It is beginning to look like chip maker Intel hit the bottom in its products and foundry businesses in the second quarter of this year and that revenues are slowly – we won’t go so far as to say surely – improving. But now the restructuring charges and cost cutting is going to start to bite and the bottom line will look a little ugly for a while.

Then, Intel will run out of excuses, and hopefully in time for its 18A manufacturing process to catch a little fire among others designing chips for myriad purposes and for 18A processes to be brought to bear on Intel homegrown client and server products. In other words, 2025 should be a hell of a lot better than the misery that 2023 and 2024 was.

“Operationally, Q3 results exceeded our expectations as we achieved key milestones across Intel Foundry and Intel Products,” explained Intel chief executive officer Pat Gelsinger on a call with Wall Street analysts going over the numbers. “Underlying trends in the business are improving at a measured pace and our outlook for Q4 is modestly above current consensus. Overall, our stepped up focus on efficiency and execution across business is having a positive impact. We have a lot more ahead and we are acting with urgency to deliver on our priorities. We need to fight for every inch and execute better than ever before, and our teams are embracing this mindset as we build a leaner, more profitable Intel.”

In the quarter, Intel had revenues of $13.28 billion, down 6.2 percent year on year, and posted an operating loss across all of its groups and units of $4.6 billion, a stark contrast to the $8 million loss Intel had in the year ago period. And adding in another $5.62 billion in restructuring and other charges – a lot of this relating to laying off more than 15 percent of the Intel workforce ($2.2 billion), goodwill impairments for the Mobileye unit ($2.6 billion), and also writing down investments in gear used to make chips with the Intel 7 process ($3 billion), which etches at a 10 nanometer-ish geometries and which cannot be moved forward to support extreme ultraviolet lithography at smaller transistor geometries. Oddly, Intel also booked a $7.9 billion provision for taxes, pushing the company to a mind-numbing net loss of just a tad under $17 billion.

Ouch.

Operating income, by the way, was impacted by a $300 million write down of accelerator inventory – which we presume was for Gaudi 2 and Gaudi 3 devices, but also possibly for some “Ponte Vecchio” Max Series GPUs that Intel might have had laying around, “due to reduced revenue expectations.”

Gelsinger said on the call that “overall uptake of Gaudi has been slower than we anticipated as adoption rates were impacted by the product transition from Gaudi 2 to Gaudi 3 and software ease of use.” And to that end, Intel’s projections of bringing in $500 million for Gaudi accelerator sales (mostly for Gaudi 3 devices we presume) in 2024 will not be realized. With a $300 million writeoff, that seems to imply that Intel is only selling $200 million in Gaudi 3 gear. That implies that of the 32,000 Gaudi 3 accelerators that Intel thought it could sell in 2024, only 12,800 found homes. If you want Gaudi 3 accelerators on the cheap, Intel has 19,200 of them sitting around. That’s a little bit more than 40 exaflops at BF16 floating point precision, which would be a not too shabby cluster by any standard. However, you are going to have a lot of work to do with the software stack, and the Intel people who might help you might no longer work there.

So far, Intel seems to be sticking to its plan to evolve the Gaudi line into the “Falcon Shores” hybrid of its Ponte Vecchio/Rialto Bridge GPU and Gaudi 3 designs and iterated forward one or two notches. It would be a very bad thing if Intel gave up on AI acceleration, even if it does cost money in the short term. The AI server market is not going away, and as we have shown in many forecasts, it will eventually represent half or more of AI server spending. Intel cannot afford to leave all of that market on the table, even if it has to become a world class foundry again.

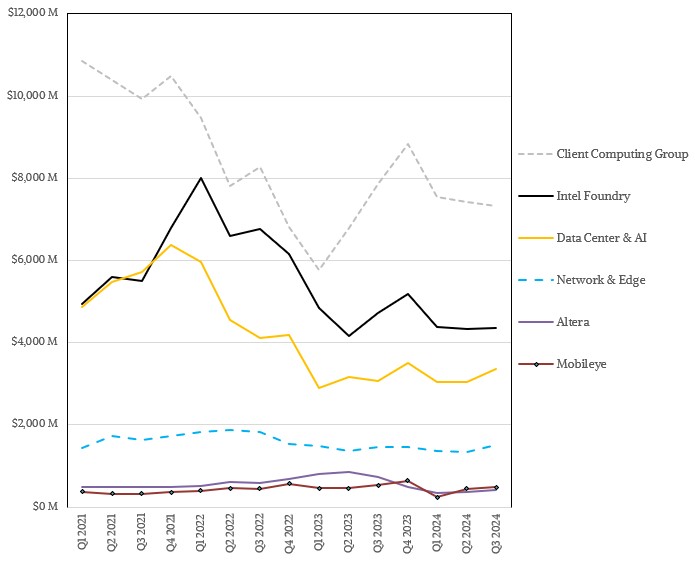

By the end of the decade, Intel wants that foundry to be driving $15 billion a year in external revenues, which is a little bit less that the Intel Products group pays Intel Foundry for etching and packaging today. Hopefully, when Intel Foundry is driving in excess of $30 billion a year in revenues – and possibly more – it will actually be a profitable business. Which it most certainly is not today, as you can see in the table below:

The main thing you need to be happy about in this table is that the Client Computing Group, which makes CPUs and GPUs for PCs, is holding its ground and represents the bulk of the free cash that Intel is generating. This is the fuel that will help Intel push through this terrible time.

If Intel had started on a genuine datacenter GPU business back in 2012, when it was very obvious that it would need one, and delivered on its potential, the Data Center & AI group would not be looking so rough right now. As it is, DCAI brought in $3.35 billion in sales, up 8.9 percent year on year and up 10 percent sequentially thanks to the ramp of the Xeon 6 server CPU lineup. With only $347 million in operating profit, which was reduced presumably by that $300 million writedown presumably related to the Gaudi accelerators not selling like hotcakes, operating income was down 11.3 percent but up 25.7 percent sequentially.

We are a long way from the close to 50 percent operating margins that the old Intel Data Center Group used to rake in.

Still, as this chart shows using the new groups that Intel set up in 2022 to describe itself to Wall Street (and that we extended backwards into 2021), things have stopped getting worse, more or less, and that is something. This is the only reason we can think of that Intel’s stock should have gone up in aftermarket trading in the wake of the report to Wall Street.

As you are well aware, we like to show the trend lines of Intel’s “real” datacenter business over time, which has become a lot simpler with the shutting down or selling off of its various network switch businesses (Barefoot Networks and Omni-Path) and the spinout of its flash storage business.

As best as we can figure from our model, Intel’s real datacenter business is 5/9ths are large as it used to be and only nominally profitable. Provided there are not any surprise writeoffs and charges going forward, this datacenter business, which includes all of DCAI plus slices of Altera and NEX at this point and is a lot less complex, should grow as Intel’s 18A processes are used for future “Diamond Rapids” P-core and “Clearwater Forest” E-core Xeon 7 processors. Gelsinger said that Clearwater Forest has powered on, and Diamond Rapids is shortly going into the fab for etching.

NSF Puts $10 Million Into Composable Supercomputer

If they are doing their jobs right, the high performance computing centers around the world in academic and government institutions are supposed to be on the cutting edge of any new technology that boosts the performance of simulation, modeling, analytics, and artificial intelligence. Not the bleeding edge, where the hyperscalers …

The “Hopper” GPU Compute Ramp Finally Starts

You can’t be certain about a lot of things in the world these days, but one thing you can count on is the voracious appetite for parallel compute, high bandwidth memory, and high bandwidth networking for AI training workloads. And that is why Nvidia can afford to milk its prior …

The Edge Propels HPE While Datacenter Taps The Brakes

Customers of Hewlett Packard Enterprise have one foot on the gas and one foot on the brakes at the same time that the company is transitioning from selling gear outright to customers to selling them subscriptions that spread the cost – and therefore HPE’s recognized revenues – out over time. …

Great to see that “things have stopped getting worse, more or less” at Intel! It’s a tough rodeo to be in and if they can stem some of the bruising and limb breaking then so much the better.

Now that they have the HPCG bullriding suplex champion Granite Rapids in the field (and Diamond as a presumably straightforward PCIe6.0/CXL 3.0 successor), it’s high noon indeed for a focus on Falcon Shores, and related media PR, tech info, details, specs, size of saddlebags, etc … The last plot in Wednesday’s AMD Instinct story says it all: a 30.4x revenue increase in 1 year! That’s the kind of silver dollar that could really help pay for foundry bringup at advanced nodes IMHO.

Intel is in a bad place compared to years past. However, it still sells about half the datacenter CPUs and client CPUs on the planet. Even in this diminished form, it still has staggeringly ubiquitous products, some of which sell for more than ten thousand dollars apiece. It’s kind of astonishing they can’t make money.

“Nvidia to Replace Intel in Dow Jones Industrial Average” per WSJ 2024 Nov 1st…Ouch!

It’s probably okay (in my mind, not unusual) as the DJIA is meant to depict overall market performance in the US based on just 30 stocks, and so they add and remove stocks from companies in similar activity categories every year (to keep just 30). Replacing Intel (underperforming) with Nvidia (overperforming) is going to give DJIA a bit of an “optimistic boost” though, that may not make it a more accurate representation of real industrial activity (imho).

What Intel is doing with (essentially) “reshoring” of advanced chip production fab capacity is very expensive, but was deemed strategically essential in view of the supply chain disruptions that arose from COVID. I expect that, through this investment, short-term profit loss will be replaced by steady gains in the medium and long-term, once fabs are operating at capacity (it just takes a bit longer than what some financial analysts are used to).

Agreed. We need a second, good foundry. This is dangerous. Of course, having a second good foundry is ALSO dangerous.

Which begs the question: Is the world always dangerous? HA! It seems to be built into the fabric of spacetime. . . . probably on purpose.

This is the problem, right? TSMC is essentially a monopoly at this point. It’s also in a politically dangerous location, but even without that it’s a monopoly. If Intel fails, does the department of justice try to split up tsmc? It’s not a US corporation. How do antitrust laws work when none of the remaining vendors are US based?

Good questions. I think antitrust bodies have the power to prevent mergers and acquisitions, but I don’t think any government has any power to do any busting up except inside its sovereign domain. I am counting Europe as a domain in this regard, given the EU.

IBM also had a 7nm fabrication problem when Global Foundries spent their money on something else and unexpectedly abandoned advanced process nodes. For that Power 10 ended up years late manufactured by Samsung. At least Intel did not turn into a manufacturer of boutique hardware designed only for running legacy code.

While Intel is trying to regain market share, my opinion is they sold off too many innovative assets and discontinued others. I think recovery will be difficult because the biggest problem is not bad CPUs but disruption by the AI industry’s need for faster storage, faster networking and faster GPU accelerators.

Fron Camp Marketing Intel q3 channel supply data on INTC financial reconciliation supplied total on a net basis,

Xeon Sierra Forrest and Granite Rapids = 1,119,000 units

NEX = 11,151,377 the dice bank is filled

Gaudi 3 = 32,000 courtesy of TPM

Core Arrow desktop = 4,739,608 and another 14,327,127 q4 credit

Core Raptor desktop warranty = 20,301,167

Core Meteor and Raptor embedded = 5,031,377

Core Lunar mobile = 31,206,224 good until Panther

Total = 78,653,881 units

Summary

Intel Stated CPU Division Revenue = $12.1 B / 78,653,881 units = $153.84

Intel Stated CPU Operating Cost = $8.8 B / units = $111.88

Intel States CPU Operating Income $6 B / units = $76.28 that is Price ‘A1’

CPU Divisions $12,100,000,000 revenue / units = $153.845 per unit

CPU described as Operating Cost = $111.88 per unit

CPU Gross is actually fixed (marginal) cost of production = $41.96

CPU R&D contribution = $51.48

CPU MGA contribution = $17.48

CPU NET revenue less costs = $1 same as q4 2023

CPU PE&C contribution = $165.67

CPU Restructure contribution = $71.47

CPU Tax accrual contribution = $100

CPU NET LOSS = ($337) per unit that is $5,622,000,000 restructuring

Fixed cost of production $41.96

R&D as fixed cost $51.48

MG&A as variable cost = $17.58

Total $111.02

Less restructuring $71.47 is Price ‘A2’

Less fixed cost of Production $41.96

Equals variable cost $39.54

The full report including q3 x86 production and component channel share is here top of comment string here,

https://seekingalpha.com/article/4731858-intel-corporation-intc-q3-2024-earnings-call-transcript

Mike Bruzzone, Camp Marketing