By all accounts, Big Blue had a pretty good quarter ending in June, with sales of its System z16 mainframes skyrocketing upwards as they do every couple of years at the beginning of a new cycle and sales of its high-end Power10 machines also getting some traction. If everything goes as planned, with the entry and midrange Power10 machines just launched and shipping at the end of this week, then the second half of 2022 should be a pretty good one for systems for IBM.

Nonetheless, Wall Street is giving IBM a bit of a drubbing as we go to press with this analysis of the company’s second quarter financial results, and that has more to do with the company shutting down its operations in Russia and the strength of the US dollar, which makes it more expensive to sell its products and services overseas. But a strong US dollar also makes every item sold overseas worth more dollars, which helps bolster revenues and profits. So there is that.

In the June quarter, IBM’s sales grew in a way that we have not seen in a long time, but also in a way we expected given the timing of the System z16 and Power10 product cycles. In a year and a half or so, unless IBM rolls out some upgraded processors – call them the z16+ and the Power10+, perhaps with refined chip 7 nanometer manufacturing processes from foundry partner Samsung as well as higher yields to boost the core count on the devices – then we expect for a pretty big lull in system sales at IBM.

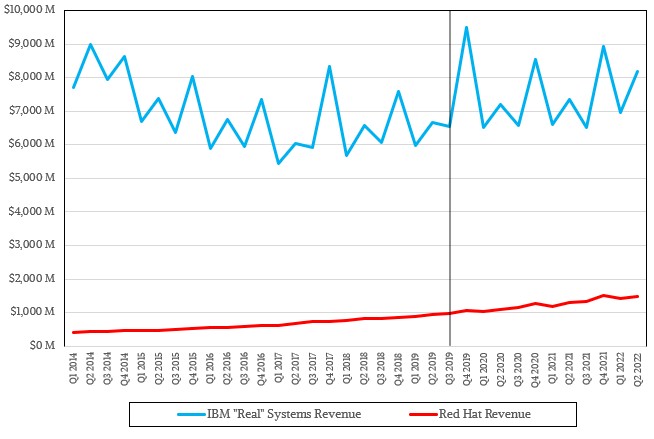

The other good news on the systems front is that Red Hat keeps plugging along, although with only 12 percent growth this quarter, to $1.47 billion, that Linux and Kubernetes business is considerably off the 20-ish percent growth Red Hat was sustaining when IBM agreed to acquire it back in October 2018 for $34 billion. In our models, we reckon that about 70 percent of the Red Hat revenue stream is for datacenter infrastructure software, such as Enterprise Linux, OpenShift, OpenStack, and a few things like Java middleware and software-defined storage. And based on that estimate, we also reckon that Red Hat broke through $1 billion in sales for subscriptions and services for such software, the second time it has done that in its history. (The first time was in Q4 2021, with $1.05 billion in sales and in this quarter it was $1.03 billion.)

IBM always talks about its groups and divisions in terms of constant currency, which means reckoning their value without taking into account the exchange rate elevation IBM gets when it converts overseas sales to US dollars. We like to think in terms of as-reported figures, just to keep it all consistent, and are happy to keep in mind the constant currency sales.

Sales in the Infrastructure group, which includes servers and storage and technical support for both, rose by 19 percent to $4.24 billion, and gross profit was only up 12.1 percent to $2,28 billion, with overall gross margins for IBM’s hardware business at 53.8 percent. Pre-tax income was $757 million, or 17.9 percent of revenues, which is the kind of profitability that a software development house can usually expect. (Somewhere between 15 percent and 20 percent is typical.) Within this Infrastructure group, sales of hybrid infrastructure – what you and I would call hardware or systems, and it is still not clear what the heck “hybrid” means when a big bank buys a mainframe to keep track of our money – rose by 34.3 percent (according to our model), hitting $2.77 billion. IBM does not provide specific revenue figures for its system sales, but said that at constant currency, the System z mainframe division had sales rose by 77 percent, and that its Distributed Infrastructure division, which includes storage as well as Power Systems servers, had a more modest 17 percent uptick (again at constant currency). Storage was the big driver here, although Jim Kavanaugh, IBM’s chief financial officer, did say that IBM “had good performance in high-end Power10.” Infrastructure support revenues came in at $1.47 billion, down 2.1 percent.

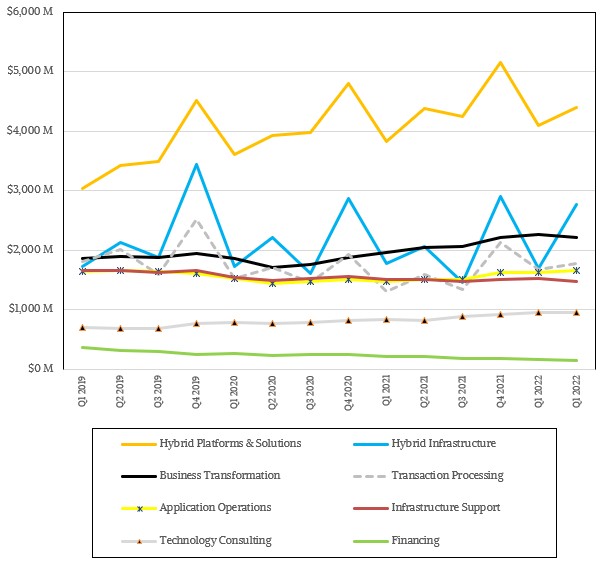

IBM’s Hybrid Platforms & Solutions division within its Software group had $4.4 billion in sales, up a smidgen, and its Transaction Processing software division, which includes mainframe databases and middleware, had sales of $1.77 billion, up 11.6 percent year on year.

If you take chunks of its Software, Consulting, and Financing groups and allocate them to systems, as we have done for years, you can come up with a proxy for IBM’s overall “real” systems business, which we think is the thing that Wall Street and customers should be looking at and worried about. We reckon that including that Red Hat systems business in the mix, IBM’s overall real systems business was just a tad under $8.2 billion, up 11.6 percent, and was $7.17 billion without those Red Hat subscriptions into the datacenter, up 11.5 percent.

As we projected many years ago, the Red Hat business has IBM’s overall systems business back on the track of growth, but remember that sales of IBM’s Power Systems and System z servers are very choppy, not the relatively smooth line that Red Hat is able to pull off each quarter – well, most quarters, anyway. The question we have is whether Red Hat can resume its historical growth rate of 20 percent, give or take.

The answer is probably no, but it is possible if not probable. We shall see.

IBM did not say much about Power10 in the call, except what we noted above and that the entry and midrange machines launched on July 12 would start shipping this week.

Add it all up, and IBM had $15.54 billion in sales, up 9.3 percent, with gross profit of $8.29 billion, up 5.6 percent and representing 53.4 percent of revenues. Pre-tax income was up by 1.9X to $1.72 billion and net income was up by 1.72X to $1.39 billion.

IBM Views Enterprise Storage Through Hybrid Cloud Glasses

For the past couple of decades, IBM’s Spectrum Scale – formerly known as General Parallel File System –has had a solid standing as one of the two go-to file systems for HPC. However, the emergence of modern workloads like artificial intelligence and analytics, coupled with the rapidly expanding growth of …

Vertically Unchallenged

Components make compute and storage servers, and servers with application plane, control plane, and data plane software running atop them or alongside them make systems, and workflows across systems make platforms. The end state goal of any system architect is really creating a platform. If you don’t have an integrated …

GenAI Races Ahead, But Enterprises Are Still At The Starting Line

The AI era has a much different vibe than prior eras in the IT industry. The pace of innovation and the amount of investment are both breathtaking. In the two short years since OpenAI’s release of ChatGPT, there has been a sprint from prompt-and-respond with pre-trained large language models to …

Be the first to comment