As the world’s dominant supplier of switches and routers into the datacenter and one of the big providers of servers (with a hope of transforming part of that server businesses into a sizeable hyperconverged storage business), Cisco Systems provides a kind of lens into the glass houses of the world. You can see what companies are doing – and what they are not doing – and watch how Cisco reacts to try to give them what they need while trying to extract the maximum profit out of its customers.

Say what you will, but Cisco has spent the last several decades brilliantly moving from its core routing business into datacenter switching just as the dot-com boom was getting started and, more recently, jumping into servers through its Unified Computing System line of blade and rack machines.

Back in 2009, Cisco radically upset the balance of power in the systems world by merging servers and networks in the UCS line, and it has yet to find a new thing that will set its enterprise businesses on fire in such a flamboyant manner. Many thought that Cisco could not create a server business that would compete against the incumbents, and now it has a business that is generating around $3.5 billion a year in sales.

At this point in its history, Cisco is struggling to grow its core switching and routing businesses, and is focusing on the top ten hyperscaler and cloud building customers, who are increasingly interested in opening up their networking gear and less interested in the kind of closed box appliances that Cisco is known for. Precisely what Cisco is doing for these customers is unclear – it could be building custom hardware and opening up all or part of its iOS and NX-OS software stacks for all we know. What is important is that Cisco not cede this market to the upstarts that are pushing new switch ASICs and open network operating systems and that it learn from the hyperscalers and cloud builders. Many of the technologies it develops for these large customers will trickle down into its core service provider and enterprise networking businesses, and it will also inform its UCS system designs for future generations.

Cisco calls these customers megascale datacenters, or MSDCs, and as Chuck Robbins, the CEO at Cisco for the past two years, explained on a call with Wall Street analysts going over its second quarter of fiscal 2017 financial results, these companies are tough and their spending is lumpy. “I have said over and over that we have been spending a lot of time with these customers, really focused on understanding what their unique needs are,” Robbins said. “Frankly, some of them are so big that they are a market of one unto themselves. And I’m very pleased with the progress we’re making. If you look at those ten, just to give you the numbers this time, overall those ten would be down. But if you normalize out one of those providers and you take the combination of the other nine – and that one has some pretty tough year-over-year comps – the other nine were up double digits. And we have one of the largest that was up triple digits for the second quarter in a row. So I feel like we are making good progress, but we still have a long way to go.”

Getting the hyperscalers and cloud builders to buy Cisco gear is a tough trick, indeed. One wonders how this is possible, but all of these companies have always said they only make stuff because they cannot buy what they need, and given the option, they would rather buy it.

It is a little tougher sledding in the enterprise and service provider sectors, where Cisco makes the bulk of its revenues and profits. (We are fairly certain Cisco is not making any money with the hyperscalers and cloud builders, but by winning that business even at no margin, it can cut off the oxygen of its competitors, like Arista Networks, Edge-Core Networks, and Wistron, who have done well in this part of the IT market peddling networking gear.

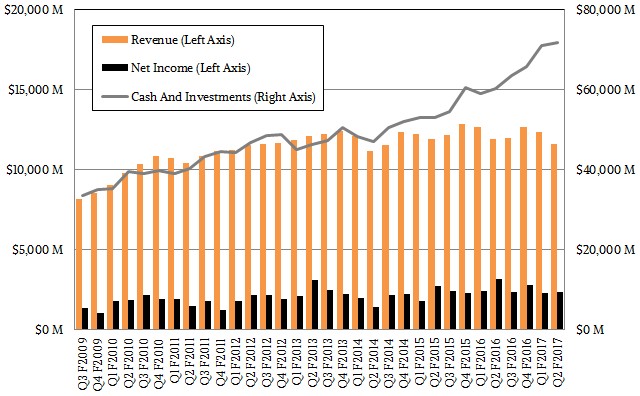

In the quarter ended in January, Cisco’s overall sales were down 2.9 percent to $11.58 billion, and net income was down 25.4 percent to $2.35 billion. This is not the direction or relative growth rates that that any company wants to see in its business. (You want revenue to grow, and net income to grow faster.) Cisco’s revenues have declined for the past five quarters, which is the result of a slowdown in enterprise spending and increased competition among service providers.

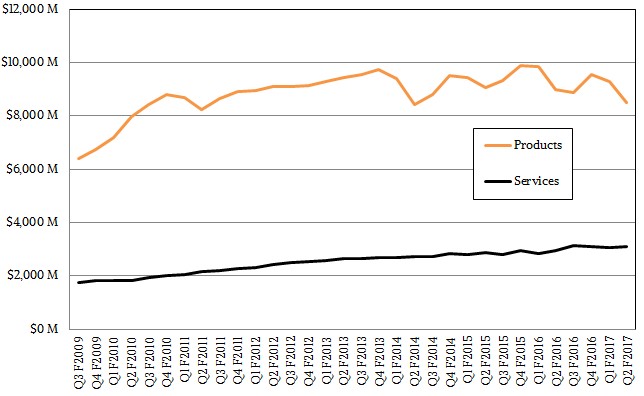

For the past year and a half, since Robbins took the helm, Cisco has been taking a page out of the IBM playbook and has been trying to build up software and services businesses that have a recurring, annuity-like revenue stream. This will make it less dependent on product sales, and to a certain extent, this strategy is working. Recurring revenue streams now account for 31 percent of revenues, up from 28 percent a year ago and up from 26 percent when Robbins took over from former CEO and current chairman John Chambers, who masterminded Cisco’s expansion from routing to a full-on datacenter hardware provider.

Looking ahead, said Robbins, the plan is to make as much of its products available as a subscription as possible – about 10 percent of current product sales were subscription-based in fiscal Q2, and the company has over $4 billion in deferred subscription revenues, up a staggering 51 percent compared to a year ago.

“As it relates to the core, I think you will see us come out with services around automation and analytics and other things that will be sold as subscriptions on top of the platforms. And the last thing I’ll tell you is that we pulled one of the key leaders from the security portfolio, who had really driven the whole product management portion of that transition to the heavy content of software and subscription that you see today, and he is now leading that force in our core networking space in the enterprise networking. So it’s clearly a focus that he’s trying to drive for us.”

The other thing that Cisco is doing to build out its software and services businesses is spending $3.7 billion to acquire application management tool maker AppDynamics, which it snapped up in late January just before the company was set to do its initial public offering on Wall Street. AppDynamics, which competes with fellow APM upstart New Relic and a slew of other incumbent management tool providers, derives 75 percent of its revenues from subscriptions. AppDynamics has already sold into 275 of the Global 2000, according to Robbins. The company had raised $314.5 million in venture capital and had an estimated market value just shy of $2 billion ahead of its planned IPO, so Cisco is paying a pretty hefty premium for AppDynamics. But AppDynamics did not have a channel program at all, and even though it was a Cisco partner, it did not have the full weight of Cisco behind it before.

On the call, Robbins was asked if there was some way to convert its base of customers, who buy switches and routers and servers, to a subscription-based model, he never really answered the question. But there is a way, of course, and it harkens back to the early days of corporate computing when companies didn’t buy data processing gear at all, but only rented it. (Not so much because it was too expensive to buy but because vendors only wanted to rent because it gave them control over product rollouts and great profits.)

Cisco is now sitting on a staggering $71.85 billion in cash, a lot of it overseas and inaccessible for doing acquisitions or anything until it is repatriated to the United States, where it is headquartered. Cisco could borrow money to build its appliances, offsetting its cash hoard without actually drawing it down and incurring taxes, and then simply offer every switch, router, and server with a monthly rental price. It would have to wait three to four years until most of the base converts from purchases to rentals. If Cisco set the rental rate fairly, then it could get off the product sales mouse wheel completely, and if Cisco made more malleable switches, with a mix of FPGAs and maybe ASICs like Cavium’s XPliant or Barefoot Networks’ Tofino chips, it could extend the life of these rented machines quite far and not incur hardware upgrade cycle costs like it is now.

It would be like the mainframe eras of the 1960s and 1970s, all over again. But in a good way, perhaps. The trick is keeping the rental and buy prices reasonably close to each other – or at least enough to not invoke the ire of customers or antitrust lawyers working for various governments.

For now, Cisco is still stuck on the product sales mouse wheel, and it shows as demand rises and falls.

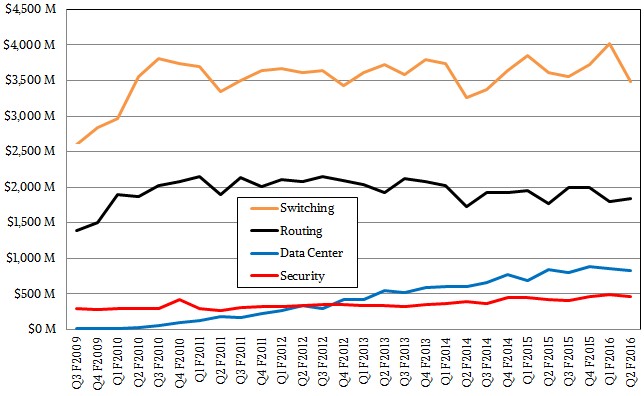

In the quarter, switching revenues were down 5.1 percent to $3.31 billion, with campus switching revenues off considerably more than this. We don’t care about campus switching here at The Next Platform, except when it puts pressure on vendors like Cisco, which bleeds into datacenter switching, either directly when the company has to pump up sales or indirectly as it has to cut costs across the board to make the company’s profits line up with revenues.

Robbins said that sales of high-end Nexus switches supporting the ACI application-centric policy management framework created by the company a few years back, had a 28 percent revenue bump in the most recent quarter. There were 1,300 new Nexus 9000 switch customers and 450 new ACI customers added in the second quarter, bringing the base to ta total of 10,800 Nexus 9000 shops and 3,100 ACI shops. (ACI runs on Nexus gear, but is not required.)

Cisco said that server sales in the quarter were impacted by a shift from blade servers to rack machines, which stands in contrast to the change the Supermicro is seeing, as its blade and modular server sales are growing faster than rack servers. The Data Center division at Cisco posted sales of $790 million, including servers and switching together in UCS systems as well as standalone rack machines, down 3.4 percent. The company’s security business, which has made a substantial shift from products to subscriptions (in part through acquisitions) had a 14.3 percent rise to $528 million. If you add them all up, Cisco’s core “real” datacenter business comprised of these four elements had a 3.9 percent revenue decline to $6.44 billion.

The thing to remember is that Cisco’s core switching and routing businesses are up by about 50 percent since the Great Recession, its security business has about doubled, and the UCS server and integrated Nexus switch businesses have been completely incremental and significant. Growth might be slowing, but had Cisco not made the changes it did, it may not have had any growth at all and it certainly would not be throwing off profits. Cisco is good a striking a balance, whether it is between in-house innovation and acquisitions in the past or shifting from product sales to subscriptions now.

More Than Anything Else, Cost Per Bit Drives Datacenter Ethernet

For whatever reason, it takes a lot longer to case the commercial Ethernet switching and routing markets, which is dominated by datacenter and campus use cases, than it does for the server and storage markets. Or, at least that is the pattern that we see in the public statements issued …

Intel Fills In The First Half Server Pothole – And Then Some

Let’s face it. Given how poorly the server market was doing in the final quarter of 2018 and the first two quarters of 2019, we had no idea how well or poorly 2019 might end up for Intel’s Data Center Group and the server industry at large. As it turns …

Hyperscalers And Clouds Switch Up To High Bandwidth Ethernet

The hunger for more compute and storage capacity and for more bandwidth to shuffle and shuttle ever-increasing amounts of data is not insatiable among the hyperscalers and large cloud builders of the world. But their appetite for is certainly always rising and occasionally voracious – even when facing a global …

Assuming you mean “Great Recession” not Great Depression…pretty sure Cisco was not around in the ’30s. Good article and interesting viewpoint. Definitely some food for though.

HA! Yes, sorry about that.

I’m a bit puzzled by your discussion of the server component of Cisco revenue. From the graph, it’s about 10% of total hardware. Although that’s a high growth rate from zero, is it actually significant? How is it supposed to become more of a winner? It’s not as if other hardware vendors are giving up.

It seems to me that Cisco’s brand has always been along the lines of “no one ever got fired for buying IBM” – corporate traditionalism. Offering a highly-integrated, completely proprietary servers-to-networking stack might work for that segment. But will it compete against the open-source, standards-based commodity ecosystem?

I speculate that the history of the industry is against the integrated/proprietary approach, which will always be limited to a minority share, and specifically not in the higher-growth sectors.