There is wracking up the money, and racking up the servers – and Supermicro, which is sometimes an OEM and sometimes an ODM as well as a motherboard and component supplier to those who want to be either, is doing both here at the beginning of its fiscal 2024 year. Things are going so good that the company is raising its revenue guidance and now expects to book somewhere between $10 billion and $11 billion in sales for the current fiscal year.

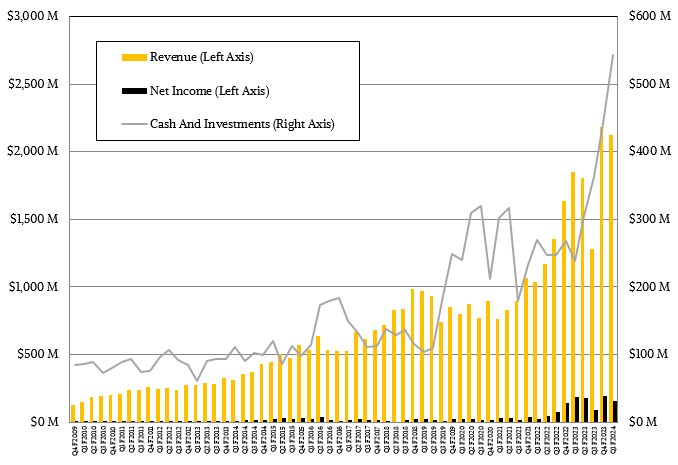

In the first quarter of fiscal 2024, which ended in September, Supermicro posted revenues of $2.12 billion, up 14.4 percent year on year and only down 3 percent sequentially.

Net income fell by 14.9 percent to $157 million, however, as research and development expenses exploded by 49.6 percent to $111 million. Sales, market, and general costs were also up, which is what you would expect as Supermicro grows to meet what it anticipates will be much higher demand growth in the coming years as it doubles revenues again to an annual run rate of $20 billion.

Supermicro is playing the long game, obviously, and generally speaking Wall Street understands that and despite a 25.4 percent decline relative to the high set in August, it still has a market capitalization of $13.5 billion as we go to press. Which makes Supermicro too big to be acquired and gives the company the financial means to do acquisitions if it thinks it needs to do. The company had $543 million in cash in the bank as it exited fiscal Q1, more than double it had a year ago.

So far, Supermicro seems inclined to build out its own engineering and manufacturing capacity and stick to its strategy of leveraging its supply chain and engineering smarts to outgrow the server and storage industries.

Supermicro is shipping more than 4,000 racks of gear per month in its rack-scale systems business and according to company founder and chief executive officer Charles Liang, it will not be long before it is shipping 5,000 racks per month. (We think that Meta Platforms is a big customer of Supermicro’s now, but this is something that neither Supermicro nor Meta Platforms has ever confirmed.)

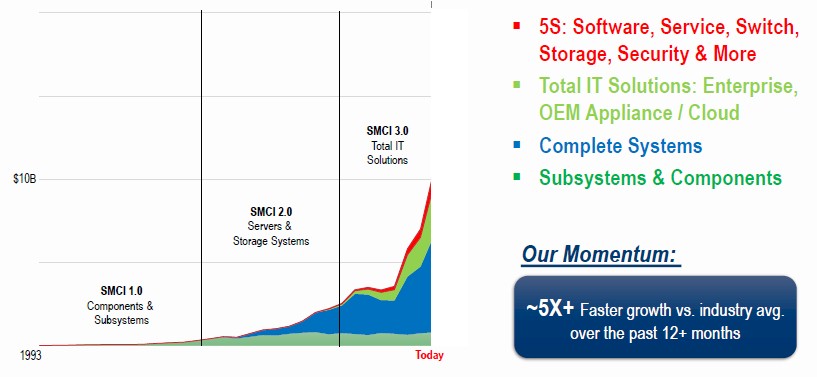

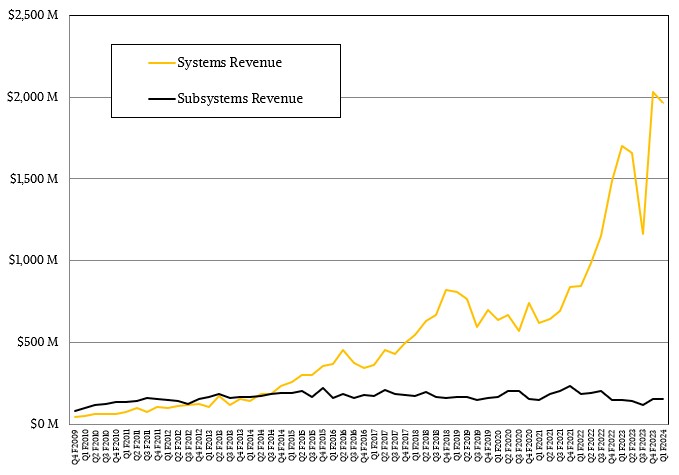

By our math, looking at the chart above and assuming that all almost of that growth to reach a $20 billion annualized run rate comes from sales of “complete systems” to hyperscalers, cloud builders, and Tier 2 service providers, then the rack-scale system business will have to triple for Supermicro to get there.

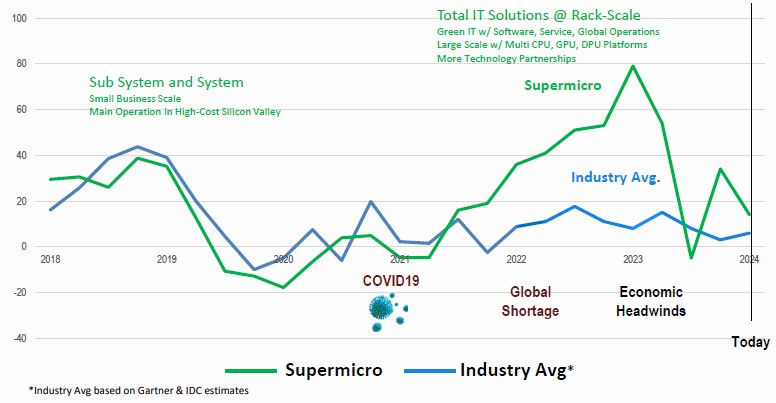

If you plot the curve of the blue area in the chart out above, it sure looks like the company can get there in a few years. It is easy, of course, to draw a line up and to the right. But it is another thing entirely to build the business that supports that line. For Supermicro to accomplish that $20 billion sales goal, a lot depends on the global economy and, really, spending by big companies in the United States. That is what is driving all of this growth in recent years:

Liang said on a call with Wall Street analysts going over the numbers that the factories it operates in the United States and Taiwan are only running at 60 percent utilization, and that the new factory in Malaysia will be coming online soon. Because manufacturing costs are lower in Malaysia, this will have an immediate effect on profits, but more importantly, as factory utilization increases across all of its facilities (including the other factory in the Netherlands that has been operating for European customers for many years) this will be the real driver of profits as costs per unit go down.

Over the course of our financial model for Supermicro, which goes all the way back to fiscal 2009 during the Great Recession, sales of subsystems – motherboards, add-in cards, enclosures, and so on – have averaged $165 million per quarter, and the $153 million sold during the first quarter of fiscal 2024 were in the same ballpark. This business has been trending slightly downwards for the past several years, but it is interesting because Supermicro has to create all of these components for its systems and rack-scale businesses anyway and it is a gauge of sorts for how the Tier 2 and Tier 3 OEMs are doing in the market since Supermicro is a big supplier to such companies.

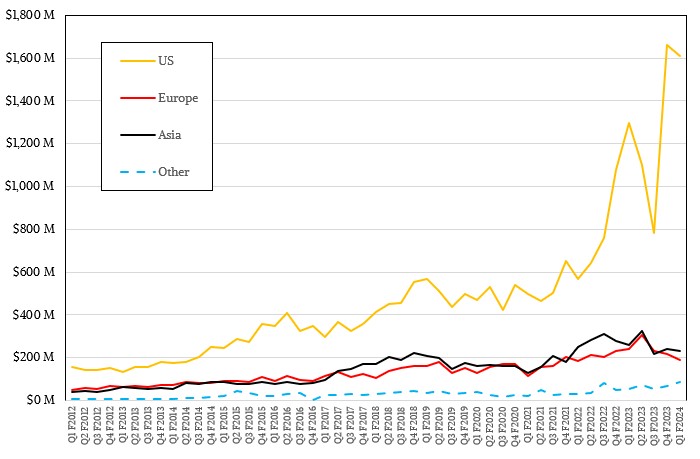

Obviously system sales – and particularly full configured racks – are driving Supermicro’s business, and overlaying the geography and segment and customer charts, you can infer that large companies in the United States are big drives of the growth in recent years, but the underlying systems and subsystems businesses are humming along. It would be good if Supermicro just broke apart the systems and rack-scale segments so we could see their individual revenue streams directly.

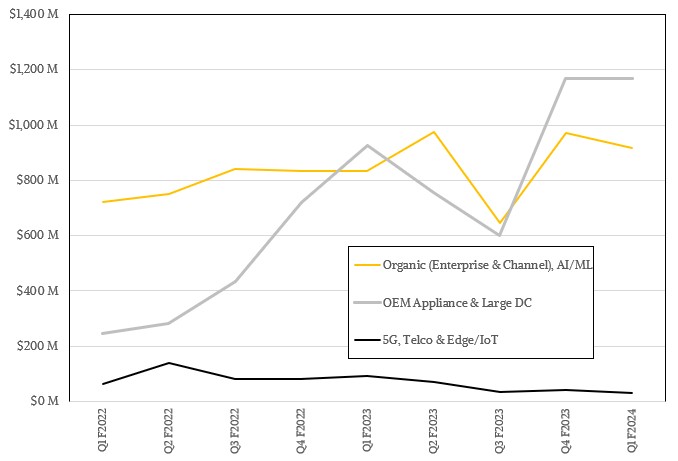

The company does provide some hints. David Weigand, chief financial officer at Supermicro, said on the call that rack-scale and AI system sales accounted for 53 percent of revenues, which is $1.12 billion. Sales to large datacenter customers and OEM appliances to other vendors (of which we also think Nvidia is one) accounted for $1.17 billion, up 26.3 percent. (These are separate slicings of the Supermicro pie, not separate slices within the same pie chart, so don’t think you can add those numbers to get the pie.) In the second pie, where you can add up the slices to get a full circle of revenues, enterprise customers and channel sellers plus AI/ML iron accounted for $917 million in revenues, up 10 percent year on year. Various edge platforms accounted for $31 million in sales, down 66.5 percent. Edge smedge. This may be an important business for Supermicro and others over the long haul, but it is not very exciting right now by comparison to the rest of the Supermicro business.

Last data point we can cull from what Supermicro said: One existing cloud service provider/large datacenter customer drove 25 percent of revenues, or $530 million in sales, and we have nothing to compare to in the year ago quarter to give you a growth rate. We think this is very likely Meta Platforms.

What we can also tell you is that no matter how you add and subtract these numbers, you can’t get a good number for Supermicro’s total AI/ML system revenues. But Weigand seemed to say during the call that AI/ML drove more than half of sales in Q1 F2024 and will do the same in Q2 F2024.

Looking ahead, the loosening up of GPU supplies from Nvidia now that export controls are limiting even more sales into China will be helping companies like Supermicro do more deals and drive more sales. Liang said that the forecast of $2.7 billion to $2.9 billion in revenues for the December quarter (it’s second quarter of fiscal 2024) “should be a very conservative number” and that so is the annual guidance of $10 billion to $11 billion for fiscal 2024.

The Only Thing Worse Than Selling AI Servers Is Not Selling Them

For as long as we can remember, the high performance computing business was one where it has been difficult for the manufacturers that build systems to make a buck. With the advent of GenAI and booming sales of AI servers to run training and often inference workloads, none of this …

System Spending Forecast Goes Through The Datacenter Roof

The third quarter earnings season starts this week for the hyperscaler and cloud giants, and it is fortuitous that the economists and IT analysts at Gartner have updated their forecast for IT spending for 2024 and added an jaw-dropping forecast for 2025 and hinted at a brave new world of …

The Slow But Tectonic Shifts In Datacenter Infrastructure

One of the more interesting trends in infrastructure that we try to get a handle on every once in a while is how much of the server and storage capacity is being deployed in bare metal, standalone fashion and how much is being sold to run utility style, cloud environments. …

No smudge or fudge, no smidge of hodgepodge, a perfect porridge for Goldilocks’ lodge; grrrrreat numbers!

And who could forget the ’21 Osaka SQUID [ https://www.supermicro.com/en/pressreleases/supermicro-delivers-broadest-portfolio-application-optimized-systems-based-3rd-gen ]!? Happy sailing for HPC and AI cephalopods … (esp. in marinara sauce) … to chestfuls of crispy chocolate doublons! 8^b