Intel’s decades-long hard work in vanquishing most of the competing processor architectures from most of the workloads in the datacenter is paying off. Just as the PC market has hit the skids again, the chip maker is firing on all cylinders with its processors for servers and storage and is getting in position to take a big bite out networking. Despite some lumpiness in the key hyperscale, cloud, and HPC markets and some skittishness among enterprises to spend money on systems in certain markets, it all seems to average out for the company.

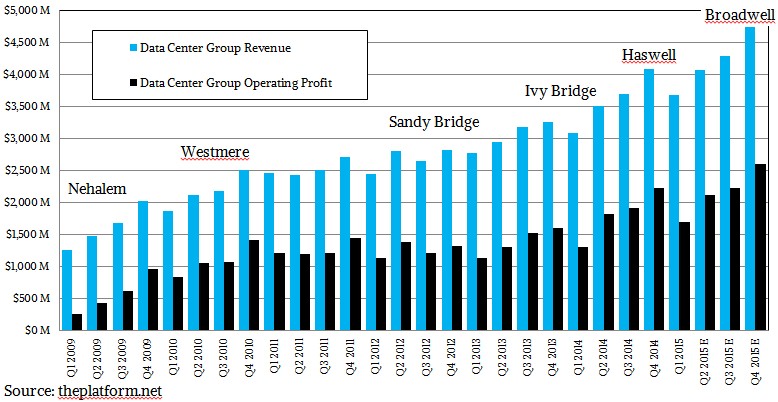

In the first quarter of 2015, Intel’s Data Center Group reported revenues of $3.68 billion, up 19.2 percent over the same period in 2014. Operating profits for the quarter came to $1.7 billion, up 23.7 percent. That is the kind of spread – 46.2 percent of revenue dropping to the middle line before taxes, investment gains and income taxes are taken into account to calculate net income – that any hardware vendor in the modern age of commoditized hardware would kill for. A richer mix of products and lower unit costs helped push up the operating profits. (There is a legion of ARM suppliers trying to gird their loins to try to take that away.) As profitable as Data Center Group was in the first quarter of this year, it did not top second and third quarters of 2014, which with 52.5 percent of revenues for Data Center Group dropping to the bottom line, was more profitable. In the final quarter of 2014, operating margins were 54.5 percent. This was during quarters last year was when everyone was expecting the launch of the “Haswell” Xeon E5-2600 v3 processors in September 2014, but it was also when Intel was ramping chips to cloud and HPC customers who get motors well ahead of announcement these days.

In the March quarter this year, unit volumes in the Data Center Group rose by 15 percent and average selling prices increased by 5 percent. (Intel does not report its chip shipments for Data Center Group as it does for client devices.)

In a conference call with Wall Street analysts, Intel CEO Brian Krzanich said that the Xeon E5-2600 v3 processors, which are known as the “Grantley” platform when you talk about Haswell Xeons, chipsets, and related motherboards, accounted for 50 percent of two-socket processor volumes in the first quarter. Krzanich said that custom versions of the Haswell Xeon E5s – and there are dozens of them that are tailored for specific customers – helped Intel to achieve record revenues in the cloud sector (which for Intel means hyperscale, cloud, and service provider customers).

While not wanting to jinx the Data Center Group business, Krzanich said that he believed that the unit could deliver growth of 14 percent to 16 percent over a period of several years, but Data Center Group has beaten this level in 2014 as a whole and in the first quarter of 2015 thus far.

In the chart above, we have shown the dominant generation of the Xeon processors available for two-socket servers at the time. These are the workhorses of the datacenter and account for the bulk of Intel’s revenues and profits. We have estimated what the final three quarters of the year might look like as Intel ramps towards its “Broadwell” Xeon E5 launch.

Interestingly, Intel’s NAND flash storage business grew by 14 percent in the quarter, and Krzanich said that the 3D NAND chips that it pre-announced without much detail with partner Micron Technology a few weeks back would be available in the second half of this year. The 3D NAND chips will allow Intel to put 3 TB of capacity on an M.2 memory stick and 10 TB on a 2.5-inch SSD. (The revenue from server-class NAND storage is not added into Data Center Group, but is included in the “All Other” category. This doesn’t make a lot of sense, but it helps that All Other category not look as bad as it already does, in terms of money lost.) It will be interesting to see where Intel parks the $200 million its Intel Federal unit took down as the prime contractor for the “Aurora” massively parallel supercomputer being installed at Argonne National Laboratory, which is based on the company’s future “Knights Hill” Xeon Phi processors and its Omni-Path 2 interconnect. This should be in the Data Center Group, but may end up in All Other.

Because of decreasing demand for the PC business, Stacy Smith, Intel’s CFO, said on the call that the company was cutting back on its capital equipment spending for 2015, and is backing off its investments by $1.3 billion to $8.7 billion. In addition, Intel is cranking out chips for inventory using its 22 nanometer processes and then beginning to wind down some of this 22 nanometer gear to make way for a further ramp for 14 nanometer processes, which are used for “Broadwell” and “Skylake” variants of its processors as well as for the “Knights Landing” Xeon Phi massively parallel processor. The first Broadwell Xeon chip, the Broadwell Xeon D, was announced in March, aimed at microservers, and Broadwell Xeon E5 server chips as well as Core Skylake chips are expected to debut at Intel Developer Forum in August. Krzanich said that the yields on the Broadwell products were better than expected, which is why it can cutover to 14 nanometer processes a bit faster. And because Moore’s Law can’t stop yet, Intel is already ramping up its 10 nanometer capacity and will accelerate this in the third and fourth quarters, which will incur increasing costs.

Intel would not comment on the rumored talks it has been having with Altera to acquire that maker of field programmable gate array (FPGA) chips, which just so happens to have chosen Intel a few years back to be the foundry for its FPGAs. Altera would be a very expensive acquisition for Intel – something on the order of twice its annual capital expense budget, which is a big deal for a $50 billion company. There are now rumors that Intel is interested in buying network chip rival Broadcom, which is coming on strong with a very good ARM server processor code-named “Vulcan” later this year. If it was tough to buy Altera, it would cost about three times as much to buy Broadcom, which has a market capitalization of just under $27 billion as we go to press. Yes, Intel plus Broadcom would be a powerhouse. Yes, antitrust authorities would have a conniption fit. Yes, it is too expensive. And yes, Wall Street and the rest of us all like to play with these ideas.

Here is all Krzanich would say on the subject of acquisitions: “Our strategy in investing in this business and what we do with our cash has not changed. And it is really the same strategy that it has been before me and that is always first, investment of business, and we firmly believe in that. Investment in Moore’s Law, new architectures, technology, and things like that. Then M&A at times, and then share buybacks and dividends.”

Until something radical changes, Intel has control of the server processor and the bulk of storage processors. It needs to do better in networking, and it can do that without having to buy Broadcom – and for a lot less money. The other option, of course, is to sell off the Ethernet ASIC business to Broadcom and partner very tightly, making sure that Xeon and Atom processors are tightly coupled to Broadcom switch ASICs rather than ARM processors. This also seems unlikely. Intel wants to compete here and win, and it has the fabs to get an advantage if it can get its switch chip designs ramped up. Intel is the underdog here, with Broadcom having maybe 65 percent market share of switch ASICs in the datacenter.

For the first quarter of 2015, Intel booked $12.78 billion in sales, essentially flat, with operating income of $2.62 billion and net income of just under $2 billion. Data Center Group represented 53.7 percent of total operating profits in the quarter. Intel does not want to make any costly acquisition or spending mistakes that upsets the flow of black ink from the datacenter to the bottom line.

Intel Back To Playing The Long Game, Not The Wrong Game

The supply chain is holding back the server business, and not just in the way you are thinking. Yes, there is a limited supply of manufacturing and packaging capacity for server-class processors based on the most advanced semiconductor nodes. It’s in the less obvious ways, such as the availability of …

With Vista, TACC Now Has Three Paths To Its Future Horizon Supercomputer

The national supercomputing centers in the United States, Europe, and China are not only rich enough to build very powerful machines, but they are rich enough, thanks to their national governments, to underwrite and support multiple and somewhat incompatible architectures to hedge their bets and mitigate their risk. In the …

Intel’s Chips No Longer Pay More Than Their Fair Share Of Foundry Costs

The biggest benefit that is coming from the separation of the Intel chip design and marketing business from its foundry operations is that Intel’s chip product groups no longer have to shoulder the totality of the immense costs of its manufacturing operations. The biggest downside is that they these chip …

Be the first to comment