Three years ago, thanks in part to competitive pressures as Microsoft Azure, Google Cloud, and others started giving Amazon Web Services a run for the cloud money, the growth rate in quarterly spending on cloud services was slowing. In the last few quarters, the rate of spending has begun accelerating again, thanks in large part to the exorbitant costs of hosting AI training and inference workloads in the cloud.

While the improved growth rates are welcomed by the cloud builders, John Dinsdale, chief analyst at Synergy Research Group, which keeps a close eye on cloud spending and hyperscale datacenter buildouts around the world, says that the market will not return to the higher rates seen before 2022. The coronavirus pandemic was driving cloud adoption like crazy between 2020 and 2022, and not only that, the cloud market had not yet been affected by the limit of large numbers that ultimately slows growth in all markets.

As we are fond of pointing out, the cloud market is going to outgrow global gross domestic product for as far out as we can see, and both cloud market revenues and the capacity of hyperscale datacenters in the aggregate are expected to double in the next four years. The annualized run rate for global cloud services – including IaaS, PaaS, and hosted private cloud capacity – was more than $300 billion and growing at 21 percent in the first quarter of 2024.

To be more precise, in Q1 2024, Synergy Research estimates that cloud services generated $76.5 billion in revenues, with trailing twelve month revenues at $283 billion. That it can hit $600 billion in a mere four years seems fantastical, but that is the forecast that Dinsdale is making for 2028.

Interestingly, AWS accounts for 31 percent market share of revenues – down a few points from its historical average. Microsoft Azure is closing the gap with AWS with a 25 percent share. Google is number three at 11 percent share. Microsoft and Google are outgrowing AWS, as has been the case for some time now. And with the GenAI boom well under way, it is not unreasonable to contemplate when Microsoft will be as big of a cloud player as AWS – and as we have already shown in our analysis, Microsoft is a bigger core platform provider than AWS and likely will always be unless AWS buys IBM. (Which is a funny thought.)

So that’s the money. Let’s talk about the datacenters for a minute before we dive into the financial results of AWS, Microsoft, and Google. (Yes, we know the company is called Alphabet, but Google is the only part we really care about here at The Next Platform.)

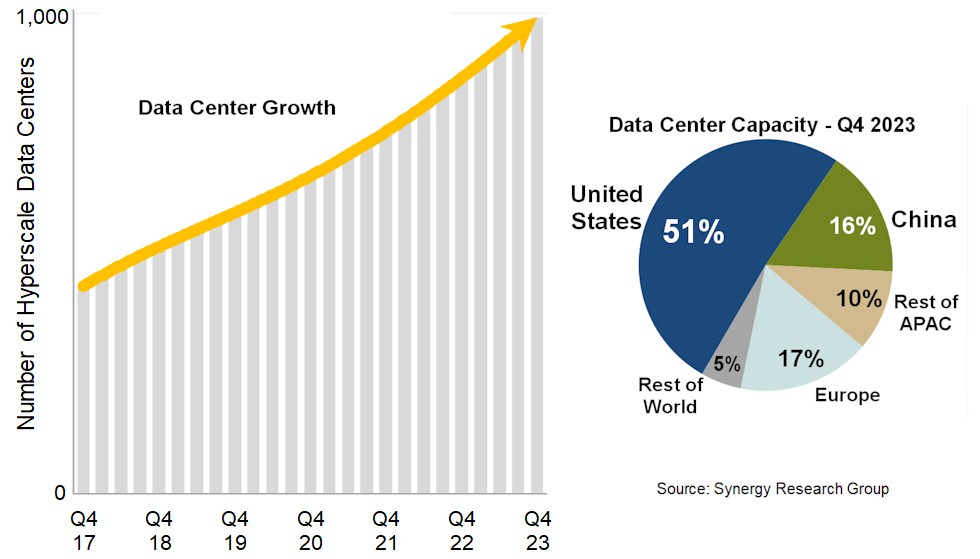

As 2023 was coming to a close, Dinsdale says that there were a total of 992 hyperscale datacenters in the world, which is 4X the number that were in existence four years ago. In Q1 2024, the number of these massive datacenters (which hold tens of thousands and sometimes 100,000 servers), passed through 1,000 worldwide.

Going forward, Dinsdale expects for somewhere between 120 and 130 additional hyperscale datacenters to be built, and as you might be surmising, GenAI is the core driver in this new capacity. And thus, in the next four years, because the power and compute density of machinery is rising faster than the datacenter count, the aggregate gigawatts of power used by hyperscale datacenters will double even though the datacenter count will only increase by about 50 percent to 1,500 worldwide.

As you might imagine, Dinsdale can’t give away too much data – this is how Synergy Research makes a living, after all – but he was helpful when we asked about how the aggregate power load has changed in the past four years and how it will look four years from now.

“I can tell you that hyperscale datacenters typically range from around 6 MW at the bottom end up to around 70 MW at the top end in terms of critical IT load capacity,” Dinsdale tells The Next Platform. “Then, of course, a campus may have multiple datacenters on it, so campus capacity can go way higher than those numbers. If you were to assume that across those thousand datacenters the average size was somewhere in the 20 MW to 30 MW range, then that might be a reasonable guess on your part. While there are hundreds or really big hyperscale datacenters, there are also hundreds of smaller local facilities in the mix that are still big enough to be considered hyperscale.”

So 25 GW to 30 GW of total critical IT load capacity for the hyperscale datacenters, and rising to maybe 50 GW to 60 GW four years from now and probably only 10 GW to 12 GW four years ago. Thanks, John. Appreciate it.

This bit of data analysis from last July from Synergy Research puts the hyperscalers and clouds in perspective with the rest of the world:

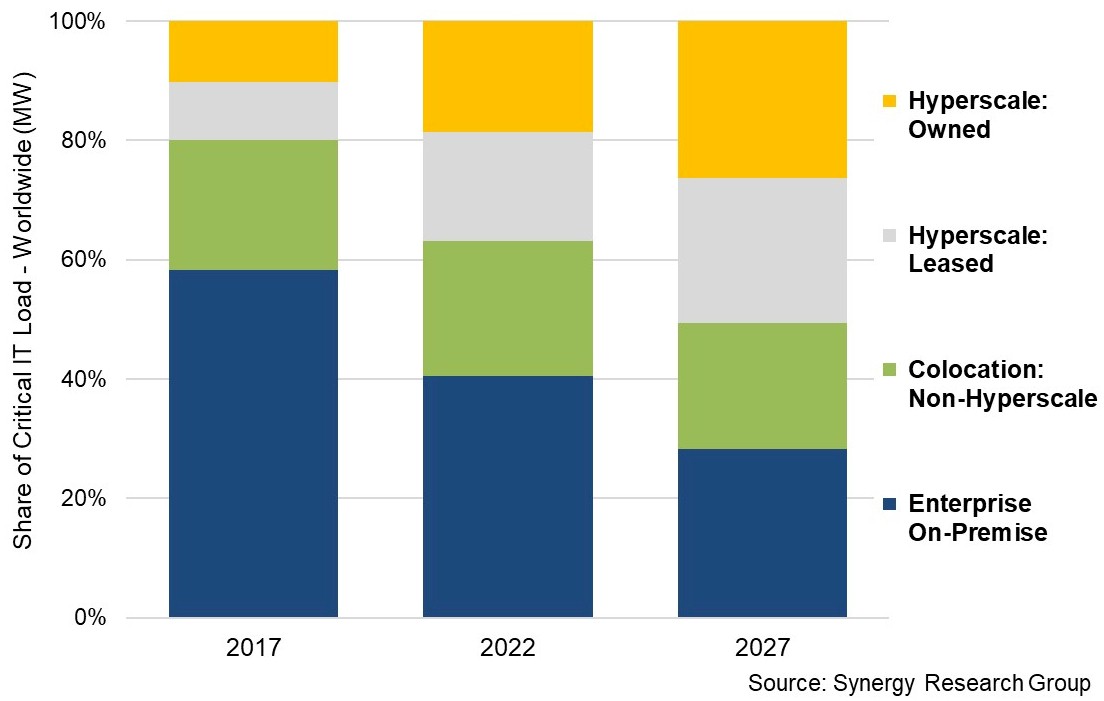

Back in 2017, the hyperscalers (which includes what we here at The Next Platform call the big cloud builders in the way that Synergy Research uses the word) accounted for 20 percent of the critical IT load, expressed in MW, in all of the datacenters in the world. There was a pretty even split between hyperscale datacenters owned by their companies and those that are leased from third parties. On premises enterprise datacenters comprised just under 60 percent of the critical IT load. The remaining slightly more than 20 percent was for co-location facilities in use by enterprises. So enterprises were 80 percent of the critical IT load and hyperscalers and cloud builders were 20 percent.

By 2022, the hyperscale datacenters were approaching 40 percent of the aggregate datacenter power, with on premises enterprise datacenters having 40 percent of the capacity and co-location facilities used by enterprises making up the remaining more than 20 percent.

Fast forward to the 2027 forecast from Synergy Research, and on premises enterprises will comprise a little more than a quarter of the overall power, co-location datacenters will have a little less than a quarter of the total, and hyperscalers will have slightly more than half of the total.

The datacenter world will have turned on its head – and not because companies don’t have datacenters, but because the hyperscalers are going to do the massive GenAI buildout that will be too expensive and disruptive for most enterprises to tackle.

That is our interpretation of the data, not that of Dinsdale and his team, and we are not so sure this is how it will play out. We see enterprises building a lot of smaller GenAI systems and using open source software and pretrained models that they augment with their own data and that they will want to have residing next to their production systems so they can hook directly into their applications. Big companies are control freaks about their data, and it is always wise to remember this. Small companies can rarely afford to be, and this is how the world will split.

With that as background, let’s take a look at the latest financials of the platform businesses of AWS, Microsoft, and Google. We like to try to figure out how large the core systems businesses are at the big clouds as well as the major public OEMs of the world so we can reckon the size and shape of the overall systems. This is different from – and complimentary to – just counting revenues at AWS, Microsoft Azure, and Google Cloud or the big OEMs.

In the quarter ended in March, AWS revenues rose by 17.2 percent to just a tad over $25 billion, beating its own forecasts (which is not hard) as well as those of Wall Street (which is always more ambitious than company forecasts because every company under-promises and over-delivers). More importantly, and thanks in large part to the GenAI boom, operating income at AWS rose by 83.9 percent to $9.42 billion, setting a record high profit as share of revenue of 37.6 percent.

Now, we know what you are thinking. The rest of Amazon is still not very profitable. Incorrect! Amazon proper is making money from its online store, its burgeoning advertising business, and its media empire. In the March quarter, the non-AWS parts of Amazon grew by 11.6 percent to $118.28 billion, up 11.6 percent, and it had an operating income of $5.89 billion, or 5 percent of revenue, compared to an operating loss of $349 million in the year ago period. The Amazon parts are getting more profitable as the quarters go by, and we think this is all due to the steady hand on the tiller by Andy Jassy, the chief executive officer who used to run AWS and who replaced a distracted Jeff Bezos in that CEO role.

If you peel the compute, storage, and networking parts of AWS away from databases and applications sold as a service, you can get a sense of the size of the “real” systems business at AWS. In our model, we reckon that this underlying systems business at AWS brought in $12.77 billion in Q1 2024, up 15 percent, and that its operating income hit $4.08 billion, up 80.4 percent and comprising 32 percent of revenues. The AI tools like SageMaker and Bedrock are, in our thinking, applications, not middleware. Draw your lines where you will.

Let’s move on to Microsoft, which posted $61.86 billion in revenues, $27.58 billion in operating income, and $21.94 billion in operating income in the March quarter, which was the third quarter of its fiscal 2024 year.

The chart above shows the revenue streams from its three groups. The most interesting one for us is the Intelligent Cloud group, which includes Windows Server, SQL Server, Visual Studio, and other middleware and tools sold into the datacenter, including compute, storage, and networking capacity on the Azure cloud and related platforms and SaaS services Microsoft peddles into the datacenter.

In fiscal Q3, Microsoft’s Intelligent Cloud revenues were $26.71 billion, up 21 percent, and its operating income was $12.51 billion, up 32 percent and presenting 46.9 percent of revenues. (We are allocating operating income proportional to revenue in our model because we have no better method at the moment.) If we extract out development tools, databases, and other stuff that is not part of a base system, we can approximate Microsoft’s “real” systems business, which includes sales of the Windows Server stack for on-premises IT and as well as raw infrastructure – compute, storage, and networking – on the Azure cloud.

Our best guess is that this “real” systems business at Microsoft drove $19.39 billion in sales in the March quarter, up 31.4 percent, and its operating income was $9.08 billion, up 43.4 percent and representing 46.9 billion.

This profitability is remarkable given the investments that Microsoft is making for AI infrastructure, but it is also possible given the massive installed base of Windows Server licenses and support sold into enterprises around the world, who have not only been underwriting Microsoft’s cloud investments for the past decade, but who are also its most natural customers for cloud services.

One note: This systems revenue shown above is not to be confused with a category that Microsoft calls Microsoft Cloud, which is any and all services it sells from the cloud, for clients as well as servers. This category has a very large SaaS component, obviously, including Office 365, Active Directory, and all kinds of enterprise applications sold as a service.

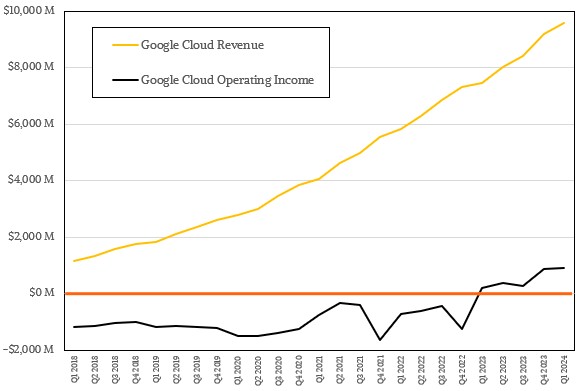

That leaves Google Cloud, which, like its larger AWS and Microsoft Azure rivals, has a mix of infrastructure, platform, and software services that it sells, but it is so small, relatively speaking, that we have not yet attempted to break its “real” systems revenues separate from higher level database and application services.

In the first quarter, Google had sales of $80.54 billion, up 17.1 percent, operating income of $25.47 billion, representing 31.6 percent of revenues and up 46.3 percent. Net income was up 57.2 percent to $23.66 billion.

Google Cloud had sales of $9.57 billion, up 28.4 percent, representing 11.9 percent of sales. The advertising and search business drove 87.4 percent of sales in the quarter and is generally somewhere around 89 percent of the total in recent years.

The interesting bit for Google cloud is that a shift in bookkeeping that depreciates servers, storage, and switching over longer terms has made the cloud business profitable. Google may be the third largest cloud provider in the world, but it is far from being the most profitable, and even when it is larger, it is hard to see how it will be more profitable than Microsoft or even as profitable as AWS.

But only a fool counts Google out over the long run, and in the longest of runs, it may turn out that across North America and Europe, if not the whole world, Microsoft, AWS, and Google all end up with around a quarter of the cloud market each and the remaining quarter comprised of sovereign and specialist clouds (like those focused only on HPC and AI with accelerators).

The Debate Over Regulating AI Ramps Up

Sundar Pichai, CEO of Google and parent company Alphabet, generated a lot of buzz recently with an op-ed he wrote for the The Financial Times calling for greater regulation of artificial intelligence (AI) technologies, adding a high-profile voice into a debate that has been simmering as innovation around AI, machine …

Sky-High Hurdles, Clouded Judgements for IaaS at Exascale

Back in 2009, I was the editor of a mini-side publication from supercomputing magazine, HPCwire, called HPC in the Cloud. At that time, the concept was new enough to warrant a formal division between what HPC was and what it would eventually be–and its own dedicated coverage. The first ISC …

You Are Paying The Clouds To Build Better AI Than They Will Rent You

Think of it as the ultimate offload model. One of the geniuses of the cloud – perhaps the central genius – is that a big company that would have a large IT budget, perhaps on the order of hundreds of millions of dollars per year, and that has a certain …

“So 25 GW to 30 GW of total critical IT load capacity for the hyperscale datacenters, and rising to maybe 50 GW to 60 GW four years from now and probably only 10 GW to 12 GW four years ago. Thanks, John. Appreciate it.”

Hmmm so if the US is ~50% of hyperscale/Cloud data centers (30 GM -> 60 GW in 4 years / 2 = 15+ GW additional required just in the US (take that math with a large grain of salt))…Where is this extra datacenter power going to come from? Not that anyone is going build out any of this server capacity on the new(ish)2me sandbar home sticking out into the Atlantic (Cape Cod). But I note the ongoing modest pace of getting our 800 MW wind farm online (Vineyard Wind I), that as far as I know BestBuy doesn’t sell SMRs yet, and West Virginia is slowing down the deco of fossil fuel plants to keep that power flowing to the DataCenter Capital of the world…

Oh and we want to covert ground transportation to all electric, convert heating to heat pumps and decarbon the grid…It would seem that a SpaceBalls-esq (“They went plaid!”) increased speed datacenter build out would have some competition for that additional power needed over the next 4 years.

…Just my 2 cents.

Yeah, I guess we will have to all stick with internal combustion engines so we can replace our functions with AI? I agree the numbers are large, and the grid can’t handle its job today much less this massive datacenter buildout and EVs too. Mr Fusion? We certainly could solve a lot of problems with free-ish power. . . .

If MR Fusion worked, it would do wonders for banana peal recycling…

…Well its a hard problem to solve, and I’m sure greater minds than mine are working on it. I doubt Nvidia is going to let themselves lose out on their next $1T in additional market cap because no one can plug in their B100s.