The supply chain is holding back the server business, and not just in the way you are thinking. Yes, there is a limited supply of manufacturing and packaging capacity for server-class processors based on the most advanced semiconductor nodes. It’s in the less obvious ways, such as the availability of power supplies and various kinds of controllers and peripherals that the OEMs and the ODMs need when they make a server.

“Trust me, we would be shipping a lot more units if we were not constrained by the supply chain of these other components in the industry,” explained Pat Gelsinger, the chief executive officer who was brought into Intel in January to save it from itself and get it back to what it once was. “Our customers, both cloud customers and OEMs, have very strong backlogs that they are pressing us aggressively to satisfy. But we are really limited by these ‘match sets’ as we call it in the industry.”

Another constraining factor for Intel’s Data Center Group, which still exists in the company’s financials despite a reorganization that happened in June, was curtailed shipments of server chips and other datacenter components to China. Gelsinger said that there have recently been changes to regulations in China — what he called a “new regulatory environment” that actually affected shipments of the “Ice Lake” Xeon SPs into the Middle Kingdom for supercomputers and cloud builders, and, we think, will also curtail those for the future “Sapphire Rapids” Xeon SP follow-ons that are slated for production starting in Q1 2022 and volumes and announcement in Q2 2022, according to Gelsinger, who added that Intel has “uniquely high market share in the Chinese cloud market.”

We suspect that is changing, and for a lot of reasons, including incursions by AMD and Ampere Computing and the desire among the hyperscalers and cloud builders to control their own fate, such as Alibaba’s Yitian 710 homegrown, custom Arm server chip, which we talked about ahead of its launch last week and which we will drill down into provided we can get the feeds and speeds. And so we suspect that Intel has more to worry about than a change in regulations in China, including the ever-expanding Entity List where certain kinds of chippery are blocked for sale by the US Department of Commerce’s Bureau of Industry and Security.

In the quarter ended in September, which disappointed Wall Street more for its forecast than for the actual numbers in the quarter, but both are softer than expected, Intel raked in $19.2 billion in revenues, up 4.7 percent, and thanks to a $1.71 billion gain on equity investments, was able to post a net income of $6.82 billion, up 59.7 percent.

In the Data Center Group, Gelsinger was happy to report that between April and September the company shipped over 1 million Ice Lake Xeon SPs, and the ramp was progressing such that another 1 million units would ship in the fourth quarter, which is a factor of 2X more units in a three-month period. What we found interesting, however, is that the mix for Ice Lake Xeon SP sales was more for the HCC variants — those with 8 to 28 cores — rather than for the XCC variants, which scale from 16 to 40 cores. (There apparently is no LCC variant with the Ice Lake chips, as there has been for many of the past generations of Xeon and Xeon SP processors.) Another mix shift that drove down chip average selling prices in Data Center Group (and therefore revenues) was the shift from CPUs to SoCs, according to George Davis, Intel’s chief financial officer, who announced he was retiring on the call with Wall Street analysts.

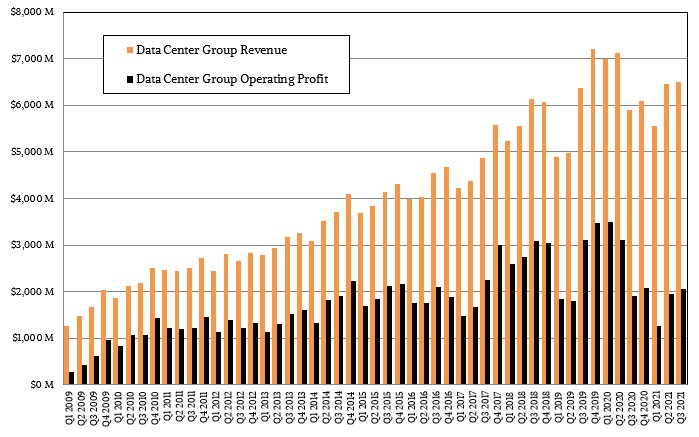

Sales for Data Center Group were just a tad bit under $6.5 billion, up a flat 10 percent, and operating income rose by a slightly less impressive 8.1 percent to $2.06 billion. Operating income was 31.7 percent of revenue, which is a hell of a lot better than the 22.9 percent it was in Q1 2021 and a tiny bit better than the 30.1 percent in Q2 2021, but we are a long way from the close to 50 percent operating income that Data Center Group had when there was no competition in the market in the glory days of late 2009 through early 2020.

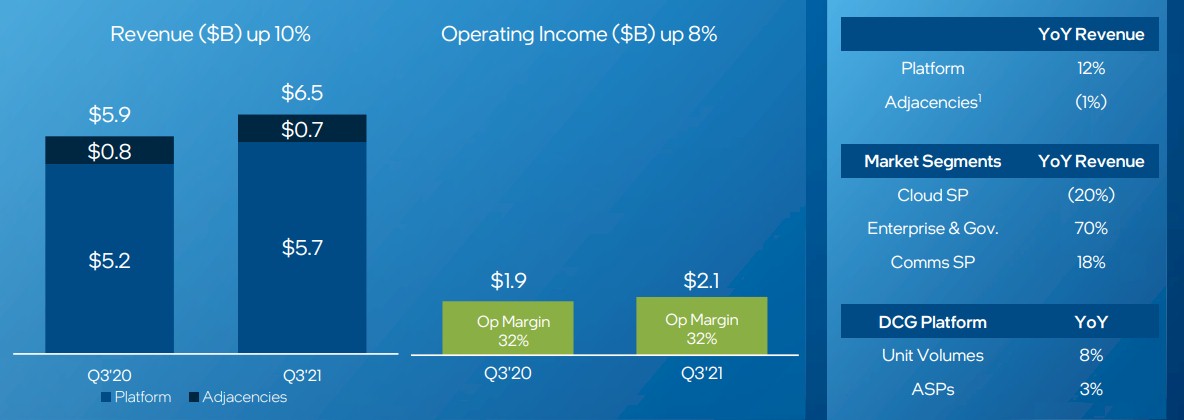

The hyperscalers and cloud builders — what Intel calls cloud service providers — spent 20 percent less on Intel chips and other components in the third quarter, and with them comprising such a big part of Intel’s sales, when they slow their spending, it really has a dramatic impact on Intel’s overall sales. And thus, even though spending by enterprise and government customers was up by a stunning 70 percent — against a weak number a year ago, mind you — and even though communications service providers (telcos and such) rose by 18 percent, overall Data Center Group sales were more muted than they might have otherwise been. Intel didn’t say how much the impact was from the regulatory changes in China, but we believe it walked the fine line between “significant” and “material” — but that is just a gut hunch.

As usual, the IoT Group + Mobileye and the Programmable Solutions Group (formerly known as Altera) that peddles FPGAs could not fill in the gap, but IoT Group + Mobileye was at least a significant contributor to top line growth and really helped operating margins, as you can see:

We have been tracking the Altera/PSG business separately for a while, and frankly, we expected for this business to grow a lot faster than it has been doing. In the third quarter ended in September, PSG posted sales of $478 million, up 16.3 percent, which is more than three times as good as Intel’s overall growth, and operating income increased by 90 percent to $76 million. If you allocate net income proportional to revenue and adjust for overhead, PSG might account for something like $100 million in net income, which would be 20.9 percent of revenues, which is the ratio of net income to revenues that Altera was posting back in 2013 and 2014, just when Intel started sniffing around to acquire Altera and when it looked like FPGAs would be more popular than they have turned out to be.

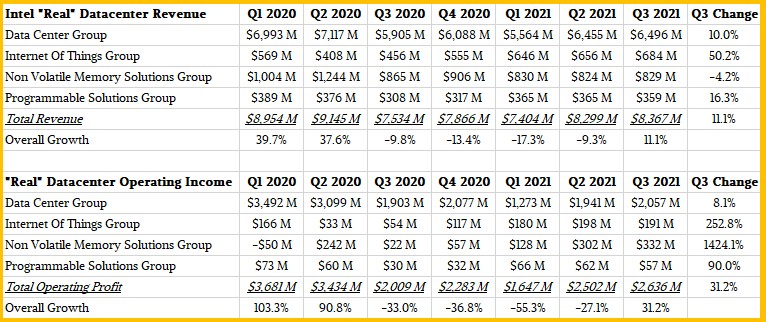

Every quarter, we try to reckon what Intel’s “real” datacenter business looks like, including portions of its various groups that actually do sell products and services into the datacenter with the posted Data Center Group revenues. Here is what our model looks like for all of 2020 and the first three quarters of 2021:

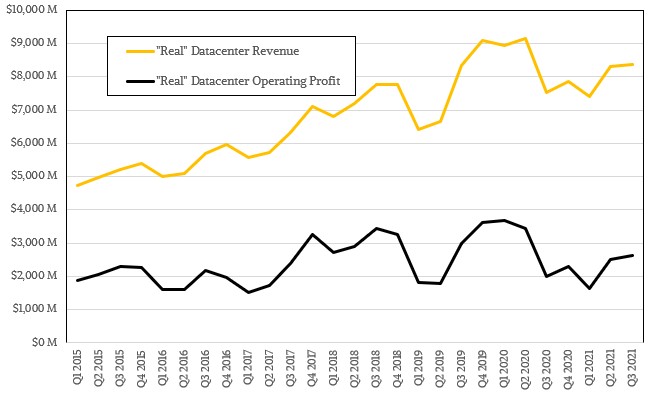

And for those of you who like your data presented visually so you can see trends better, here is a plot that goes back to 2015, when we first were able to build this model:

After our allocations, which we admit are based on educated guesses, we reckon that revenues for the “real” datacenter business at Intel were actually up by 11.1 percent, to $8.37 billion, and operating profits rose by 31.2 percent to $2.67 billion, which works out to 31.2 percent of revenues.

Looking ahead, the top brass at Intel say they expect to break through $74 billion in sales in 2022, with a compound annual growth rate of 10 percent to 12 percent over the next four to five years, and gross margins hitting 51 percent to 53 percent in the next two to three years. Capital spending is set at between $25 billion to $28 billion in 2022 — that is about one and a half modern 7-nanometer fabs, give or take, so don’t be impressed, be horrified that this is all that money gets you.

Maybe we are just getting cynical, but we think Intel is going to have a lot tougher sledding than this. But Gelsinger is not just a technologist and a manager, he is an optimist. And he was pleased to tell Wall Street that the next five nodes of semiconductor manufacturing — 10 nanometer SuperFIN is already out and is what the company is now calling Intel 7, Intel 4 (what we used to call 7 nanometer), Intel 3 (what we used to call 5 nanometer), Intel 20A, and Intel 18A — which are all slated to come out in the next four years, are on or ahead of schedule.

“Relatively speaking, we are closing the gap on the industry, probably even more rapidly than I would have expected just a quarter ago,” Gelsinger said. “And as a result of that, these investments will be producing superior products with superior pricing and margins more rapidly, than we would have forecast even a quarter ago.”

Taiwan Semiconductor Manufacturing Co is reportedly having issues with its 3-nanometer process, so maybe it will be Intel’s turn to be in the driver’s seat for a while. Stranger things have happened. Like Intel almost forgetting that it needed to be at the forefront of chip manufacturing and then also design excellent chips. The former was always more important than the latter when it came to Intel processors, and Intel might have just remembered in time to not lose its server business to the competition that has filled the vacuum it left. Still, look at all those profits from 2009 through 2020 … It’s an object lesson in short term gain over long-term gain. Now, with Gelsinger at the helm, Intel is back to playing the long game. At least it is not the wrong game.

Billions in profit, I don’t see any need to be concerned, they can keep doing what they do, they have nothing to worry about.

On channel data on Intel q3 financial reconciliation and CEO Gelsinger Ice Lake 1 million unit shipment statement, I have Cascade Lake R still out shipping Ice by 12 to 1. Unless of course Sapphire Rapids is shipping in risk volumes would not be the first time Intel shipped next generation for revenue before the products introduction.

Xeon 1K price on channel across grade SKUs percent inventory weight;

Xeon Ice Lake q2 1K AWP = $2392.92

Xeon Ice Lake q3 1K AWP = $2290.10 < 4.29%

Xeon Cascade Lake R q2 1K AWP = $1723.55

Xeon Cascade Lake R q3 1K AWP = $1789.93 + 3.85%

Xeon Ice and CLr combined q2 1K AWP = $1723.55

Xeon Ice and CLr combined q3 1K AWP = $1891.47 + 9.74%

Intel Xeon high volume discount off 1K through q3 is 77%. Xeon can be procured in a cross generation full line sales package for $518.75 each. In a 100,000 unit sales package 767 would be Ice. Across CLr and Ice core grades LCC to XCC, 251 components would be Ice 32 to 40 Core. I suspect Cascade Lake diminished from Intel inventories by next quarter and Ice as an intermediate technology tied to Sapphire Rapids procurement contracts. Take Cascade Lake R to help off it into the broker market, except Ice tied in sales package for Sapphire Rapids access and allocation.

The buy in price is going up. Lock yourself in?

Mike Bruzzone, Camp Marketing

“Trust me, we would be shipping a lot more units if we were not constrained by the supply chain of these other components in the industry,” explained Pat Gelsinger…

I’m pretty certain that holds true for AMD as well.