 billion and $8 billion a quarter from here on out, with profitability being anyone’s guess. So much depends on component prices and competition in servers, storage, and switching.

Interestingly, if you take out sales of the Tier 1 providers that HPE sells iron to from the third quarter numbers, revenues were up 10 percent, according to Meg Whitman, the former eBay executive who has been running HP and then HPE for more than six years. (And incidentally, in the call with Wall Street analysts, Whitman said she is also an investor in ride sharing pioneer Uber and confirmed that, at the last minute, she had been asked to be considered for the CEO role at that tumultuous and disruptive company, but in the end she decided she had plenty to do at HPE and was staying parked there.)

The server business did a bit better in the fiscal third quarter, due primarily to better sales execution, according to Whitman but also thanks to acquisitions like SGI and Aruba. The core server revenue – meaning that among small, midrange, and large enterprises who are not those Tier 1 companies – rose by 13 percent in the quarter, and for the calendar Q2 period, HPE expects to show share gains overs rivals Dell, Lenovo, IBM, Oracle, Fujitsu, and its other server rivals. (We suspect that Sugon and Inspur will gain even more share than HPE, and not through acquisitions.)

Drilling down a bit, Whitman said that the Synergy composable system, which we detailed here, is gaining in momentum, with over 600 customers so far and, ironically, is driving sales of traditional ProLiant c7000 blade servers, which have an upgrade path to the Synergy systems and which exhibited double digit revenue growth in the period.

Tim Stonesifer, HPE’s chief financial officer, said on the call that server revenue was flat at constant currency, and by our math, they were down 2.1 percent to just a hair under $3.3 billion. Excluding those pesky Tier 1 customers, the core server revenues at HPE rose by 12 percent, and it is likely that some of this was due to Intel’s “Skylake” Xeon SP processor launch, which came three weeks before the end of the quarter. We think that given the huge premium Intel is charging for the Skylake Xeon chips over their predecessors, there could be a significant bump in revenues for ProLiants using these chips as well as a chance to absolutely clean the barn out of older “Haswell” and “Broadwell” Xeon E5 and Xeon E7 systems that are missing a bunch of Skylake features but which, particularly at discounted prices, will offer bang for the buck that is better than Skylake systems in many cases.

Either way, HPE wins. So there is that.

HPE has gotten the first wave of its ProLiant-hosted SimpliVity hyperconverged storage out the door, and this is also being counted as server sales, not storage sales, and this line grew by 200 percent in the quarter. (This is just as reasonable as doing it the other way around, and this is also from a very small installed base and revenue stream.) Having just acquired Nimble Storage for $1.2 billion, that helps tell a good storage story, and even with 3PAR array revenues down 9 percent, overall storage revenues rose by 11 percent to $844 million. (Our charts have previous categorizations for storage, which have been shifted around a bit, so we are showing higher growth rates compared to Q3 fiscal 2016.) All flash array sales, mostly through the addition of Nimble’s products, grew by 30 percent in the quarter.

As far as the HPC sector goes, Stonesifer said that the core business without SGI added in had grown on its own by 10 percent, and with SGI tossed in it had grown by 40 percent. SGI did about $125 million a quarter when HPE acquired it, and that implies that the core HPC business (which includes servers, storage, and switching we presume) at HPE is around $420 million per quarter and around $1.7 billion a year or so. (Those are very rough estimates, but there you go.)

The networking business did well, thanks to the Aruba edge networking products that, quite frankly, are saving HPE’s cookies in this segment of the datacenter. Stonesifer said that wired switching rose by mid single digits in the period, and Aruba wireless products had growth of over 30 percent, and overall networking revenues were up 16 percent to $702 million. (We don’t know how much HPE’s reseller agreement with upstart switch maker Arista Networks is helping here, either.)

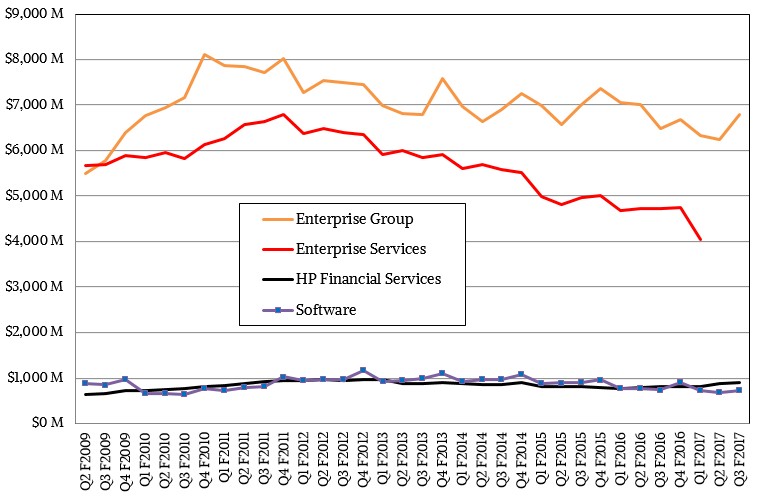

Add the Technology Services division, which saw a 2 percent revenue bump, into the mix, and overall Enterprise Group sales were up 2.7 percent to $6.79 billion. And if you take out those Tier 1 suppliers, Stonesifer said that Enterprise Group would have posted 9 percent growth.

So let’s recap. Taking out those Tier 1 players from the mix, the remaining overall HPE business grew by 10 percent, Enterprise Group grew by 9 percent, and servers grew by 12 percent. That is not only not too shabby considering the current climate in the datacenter, it also gives us a chance to see how big that Tier 1 business is and what the rest – what we will call the core enterprise – looks like, too. Here is our best shot at modeling it:

Obviously, there are a lot of ways to fit data to these points that Whitman and Stonesifer revealed on the call with Wall Street. But we think this is pretty close to what is probably the truth. We are guessing that HPE is selling a fair amount of servers, switches, routers, and other products and services (such as modular datacenters, consulting and planning services, and such) to these Tier 1 customers, and our model reflects this. And it also shows how far this business has fallen off in the past year.

It is no wonder, then, that HPE is trying to figure out what to do with the Cloudline servers that it makes in conjunction with Foxconn and that it has more recently expanded into a hyperscale storage line.

“Tier 1 continues to be a headwind for us,” Whitman admitted on the call. “It is a very lumpy business with not much profit attached to it. And so we need to figure out what the long term answer is on Cloudline. And so we are evaluating that right now.” Whitman added that HPE hoped to have it all sorted out by its security analysts meeting in October.

It is interesting to us that, several years ago when Amazon Web Services was a substantial customer for Rackable Systems, which was then bought by SGI, that SGI’s top brass walked away from a pretty large cloud server business because it could not make margins. Dell lost its deal to make custom servers for Facebook in much the same way, and Google has been using ODMs for a long time as has IBM’s Bluemix (formerly SoftLayer) cloud through its partnership with Supermicro. This is a tough business, but it is also tough – and perhaps foolish – to walk away from it.

First and foremost, working for the Tier 1s means solving some of the toughest problems in the datacenter, and the engineering that comes out of that can – and should – trickle down to the enterprise. (And also government and academic datacenters, for that matter.) And by making machinery for the Tier 1s, any vendor keeps their volume purchases for components high enough to command better prices for those components than they might otherwise get. This is a kind of profit, too. And absent this – like IBM when it first sold off its PC business and then its System x X86 server business – component costs bought at relatively low volumes can make it hard to compete. Then again, so does not being able to make any money.

With HPE sitting on $6.5 billion in cash once the software spin-merger is done, perhaps it is time to start thinking a bit differently if it is really going to be heads down in infrastructure for the hybrid cloud. HPE is only throwing off $400 million a quarter, so buying Arista Networks, which has a market capitalization of $12.7 billion, would be problematic. (No more so than Dell buying itself from Wall Street and then buying EMC and VMware for truly enormous sums.) White box server maker Supermicro, which has a market capitalization of $1.3 billion, is an easier acquisition – if HPE didn’t mind selling parts to the channel that often sells against ProLiants. There are, no doubt, other potential acquisitions. Nutanix is, at $3.2 billion, probably an affordable acquisition, and would have been cheaper if HPE had done it years ago. But HPE undoubtedly wants to grow the SimpliVity product rather than buy Nutanix and confuse itself and its customers.

That leaves the core enterprise, where Dell fights very hard and wins about half the time and where the Chinese vendors are very keen on protecting their turf. HPE indeed has its work cut out for it to keep and grow its infrastructure business.

HPE Converts Analytics, Storage, Data Protection To GreenLake

Since launching GreenLake in 2018 and promising that all of its portfolio would be available as services by next year, Hewlett Packard Enterprise has been on a sprint to build up the capabilities of the platform. That has only accelerated since Antonio Neri took over as CEO in the wake …

With DPU-Goosed Switches, HPE Tackles VMware, Security – And Maybe HPC And AI

Pendulums are always swinging back and forth in the datacenter, with functions being offloaded from one thing and onloaded to another cheaper thing that is often more flexible or faster. So it is with network functions that were originally in distinct devices, then pulled onto CPUs during the software-defined networking …

HPE Walks Away From Risky $700 Million AI Deal

This probably happens more than we know, but sometimes OEMs and ODMs walk away from big deals because something is fishy. And that happened to Hewlett Packard Enterprise in its fourth quarter of fiscal 2024, a period that ended on October 31, as it “de-booked a large order” for $700 …

HP, like IBM before it, only better, used to make great Computers for the consumer; but, again like IBM, they offered noticeably less for a greater cost.

You would see HP’s Laptop and ‘Brand X’, with HP offering 768P and the others 1080P – the other’s CPU clocked a bit higher and had extra Ports or a CD Drive; all for a couple of hundred less.

If HP had matched Specs and charged more or fell behind on their Specs but charged equal many would have chose HP over the unknown brand – it’s because HP wanted both last year’s tech at inflated prices that fewer and fewer people bought HP.

That’s what lead to their decline in the consumer market, free Printers and expensive Ink Cartridges couldn’t make people buy their Computers when others (Epson for example) were making great enough Printers to charge for them and sell you the ink too (without really dabbling in the computer market).

It was a repeat of IBM’s mistake except IBM sold last year’s tech for double the cost of offshore products being mass produced (in both increasing numbers and quality).

Soon IBM was out of the few homes that could afford an IBM computer followed shortly thereafter their exit from small and medium sized businesses.

IBM then turned it’s focus to big business (who had money) and stuck to it’s irons, Big Iron, never abandoning the old Mainframe but instead focusing on it – which does make some money off of fewer people, but tosses the huge and lower profit market that brings in enough to pay the bills while awaiting big business to slowly upgrade their prior purchase.

And, now HP follows the same path; splitting off HP to HPE and then selling of all the bits and pieces to focus on appeasing Stockholders but holding nothing to sell (product or service) – save for their Cloudline and continuing with their ‘tried but true’ (last year’s tech, but now this year’s CPU, at a noticeably greater price than the competition (like Dell or Supermicro or going a different direction, Oracle).

It’s like HP wants to keep the lights on, sell lanterns and fuel; but they sell way more fuel than lanterns, make too few great lanterns; and wonder why the lights are going out.