There are times when tectonic forces are at work in the IT world. Depending on where you focus, mountains are being ground down to sand, eliminating giants as subduction zones eat old crust and create new ranges. In other places, there is a rifting between continents, where new crust is created and islands of infrastructure isolate from each other, allowing for evolution and eventually causing a new round of continent smashing and mountain building. In yet other places, continents are grinding against each other and when they slip, they cause earthquakes.

Earth has a lot of geological drama, metaphorically, there is similar drama within the server segment. We are in a period of enormous competitive pressure as relatively new buyers – hyperscalers and cloud builders – bend suppliers to their wills thanks to the tremendous volumes they acquire while the rest of the industry decides how much of their workloads to keep and now much to deploy on top of the hyperscale and cloud capacity in one form or another.

What a difference two decades makes. It is like hundreds of millions of years in geologic time, all compressed into a few server eras. The penultimate mountain building event – technically an orogeny if we are sticking to the geology metaphor – in the recent era was when the Internet smashed into corporate datacenters, and the dot-com boom took off in the mid-1990s. It is amazing how the X86 server business has been utterly transformed by the dot-com boom and then the follow-on orogeny that has given rise to the hyperscalers and cloud builders, whose infrastructure looms as large as the ancient Appalachians at the height of the supercontinent Pangea or the current Himalayas that were created as India smashed into Asia after Pangea started breaking apart.

Back in 1995, the entire X86 server market accounted for about $5.7 billion in sales, but after the dot-com boom got into full swing by 1997, sales had more than doubled to $12 billion and shipments had also more than doubled to 1.8 million units. The X86 server market comprised about half of overall server shipments at this time, but garnered a smaller portion of the revenue pie, which was $55 billion that year. There were many ups and downs with recessions and slowdowns in the 2000s, and the server business did not explode to the $90 billion that IDC had been projecting by 2003. In fact, it has taken the hyperscale and cloud builder orogenies to create that kind of demand. In a sense, the rise of customer-facing and consumer-facing applications on a vast scale or metered infrastructure capacity on public clouds are but the logical next steps of the original dot-com mountain building. The Appalachians were built from three or four major orogenies, over many hundreds of millions of years, and the ultimate hypercloud, should it come to pass – Amazon and Microsoft and Google certainly want this to happen – will take waves to develop. If the governments of the world allow it. Which they won’t.

But the building has begun, nonetheless, and the current state of the server market reflects this as well as a substantial rise in pricing for CPUs, GPUs, DRAM, and memory.

In the second quarter, the server racket posted its best quarter in history, according to the latest statistics from IDC, with revenues up a stunning 43.7 percent to $22.53 billion and shipments up 20.5 percent to 2.94 million machines. The revenues are rising faster because of the richer configurations that companies are deploying, to be sure, and the increased volumes are also driving topline revenues. But our guess is that half of the increase in revenues in Q2 2018 was due to rising component costs. Plotting server units and server revenues shows where the two started to drift apart at the end of 2016:

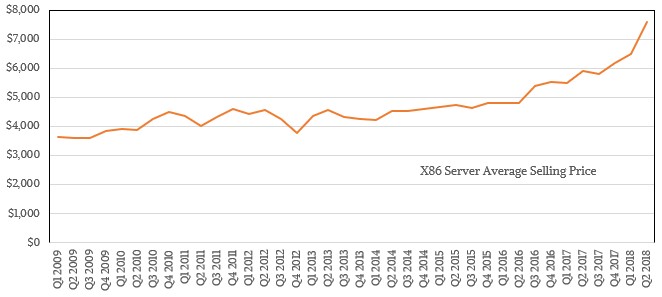

The average selling price chart below shows the increasing spread, and you can eyeball where the drift there, too:

Back in the mid-1990s, the average X86 server price was around $6,000, and as the dot-com boom ignited a firestorm of competition, those prices started to decline as each year passed. The hyperscalers and cloud builders, who buy in lots of tens of thousands of servers per datacenter and hundreds of thousands of servers per quarter, put tremendous pressure on the market with their minimalist designs and volume purchases, such that by the belly of the Great Recession in early 2009, the average selling price of an X86 server had dropped all the way down to just a tad more than $3,600 a pop. As 2017 came to an end, the X86 server ASP pushed through $6,000 and in the second quarter, because of all of the issues mentioned above, the X86 server ASP has set a new high of just under $7,500.

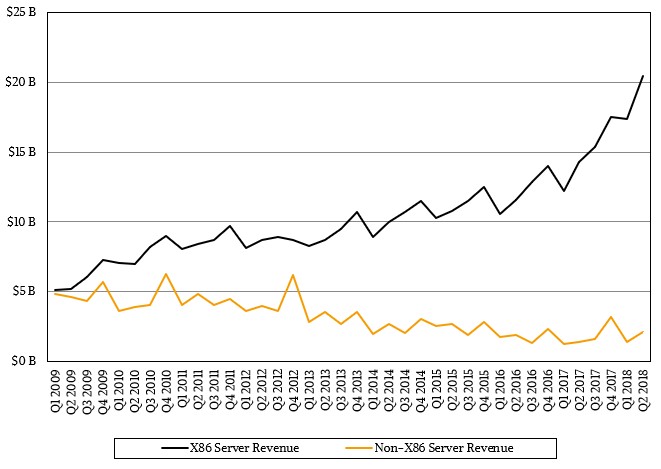

This is, in part, one of the forces that is driving the X86 server business to new heights even as competitive pressures are increasing on Intel. Sales of non-X86 iron have stabilized, but all of the growth is in X86 iron, as you can see here:

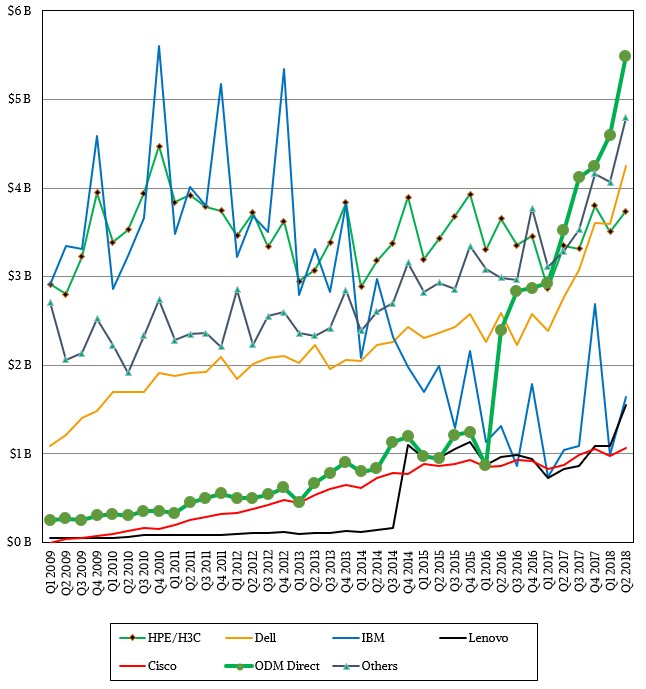

The original design manufacturers – Quanta Computer, Foxconn, WiWynn, and Inventec are the big ones – and the custom server businesses at the major OEMs that have them – Dell, Hewlett Packard Enterprise, Lenovo, Inspur, Sugon, Huawei Technologies – are the big beneficiaries of the big spending by the hyperscalers and cloud builders. Supermicro is somewhere between an OEM and an ODM and a partner supplier, and it is getting its share of the action, too. We suspect that the ODMs bring very little juice blank ink to the bottom line for their effort, at least compared to the gross profits that a Dell or an HPE or an IBM or a Cisco Systems can extract from enterprise customers who can’t create their own supply chains and use ODM manufacturers. This chart below, which breaks the ODMs out separately, shows only part of the rise of the hyperscalers and cloud builders:

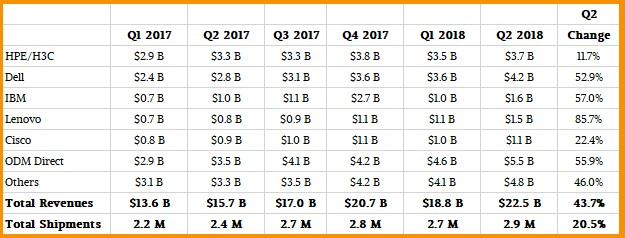

Several years after buying IBM’s System x server business, Lenovo is finally showing the kind of growth that it had expected, and Inspur, Sugon, and Huawei are coming on strong, too. But Dell is now far and away the top shipper and the top revenue maker from the server racket. In the quarter just ended, Dell raked in $4.25 billion in server sales according to IDC, up 52.9 percent and pulling up the market average, against 574,600 units, up only 16.6 percent. HPE saw its share of server shipments fall as it walked away from that unprofitable hyperscaler and cloud business with its Cloudline servers (made in conjunction with Foxconn), dropping 12.4 percent to 443,700 units shipped in the second quarter. HP’s revenues grew by 11.7 percent anyway, thanks to the addition of SGI and the partnership with H3C Group in China, to $3.74 billion.

IBM and Lenovo are in a statistical heat in terms of revenues, with IBM rising 57 percent to $1.64 billion thanks a little to the Power9 rollout in its Power Systems machines and the System z14 rollout in its mainframe base. (IBM sells relatively few machines by comparison to other vendors, and doesn’t make the top five in terms of shipments.) Lenovo had $1.55 billion in sales, up 85.7 percent from the year ago period, and was tied as the number three shipper with 224,100 machines compared to 203,200 for Inspur, which had $1,09 billion in sales, more than double from a year ago. Cisco was neck and neck in terms of revenue, with $1.07 billion in sales, up 22.4 percent, followed by Huawei with $966.8 million in server revenues in the period, up 77.1 percent.

Here is what the revenue picture looks like for all of 2017 and for the first half of 2018:

We know that HPE is under pressure trying to make money on servers, and we will be drilling into the financials of Dell to see what we can learn about this systems business.

The high end server market – yes, companies still deploy big NUMA machines running Windows Server, Linux, or Unix as well as mainframes from IBM – had a 30.4 percent jump to $1.7 billion in the quarter, largely on the strength of IBM’s System z mainframe sales. (To IDC, a high end machine costs $250,000 or more.) Midrange machines, which cost less than $250,000 but more than $25,000, accounted for $2.5 billion in revenues in the second quarter of this year, up 63 percent year-on-year as IBM’s Power9 rollout started to take affect and fat Intel Xeon platforms also made some headway. The volume server segment, which is comprised of machines that cost less than $25,000, had a 42.7 percent rise to $18.4 billion. Clearly, the volume X86 server dominates spending on servers in the modern datacenter.

For now, there is a vibrant group of server makers that are chasing various classes of customers – hyperscalers and cloud builders, distinct from smaller service providers and large enterprises and still different from the SMB segment – in different geographies. We have joked that we used to be worried about only having four or five server makers, but that the real threat to continued competitive pricing on iron is what happens when there is only a handful or server buyers – or one within a geo region. The volume economics will increasingly favor the hyperscalers and cloud builders, and the preferential engineering these customers can get also helps make it harder for others to compete and enterprises to keep their own gear. But there are always limits to hegemony in the datacenter. Or we would still all be running COBOL and Fortran programs on IBM System/360 mainframes.

There’s a funny thought. How many mainframes would it take to provide the same compute capacity as the 2.8 million or so X86 servers that shipped in the second quarter? How much money would that be? Our guess is somewhere around a factor of 5X or so higher in raw computing costs, and probably around 10X when the IBM mainframe Linux software stack is applied and taken into account. Running IBM’s own mainframe operating systems would drive the price a lot higher, for both hardware and software because IBM sets the pricing on hardware running Linux (both for z and Power machines) artificially low compared to its proprietary offerings. That’s why so much of the mainframe revenue base has been subducted, and Unix systems with their proprietary RISC processors did not fare much better – maybe they cost half as much as mainframes for a given workload. That continent has also been pushed underneath the hyperscale and cloud continents, pushing up new server vendor mountains who peddle Linux and Windows iron.

Other Than Nvidia, Who Will Use Arm’s Neoverse V2 Core?

We are still plowing through the many, many presentions from the Hot Interconnects, Hot Chips, Google Cloud Next, and Meta Networking @ Scale conferences that all happened recently and at essentially the same time. And we intend to take our usual, methodical approach of finding the interesting bits and doing …

Great Accelerations: Just How Much Will We Spend On GenAI Again?

Ever since the launch of the “Antares” MI300X and MI300A compute engines by AMD back in early December, we have been mulling over the spending forecasts for AI spending in general and for infrastructure and accelerators more specifically. With the generative AI marketing rocketing upwards on what looks like escape …

In The Absence Of A Xeon Roadmap, Intel Makes Us Draw One

One of the oldest adages in the systems business is that customers don’t buy processors, but rather they buy roadmaps. The trick with being a server compute engine supplier – whether you are talking about CPUs, GPUs, or any other kind of device – is to reveal enough of the …

Be the first to comment