Accounting is something of an art, and companies always save some accounting tricks – perfectly legitimate items that meet the discerning eye of financial standards – to goose their numbers when they really need it. When they really need to tell a turnaround story. And so it is with Intel in the second quarter of 2023.

Yes, the PC market is less horrible than it was and yes, Intel is executing to its server roadmap and is on track to compete with rival Taiwan Semiconductor Manufacturing Co within two years in terms of process technology. We said “compete with,” and we said it on purpose. Intel keeps saying it can beat TSMC on chip manufacturing with its 18A process by 2025, but TSMC keeps saying not a chance, its 2N process will whip anyone out there. (There’s only two other companies out there, Samsung and Intel.) History – backwards looking time – suggests TSMC is right, but only forward looking time (from our current point of view) lived in the moment then (in the future that will become present), will tell who is right.

As we have said before, the only perfectly accurate way to predict the future is to live it. Which is what makes life exciting.

That Intel is not doing as badly as either itself or Wall Street expected is, of course, a good thing. The IT sector needs Intel to compete, and compete well, to help drive the cost of compute in the datacenter downwards and the performance of those compute engines up. AMD has been doing a pretty good job in Intel’s stead in recent years, which is what we expect AMD’s numbers to show next week. But even with this explosion in AI spending, the underlying server market is sluggish, and even the cloud builders and hyperscalers are taking it a bit easy here in the first half of the year.

In the quarter ended in June, Intel’s posted $12.95 billion in sales, off 15.5 percent, but even after some pretty substantial cost-cutting, the company still posted an operating loss of $1.02 billion, an increase of 45.1 percent compared to the 700 million operating loss in the year-ago period. Intel had a $224 million gain from interest, which help cushion the blow a little, and posted a $2.29 billion benefit from income taxes, which switched it from what would have been a pretty big net loss to a net gain of $1.48 billion.

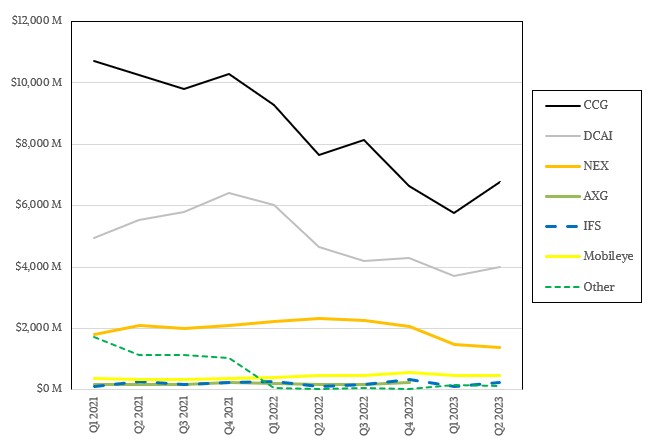

What matters most of course is how the underlying businesses are doing, and when it comes to Intel what we really care about are the Data Center & AI group and the Network and Edge Group.. We like when the other parts of Intel are growing and making money, of course, because that makes Intel more resilient. But what we really always care about is trying to ascertain how its “real” datacenter business is performing financially.

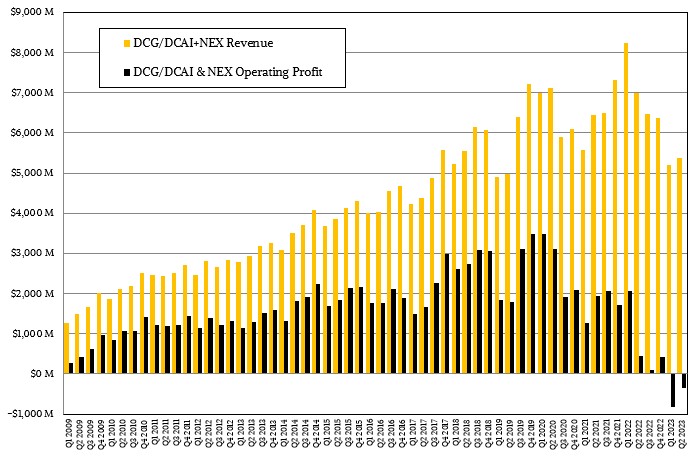

Intel merged portions of the former Accelerated Computing and Graphics group (AXG) into its DCAI and Client Computing Group (CCG) starting in the first quarter and is recasting these figures as the quarters roll on – it has not put out a summary table that goes back into the prior year as yet. So the comparisons in the chart above are a little wonky. We will fix it by January next year when the last change rolls through for Q4 2023. The next effect is that the DCAI and CCG groups have more revenue but also losses they didn’t have before – and the losses are bigger than the revenue gains.

As currently reported, The DCAI group had sales of just over $4 billion, down 14.7 billion, and this key historical profit engine for Intel had an operating loss of $161 million, a little more than double the loss from the year-ago period. That loss was driven by higher unit costs, which in turn were driven by lower factory utilization at the Intel fabs and a product mix towards more capacious (and more expensive to manufacture) compute engines.

“While we performed ahead of expectations, the Q2 consumption TAM for servers remained soft on persistent weakness across all segments, but particularly in the enterprise and rest of world where the recovery is taking longer than expected across the entire industry,” Pat Gelsinger, Intel’s chief executive officer, said on the call with Wall Street analysts. “We see the server CPU inventory digestion persisting in the second half, additionally, impacted by the near-term wallet share focus on AI accelerators rather than general purpose compute in the cloud. We expect Q3 server CPUs to modestly decline sequentially before recovering in Q4. Longer term, we see AI as TAM expansive to server CPUs and more importantly, we see our accelerated product portfolio is well positioned to gain share in 2024 and beyond.”

Gelsinger said that its datacenter AI pipeline is now over $1 billion, including Flex and Max Series GPU accelerators and Gaudi matrix math engines, and that the Gaudi chips are driving the lion’s share of this opportunity. That is not a surprise, given that the Max Series GPUs, formerly known as “Ponte Vecchio” and used in the “Aurora A21” supercomputer at Argonne National Laboratory, are very expensive to make and are being consumed almost entirely by that supercomputer at the moment. As we have said, Gaudi is going to get some supply wins as are every other kind of engine that can do AI training math because of the high cost and dearth of Nvidia GPU engines. We think AMD’s Instinct MI300 series GPUs are set to benefit more than Intel’s Max Series GPUs and Gaudi2 and Gaudi3 accelerators, but we also think that Intel could sell all of the AI compute engines it could make. The question is: Can it or will it make more?

More broadly, Gelsinger said that server buying by hyperscalers, cloud builders, and enterprises are expected to all be softer in Q3, and the recovery of the economy in China is also taking longer, so the server recession is going to go into its third consecutive quarter. AI server sales is helping, particularly with so many designs using Intel’s “Sapphire Rapids” Xeon SPs. But plenty of designs are using AMD “Milan” Epyc 7003 CPUs, and we expect to see “Genoa” Epyc 9004 series CPUs going into more AI systems as soon as volumes become more readily available.

Gelsinger said that Intel was getting ready to ship its 1 millionth Sapphire Rapids CPU, which was launched officially in January but which we think has been shipping to cloud builders and hyperscalers since about this time last year.

The NEX group, which has exited the datacenter switching business Intel had invested very heavily in, still does network interface cards, DPUs, and customized gear for the edge and other embedded use cases (including the Xeon D processor), had a much tougher quarter.

Revenues were down 38.3 percent to $1.36 billion, and NEX shifted from a $294 million operating profit to a $187 million operating loss in the June quarter. Ouch. Intel said that there was not as much uptake on edge use cases as it had hoped and there was softness in demand among telcos and other service providers, too. The former Altera FPGA business, which was known as the Programmable Solutions Group before it was folded into NEX last year, had its third consecutive quarter of record results since it was acquired by Intel, and that helped prop up NEX sales and profits.

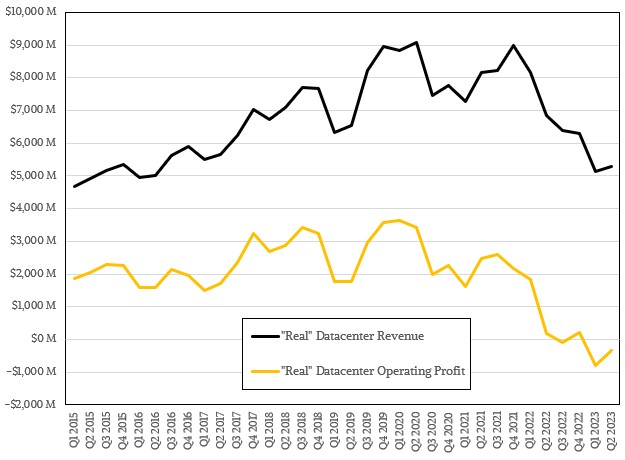

Intel dices and slices its datacenter business in a bunch of ways, and for the past eight years, we have been trying to suss out what Intel’s “real” datacenter business is. This gets trickier and tricker, but we think it is an illustration of a point as much as it is an attempt to quantify that which Intel should already do as part of its financial reporting.

Our best guess is that Intel’s real datacenter business – literally all of the stuff that ends up in datacenters and doing server-type work in the datacenter and now at the edge – came to $5.29 billion, down 22.9 percent year on year, and that operating income for this “real” datacenter business went from a $177 million gain a year ago to a $329 million loss this time around.

At its peak in 2019 and early 2020, using our old way of categorizing the datacenter, the datacenter business at Intel was pushing close to $9 billion a quarter in sales and somewhere around $3.5 billion in operating income. Just to have a sense of how far Intel has fallen here.

Wall Street might be celebrating that Intel beat expectations. But this is still pretty tough, and it looks like it will be tough slogging for a while yet. In fact, Intel may be slogging it out for the next five to ten years if its competitors stay focused and keep the heat on. They look inclined to do just that.

Enterprises Fill In The Hyperscaler Gap For Intel’s Datacenter Business

There is a new tick–tock at work at chip maker Intel, and one that overlays the normal metronome cadence of manufacturing process shrinks and architecture advancement. This one is the tick of shipping products to hyperscalers, cloud builders, and a select few HPC centers and the other is the tock …

HPC In 2020: Compute Engine Diversity Gets Real

The choice of processors available for high performance computing has been on growing for a number of years. There are no less than three major types of CPUs available for HPC duty, including X86, Arm, and Power architectures with more than a half dozen credible suppliers in total, along with …

Debunking Datacenter Compute Myths, Part One

There has always been a certain amount of fear, uncertainty, and doubt that IT vendors sow as they try to protect their positions in markets that they participate in. But there is also a lot of straight-up misunderstanding among those vendors as well as the people who work at the …

It’s good to see Intel coming out (albeit slowly) of its hubris-induced penalty box, as captain Gelsinger helms this highly-capable chip-shop back onto a proper course, on the sea of engineering-centered tech innovation!

FPGAs are cool (eg. Altera), and open source efforts such as Intel’s Open FPGA Stack (OFS), Open Programmable Acceleration Engine SDK (OPAE), and overall open.intel ecosystem, are great to widen software availability, and lower the barriers to entry for the development of much-needed talent pools in this field. I would encourage linking with yosys-mistral-nextpnr so that this FOSS suite works beyond Cyclone V (of the DE-10 based MiSTer FPGA arcade machine recreation project), in a way possibly similar to Intel’s valuable contributions to Linux & GNU software.

Someone could then probably implement the Berkeley SPUR CPU (RISC-IV, from 1987) in a contemporary FPGA! (it has tagged data typing and a windowed register file, perfect for running lexically-scoped dynamically-typed workloads, eg. VMs, JiTs, WebAssembled JavaScript, preemptively multitasked GUIs, etc…).

I quite like your CPU idea (and congrats to Intel for climbing out of the hubris sinkhole!). The Lattice ECP5 has 9-bit wide block RAM, perfect for 36-bit or 72-bit wide register files (32-bit data + 4-bit tag, or 64-bit + 8-bit tag). If only someone would make an ECP5 board with x18 or x36 external RAM (Radiona’s ULX3S uses x16-wide SDRAM, and so does Greg Davill’s OrangeCrab).

“Intel keeps saying it can beat TSMC on chip manufacturing with its 18A process by 2025 …”

Intel recently announced positive results on PowerVIA, which they claim gives them a 2 yr lead on TSM’s program.

From their q2 earnings call:

“On Intel 20A, our first node using both RibbonFET and PowerVia, Arrow Lake, a volume client product is currently running its first stepping in the fab.”

And TSMC said in its report to Wall Street: No way anyone will beat us!

“The former Altera FPGA business, which was known as the Programmable Solutions Group before it was folded into NEX last year, had its third consecutive quarter of record results…”

They also announced PRQ on 11 new FPGA products. Looks like they intend to expand on their FPGA success:

“We have now PRQed 11 of the 15 new products we expected to bring to market in calendar year ’23. “

Its insane that the results you objectively portray, could be viewed with such pink glasses by other reporters.

How can these results be construed as Intel climbing out of any sinkholes?

Investors should be very worried about low fab utilization. That could be deadly. I have little optimism for their hopes re contract fabbing.

A couple of long-departed crystal-ball spirits suggest that Intel stock (at $36) is undervalued and will return to $50 within a year or two-to-five (buy low, sell high, for 30% ROI — eg. google “Intel stock” and set range to Max). AMD, nVIDIA and APPLE are all currently at or near historical highs, and so a bit more of a gamble (needs careful reading of TNP to choose!) … 8^q

Intel Xeon SR/Ice/E Average Weighed Price q2 2023 = $1948.81 for gross $755.62 up 3.7% over q1 and q2 net before taxes (there don’t appear to be any) = $436.95 and with taxes $336.12 up minimally 16.8% per unit from q1. Intel sells approximately 9,163,317 units of Xeon not including NEX in q2. Subject product categories such as accelerators for whom the analyst has no channel supply data to establish volume and average weighed price assumes the DCG average.

Intel x10_ fabrication costs are coming down see Server Today at Slides 35 through 41. Ice cost per mm2 averaged $1.27 and Sapphire Rapids now averages $0.42 (MCC) to $$0.86 (XCC) and normalized $0.56 per mm2 on gross design production ‘marginal cost per unit’.

https://seekingalpha.com/instablog/5030701-mike-bruzzone/5509267-server-today

There are still cost : margin efficiency questions but the cost per mm2 of fabrication is improving and Ice volume pops + 78.6% q2 over q1 2023.

if pay walled here;

https://static.seekingalpha.com/uploads/sa_presentations/914/94914/original.pdf

Continuing Ice by UCC, XCC, HCC, LCC today and moving to AMD Genoa and Milan through the week.

Mike Bruzzone, Camp Marketing

Intel q2 channel on 10 K reconciliation;

DCG + AI average weighed $1K price across Sapphire Rapids, Ice, Rocket E = $1948.81 for gross $775.62 less R&D, MG&A, restructuring nets $436.95 and $101 less (per unit) with tax accrual accept Intel does not appear to register any tax expense q2. DCG gross is up 6.5% over q1. Net pretax up + 51.8% and if tax accrual + 16.8%.

Why the DCG loss I’m still looking into that. I can say Intel has not reached effective manufacturing albeit the cost situation has greatly improved with Ice per mm2 design production cost at $1.27 per mm2 through 2022 dropping at Sapphire Rapids to a normalized $0.56 average across XCC and MCC full line volume.

Intel q2 was probably stuck with selling some 2022 produced inventoried Ice at cost = price. You can tell on q1 in relation q2 channel volume Intel scrambled on Sapphire Rapids XCC and Ice volume price supports to pull up Sapphire Rapids MCC subject Xeon ‘full line’ q2 average price.

DCG + AI ships 9,163,317 units in the quarter and including NEX + 4,057,974 units = 13,221,291 approximately the same volume as q1 < 1.6%.

Camp Marketing believes Xeon D 27/17 subject NEX consecutive quarterly losses are written down at cost or went to the crusher? The product appears rejected.

Core line q2 recovered financially albeit q/q volume slightly down and more data is available at my Seeking Alpha comment line.

Mike Bruzzone, Camp Marketing