Letting go of infrastructure is hard, but once you do – or perhaps more precisely, once you can – picking it back up again is a whole lot harder.

This is perhaps going to be the long-term lesson that cloud computing teaches the information technology industry as it moves back in time to data processing, as it used to be called, and back towards a rental model that got IBM sued by the US government in the nascent days of computing and compelled changes in Big Blue’s behavior that made it possible for others to create and sell systems against what was, technically speaking, a regulated monopoly.

It is funny to ponder what the world would look like had IBM continued to fight against the provisions of the 1956 consent decree that settled the lawsuit against it by the US Department of Justice. We may have gotten to cloud computing as we know it today a whole lot earlier, but it is safe to assume that we would not have necessarily been on a Moore’s Law curve of increasing sophistication and decreasing costs that we have all benefitted from thanks to the intense competition from many platforms over the past five decades that only has Intel as its most recent champion. Digital Equipment, Novell and Compaq, Sun Microsystems, Microsoft, the Linux collective have been champions for value in their turn, and one can make a credible argument that Amazon Web Services is a platform in its own right and is also, in its way, driving the value proposition for the cloud industry when it comes to data processing and storage.

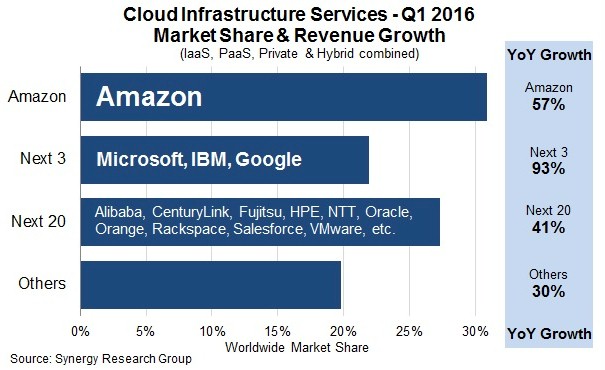

This is an industry at a peculiar point in its history, one where the market is growing at over 50 percent during the fourth quarter, with over $8.2 billion in revenues according to statistics from Synergy Research Group and still growing at over 50 percent. As John Dinsdale, chief analyst and research director at the company put it in the stats for the first quarter, which were announced late last week: “This is a market that is so big and is growing so rapidly that companies can be growing by 10 percent to 30 percent per year and might feel good about themselves and yet they’d still be losing market share. The big question for them is whether or not they are building a sustainable and profitable business. This can be done by focusing on specific regions or specific services, but the bulk of the market demands huge scale, a broad footprint, very deep pockets and a long-term corporate focus.”

Here is how Dinsdale stacks up the cloud players:

Interestingly, the United States accounts for about half of the cloud revenues in the world, according to Synergy, as was the case for computing during the mainframe era way back when, but over time we think that as the largest cloud operators learn to go local, working with partners to build clouds that are operated by regional IT or telecom companies, the cloud footprint will actually represent a larger portion of computing inside of the emerging economies than it does inside the US and other regions that dominate the established economies. China went straight to cell phones, and there is every reason to believe that China will be enthusiastic about clouds because of the centralized command and control it offers.

Amazon, with 31 percent share of cloud revenues in the first quarter, continues to dominate its peers, even though it is a pure public cloud play and is not, like Microsoft and IBM, bolstering its cloud numbers by selling infrastructure that others pay for to build their own private clouds. (Mixing acquisitions of hardware, software, and systems integration services with rentals of compute, storage, and networking capacity makes this a kind of apples to applesauce comparison, mind you. But this is the data that is out there, and this is how IT vendors talk about their cloud products so it is hard to break it down at a more atomic level.) Dinsdale says that Microsoft and Google more than doubled their revenues in Q1, and that means IBM’s SoftLayer cloud combined with private cloud revenues did not more than double. All that IBM said in its most recent financial results is that SoftLayer had double digit revenue growth and that on the broadest definition of cloud possible it had $2.6 billion in cloud-related revenues in its first quarter and that it was at an annualized run rate of $5.4 billion.

Amazon Web Services, as it turns out, had revenues of $2.56 billion in the first quarter, up 63.9 percent and giving it an annualized run rate of more than $10 billion. The operating profits for the cloud unit of the online retailer more than tripled to $604 million.

In other words, IBM’s cloud business (including actual systems) will likely never be able to catch that of AWS, no matter how generous of a definition you want to use, and the reason is simple: Amazon has well over 1 million customers who are adding capacity like crazy, and IBM has probably shrunk down to 250,000 customers, who are generally looking for a cheaper alternative, with the possible exception of the nascent market for OpenPower systems among the hyperscale and HPC elite, or whose applications are tied to IBM’s systems that it is virtually impossible for them to leave without incurring too much risk. As we pointed out last week, in about two years, AWS will probably be larger than IBM’s entire systems business, including sales of systems, operating systems, middleware, tech support services, and financing as well as its cloud infrastructure, which is largely based on X86 iron made by Supermicro.

We have said it before and we will say it again: If AWS wanted to accelerate the adoption of cloud among enterprises, it could create AWS stacks for private clouds and sell them into corporate accounts. But we think AWS and parent Amazon have done the math and figured out that this would eat into profits, something that it cannot afford to do because without AWS, Amazon is essentially not a very profitable company. In the first quarter, Amazon posted $1.07 billion in operating income against revenues of $20.6 billion, and if you do the math, that means Amazon brought 5.2 percent of its revenues to the middle line as operating profit – not bad for a retailer – but 56.4 percent of that operating profit was due to AWS, which only drove 12.5 percent of its overall sales. That is another way of saying that AWS is 9.1X times as profitable as the other businesses in the Amazon lineup.

Rather than turn itself into a distributed cloud, with lots of capacity in its own datacenters and perhaps an equal sized portion at large enterprises that want their own gear, Amazon is going for the cream of the crop, which means those who are creating new cloud native applications, those who are all-in with the public cloud, and those who are willing and able to build private clouds that are quasi-compatible with AWS when they want to go hybrid. All the grief and cost is on the customer in that last scenario, which is pretty smart when you are managing for profit and when you believe that, in the fullness of time, everyone will end up on a public cloud anyway, as AWS does.

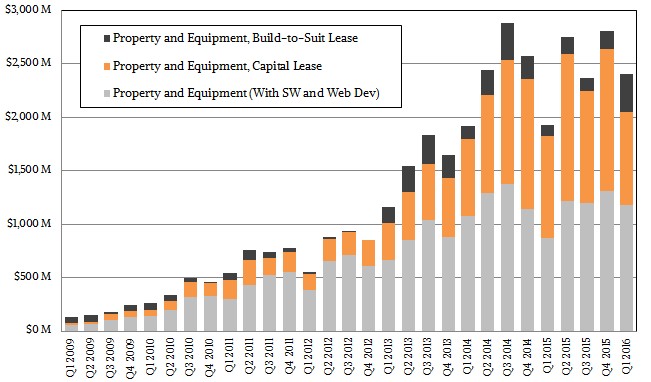

That public cloud infrastructure is enormously expensive, as you can see from the capital expenses chart above. But what seems clear is that Amazon is getting better at managing its capital, and indeed, one of the reasons why it was willing to divulge AWS numbers last year was because it has gotten better at squeezing more revenue out of its infrastructure. In the presentation above, the data for the past five quarters shows operating profits after stock-based compensation and other items are taken out, something the company started doing in the most recent quarter and backcast through the beginning of 2015. So if you are thinking AWS is less profitable than it was a few years ago, it is just that this compensation is being taken out at the group level rather than at the company level. The point is that AWS is throwing off operating profits like it is a software company, which is a neat trick for an organization that is building datacenters and all of the gear inside of it to sell infrastructure, platform, and software services on top of that.

One of the things we want to know is how large the AWS ecosystem is. In other words, what is the aggregate value of the goods and services that are sold as a platform but not including the revenue generated by the companies on the platform. Ecosystem revenues tend to be multiples of the revenues of the underlying platform revenues. The last time we did a detailed analysis of ecosystems was in 2005, when an installed base of around 19 million servers drove $365 billion in sales, with Windows comprising around 38 percent of that dough, Linux around 11 percent, and Unix about 28 percent. The multiples were anywhere from 5:1 to 8:1 comparing the underlying server platform revenues each year with the overall value of the ecosystem of hardware, software, and services sold for that platform beyond (but including) their primary vendor.

It would be interesting to separate out infrastructure services on AWS from platform services and software services from third parties to do a similar kind of analysis, and also to see at what point platform and software services will outstrip basic compute and storage services that underlie them.

So many questions, so little actual data. Pipe up if you have any, and we will start gathering our data and thoughts, too.

AWS Works Hard To Keep Ahead Of The Public Cloud Herd

Amazon Web Services is at the top of an expanding mountain, the dominant player in a public cloud services space that is expected to push past $200 billion in revenue this year and make its way well beyond $300 billion by 2022. The share of this massive and fast-growing market …

Inside Amazon’s Graviton3 Arm Server Processor

The Graviton family of Arm server chips designed by the Annapurna Labs division of Amazon Web Services is arguably the highest volume Arm server chips the datacenter market today, and they have precisely one – and only one – customer. Well, direct customer. These two facts inform the design choices …

AWS Boosts Memory Capacity On Graviton 4 Compute

UPDATED With its Graviton 4 homegrown Graviton 4 Arm server processors, Amazon Web Services has put into the field a CPU that can compete with all but the toppest of bin parts from AMD for X86 CPUs and Ampere Computing and Nvidia for Arm CPUs, and it is driving price/performance …

Be the first to comment