People control the purse strings for datacenter budgets, at least for the time being until CFOs are replaced by algorithms, and that is one of the reasons why it is hard to predict precisely what enterprise, hyperscale, HPC, and cloud organizations will do in any given quarter when it comes to spending on infrastructure. Economies are always changing, and that means a lot of fitting and starting.

While chip maker Intel has very good visibility into its largest customers, who buy direct from the company, it does not have the same ability to take the pulse of millions of enterprises worldwide that have machines using its processors running their businesses. And so forecasting what will happen in its own business from quarter to quarter and year to year is inherently tough.

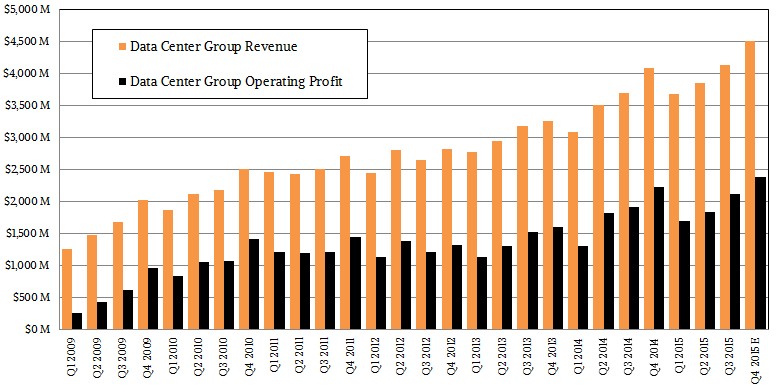

To its credit, Intel actually makes forecasts, and being such a key component of the IT stack, this is important because it sets the pace and expectation level for the industry. In the past several years, Intel’s forecasts for its Data Center Group, which makes processors, chipsets, and other components that go into servers, storage arrays, and switches, have been mixed in that it has been a little too aggressive on spending in the enterprise and pessimistic about its prospects in hyperscale, HPC, and cloud. The third quarter ended in September, as it turns out, was a bit of a surprise for Intel again, and it looks like the fourth quarter might be a little softer than originally expected, too.

This is not the end of the world, and Data Center Group is faring a lot better than Intel’s Client Computing Group, which is falling faster than the Data Center Group is filling in the gap. (You begin to see now why Intel is trying to accelerate the adoption of cloud computing, both public and private varieties.) The PC market is slowing as companies take longer and longer to do refreshes and more and more users depend on tablets and smartphones for a substantial portion of their work. While this is driving utilization on commercial and consumer cloud-based applications, Intel is not the processor of choice for smartphones and tablets, and therefore is not benefitting from this shift on the client side. Hence, in the September quarter, the Client Computing Group saw revenues drop by 7.5 percent to $8.51 billion. That’s a decline of $685 million. And while Data Center Group pushed revenues up by 11.9 percent to $4.14 billion, to make up the client chip drop, this datacenter portion of Intel would have had to boost sales by 18.5 percent.

If you want to be generous and count the Internet of Things Group and a very big chunk of Intel’s fast growing flash storage business as part of a broader datacenter group, which is logical in a way, then Stacy Smith, Intel’s chief financial officer, says that this business represents just under 40 percent of revenues that target datacenters, or about $5.6 billion in the quarter ended in September. Part of Intel’s problem with Data Center Group is that it is not putting its flash memory sales that are going into datacenters in the Data Center Group financial category, and doing so would be very interesting indeed. Intel’s memory business grew 20 percent in the third quarter, and on the conference call with Wall Street analysts going over the numbers, CEO Brian Krzanich said that more than 80 percent of the flash drives that Intel sells are going into datacenters. If you want to call the IoT Group a different animal entirely from the datacenter business, then if you do a little math on Intel’s numbers, Data Center Group plus 80 percent of the flash business came to around $4.88 billion in the third quarter by our estimation, up 13 percent year-on-year.

We do not know how profitable the flash business is for Intel, but it is less than for its core processor and chipset business in Data Center Group. We do know that Intel brought in $2.13 billion in operating income for Data Center Group in the third quarter, which is 51.4 percent of revenues for this group and which increased by 9.3 percent compared to the year-ago period. Product volumes were up 6 percent and average selling prices for components rose by 6 percent.

Whatever happened in the third quarter, Intel’s revenues grew faster in Data Center Group than profits – a situation that vendors usually like to have in reverse. The upside for Intel is that if current conditions persist, Data Center Group will drive more profits than the Client Computing Group. The bad news is that the PC business is not what it used to be, and very likely will never be again.

Two decades ago, Intel depended on client volumes to help fund the development of server chips and to ramp up its fabs to the wicked level of efficiency and advanced technology that they have today. Ironically, the profits from the datacenter business are what is allowing Intel to keep pressing ahead with advanced processes, but as Smith pointed out on the call, one of the reasons for the hit on the Client Computing Group’s bottom line is that the 14 nanometer ramp is a little more bumpy and expensive than Intel anticipated and offset some of the upselling that Intel did with “Skylake” Core processors in the quarter. These same 14 nanometer processes need to be perfected before Intel can roll out the “Broadwell” Xeon E5 v4 processors, which are expected in the spring of next year. Intel will want to have good yield on 14 nanometer manufacturing to increase its profits on the Broadwell Xeons, or otherwise it will have to make up the revenue and profits with level prices or perhaps even a slight increase per unit of compute on certain SKUs.

Intel did not give out precise metrics for the categories it tracks for its Data Center Group revenues, but Krzanich said on the call that “strong cloud and networking volume” drove this part of Intel in the third quarter. Smith said that the memory business would continue to grow at a “fast pace,” but that because of macroeconomic issues, the both the Data Center Group and the IoT Group would see weaker than expected growth in 2015 than Intel had been forecasting as this year got started, and this is predominantly due to weaker sales into the enterprise segment, which accounted for $6.7 billion of Intel’s $14.4 billion in Data Center Group revenues in 2014. The forecast for this year is for “low double digit” revenue growth for all of 2015 instead of at least 15 percent growth. Despite the blip in 2015, Smith said that Intel was not changing its long-term forecasts for 15 percent growth in the Data Center Group every year out to 2018.

In our own forecast shown above for Q4 2015, we expect Intel to bring in $4.5 billion in revenues in Data Center Group, up 10 percent from Q4 2014, and $2.39 billion in operating profits, a little lower than the year-ago period but still better than the first three quarters of 2015. That puts Data Center Group at $16.2 billion in sales with $8.08 billion in operating margins for all of 2015, and it makes it one of the richest segments of the IT economy. The cloud segment will drive about $4 billion of that revenue, by the way.

In the past, Intel has been very clear that it does not think that cloud will eat into enterprise sales, but perhaps it is time to re-examine this idea. It may have certainly been true up until now that enterprise revenues for Intel chips and components tracked with the gross domestic product of the local economies, but with companies shifting workloads to the clouds and running workloads across companies, driving up efficiencies, maybe it is reasonable to expect a downdraft in enterprise server revenues. Or at least diminished growth prospects. Ditto for any company moving to cloudy infrastructure internally.

Having virtualized their systems to drive up utilization, now companies are ready to start orchestrating and automating workloads like hyperscalers and HPC centers do, and when they do that, some compute capacity that might have been acquired is not. It is not as simple as saying that for every three or four processor cores in a datacenter running at 15 percent to 20 percent utilization there is one running in a cloud at 65 percent utilization, but that is the ratio of utilization in traditional IT infrastructure and on public clouds. The public clouds are growing because they are adding customers and those customers are adding workloads, but it would take three or four times the iron to do it the old-fashioned, unshared, unautomated way. The collapse of revenues for mainframes, proprietary minicomputers, and Unix servers was due in part to the excellent virtualization that was made available on them, and companies started using them. (It was also due to the shift away from these machines and towards X86 iron, make no mistake.)

Intel seems to be assuming perfectly elastic demand for compute once customers get virtualized and automated – Data Center Group general manager Diane Bryant mentions Jevon’s Paradox at just about every briefing – but appetites may get satiated and budgets could shift away from hardware and towards software. That is certainly what happened on these other platforms, much to the chagrin of the vendors who manufactured these systems.

We suspect that enterprises are trying to figure out how to use as few servers as possible – whether virtual or physical – and are not interested in adding more capacity per year. The hyperscalers and HPC centers of the world certainly can double their footprint every couple of years, and telcos and other service providers need massive infrastructure to offer new services. But enterprises will be looking to leaner virtualization techniques and platform clouds internally and a mix of public cloud infrastructure rented on demand to do more with less money – and less iron than they might otherwise use. If Intel has not built this into its models – and we are not saying that it has not – then it may be looking at revising its long-term Data Center Group revenue projections sometime soon. It is hard to say what will happen because, as we said, people are in charge and they are somewhat unpredictable, relying on hunches as well as data to make decisions. GDP is predictable with some big error bars, and so are our reactions to it, and not because people are bad or silly, but because information is thin and imperfect even if data is big.

It would be interesting to put these forces under tectonic pressure, with ARM servers coming to market at the same time as the software stack for them is ready and a recession starts in, say, mid-2016 or so. We are not making that prediction, but just pointing out that those conditions would certainly stress the Xeon business and see how much price elasticity there is in the Intel machine and just what the appetite might really be there among hyperscalers and HPC shops for an Intel alternative. Without such pressure, ARM servers may not get traction in the datacenter for many, many years.

One thing for sure is that we will know what happens after it does, and only then might we be able to explain it.

What Would You Do With A 16.8 Million Core Graph Processing Beast?

If you look back at it now, especially with the advent of massively parallel computing on GPUs, maybe the techies at Tera Computing and then Cray had the right idea with their “ThreadStorm” massively threaded processors and high bandwidth interconnects. Given that many of the neural networks that are created …

Can Graviton Win A Three-Way Compute Race At AWS?

One of the main tenets of the hyperscalers and cloud builders is that they buy what they can and they only build what they must. And if they are building something from scratch – be it flash controllers using FPGAs a decade and a half ago or custom Arm processors …

AMD Firing On All Compute Engine Cylinders

A few years ago, it was hard to imagine how AMD would have survived without re-entering the datacenter with its CPU and GPU compute engines. And now, it is hard to imagine how the chip maker could have possibly thrived without a revitalized GPU compute engine business. Intel knows a …

Be the first to comment