Imagine, if you will, how troublesome AMD’s chip business would be at the end of 2022 had it not decided way back in 2015 to re-enter the datacenter with its Epyc processors. And imagine further how 2022 might have turned out – and how 2023 might be – if it had not shelled out an enormous amount of money to acquire the suddenly fast-growing and very profitable Xilinx FPGA business?

Scary, isn’t it?

As it is, 2022 ending with a bit of a wheeze and the first half of 2023 looks to be problematic not only for Intel, which has plenty of issues including stuffing the channel and the hyperscalers and cloud builders (who are channels of a sort in their own rights) with too many PC and server CPUs. Well, AMD has the same problem, as Lisa Su, the company’s chief executive officer pointed out in a conference call going over the financial results for AMD’s fourth quarter of 2022.

The situation is not anywhere close to dire for AMD, and in many ways it is for Intel, as we pointed out last week in our coverage of Intel’s Q4 2022. But it is concerning. But AMD has a strong roadmap, has had flawless execution on its roadmap – it’s only delay was a two-quarter tweak for its current “Genoa” Epyc 9004 processors to allow for the addition of the CXL memory protocol to the PCI-Express 5.0 interconnect, which was the right thing to do – and is poised to make Intel’s life a bit harder with the launch of the 128-core “Bergamo” Zen 4 processors sometime in the first half of this year. Genoa-X will come along at some point and put some additional pressure on Intel’s “Sapphire Rapids” Xeon SPs, but Intel has a pretty good counter there with the HBM variants of these chips, known as the Xeon Max Series.

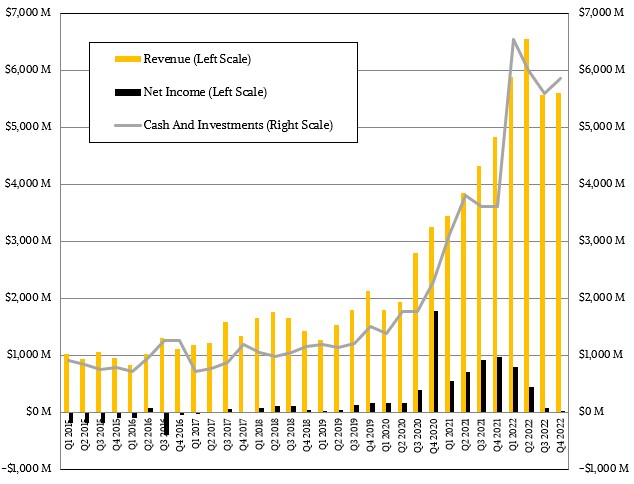

In the December quarter, AMD’s sales were up 16 percent to $5.6 billion. This despite a collapsing PC chip market that has been the victim of its own pandemic-driven optimism. (We all bought lots of PCs. We’re good for a while.) AMD took a $443 million charge to amortize assets acquired from Xilinx (and probably a tiny bit from Pensando), which knocked its gross margins down by seven points to 43 percent. Research and development costs exploded by 68.4 percent to $1.37 billion, there was another amortization charge of $601 million (mostly for Xilinx , plus a $5 million licensing gain, which pushed AMD down to an operating loss of $149 million. Thanks to $3 million in equity income and a $154 million tax benefit (companies keep these things around for rainy days), AMD posted a meager net income of $21 million. For all of 2022, AMD has whacked a total of $3.55 billion in amortization costs against its books related to acquisitions. If there was a year to do it, that was the one. Now that is done. But it has all meant that AMD swung from a $974 million profit down to a $21 million profit in Q4 2022.

And just in time for 2023 to get off to rough start as enterprise and government spending is slowing at the same time that the hyperscalers and cloud builders are digesting the CPUs (and very likely the GPUs and FPGAs) they acquired in the third and fourth quarters as both Intel and AMD did a private launch with the hyperscalers and cloud builders, the dominate buyers in the IT sector who don’t just go to the front of the line but don’t have to stand in line at all. They get what they want even before a launch.

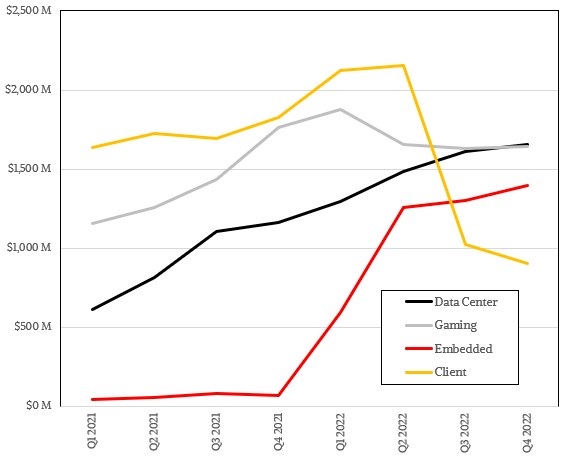

In the quarter, AMD’s Data Center group was the top revenue generator for the company for the first time in its history, toping its gaming GPU and console business, which has also slowed, The embedded business that is largely based on the Xilinx FPGA portfolio continues to grow, and it probably won’t be long before it is at parity with the Data Center and the Gaming groups. Who knows when the Client group will rebound, but it had an operating loss of $152 million against $903 million in sales in Q4. Data Center group had $1.66 billion in sales, up 42.3 percent, and an operating income of $444 million, up 20.3 percent. The Embedded group had just a tad under $1.4 billion in sales and an operating income of $699 million.

The datacenter and the edge have made AMD resilient to the downturn in the PC market. But only because it has executed well, first by building a credible server CPU business and second by acquiring Xilinx. The fortunes generated by the first (both cash and market capitalization) enabled the latter.

As best we can figure from what AMD said on the call and from our model, AMD generated $1.58 billion in sales from datacenter CPUs, up 55.1 percent. AMD said on the call that sales of datacenter products to hyperscalers and cloud builders more than doubled (as it has been doing for a while), and we think that means $1.18 billion in CPUs were sold to the hyperscalers, mostly those based in the United States. We reckon that sales of Epyc CPUs aimed at enterprise, government, academic, and telco/service provider users were down 11.5 percent to $394 million after a pretty good quarter a year ago.

Datacenter GPU sales faced a tough compare with AMD helping Hewlett Packard Enterprise build out the “Frontier” supercomputer at Oak Ridge National Laboratory, which has 37,888 of AMD’s “Aldebaran” Instinct MI250X GPU accelerators. We figure Datacenter GPU sales fell by 49.2 percent to $75 million in Q4.

For the full year, we think AMD had $5.74 billion in sales of datacenter CPUs, up 75 percent. Intel’s Data Center & AI group had sales of $19.2 billion in 2022, and if you assume that 75 percent of Intel’s DCAI revenue is for server CPUs, then Intel had 71.5 percent revenue market share of the datacenter X86 server CPU market and AMD had 28.5 percent market share. If you assume a higher share of Intel’s sales came from CPUs and not chipsets, motherboards, and other stuff, then AMD’s share of the X86 market in datacenter servers drops.

Also for the full year, we think hyperscalers and cloud builders bought $4.25 billion in AMD CPUs, more than double of that from last year, and sales to all other companies and organizations rose by 29.1 percent to $1.49 billion. Given all this, datacenter GPU sales fell by 35.7 percent to $295 million for 2022.

Looking ahead, Su & Company say that the datacenter business will shoulder a “double digit decline” in the first quarter of 2021 “that is more than seasonal” but adds that the Xilinx FPGA business will grow in the single digits in Q1 2023. AMD expects for Data Center group to have a tough Q2 as well, but for it to grow enough in Q3 and Q4 for the datacenter business to grow for all of 2023 once the beans are all counted in January 2024. The Embedded business is expected to grow in the first half, but Su was not prepared to say how the second half would do given how strong 2H 2022 was, but the company does anticipate that Embedded group will grow sales in 2023. AMD is planning for declines in the Client and Gaming groups in 2023.

No company is big on providing detailed or long-term guidance right now, but AMD did say that it expects for Q1 2023 revenues to be around $5.3 billion, plus or minus $300 million, which is a decrease of 10 percent at the mid-point year-on-year and a decline of 5 points sequentially at the midpoint.

Supermicro Throws Its Weight Behind Arm Servers

Supermicro has become the latest of the big OEMs to add Arm-based systems to its portfolio, with the launch of its Mt. Hamilton platform based on the Altra line of Arm CPUs from Ampere Computing. Since Amazon’s Graviton chips aren’t available outside of AWS, and Nvidia has yet to ship …

AMD At A Tipping Point With Instinct MI100 GPU Accelerators

It is hard enough to chase one competitor. Imagine how hard it is to chase two different ones in different but complementary markets while at the same time those two competitors are thinking about fighting each other in those two different markets and thus bringing even more intense competitive pressure …

How The “Antares” MI300 GPU Ramp Will Save AMD’s Datacenter Business

It is beginning to look like AMD’s Instinct datacenter GPU accelerator business is going to do a lot better in 2024 than many had expected and that the company’s initial forecasts given back in October anticipated. But make no mistake. The GenAI boom cannot yet make up for the ongoing …

>>datacenter GPU sales fell by 35.7 percent to $295 million for 2022

According to CEO Su, AI is the most important initiative for AMD, so this can only be characterized as a limp effort. Backing Mellanox out of Nvidia’s Data Center numbers, Nvidia is selling close to $10B GPUs (TTM) in DC, or 34X AMD’s effort. So AMD is responsible for 3% of GPU data center sales by revenue. Not sure how they get onto the AI solution short list, but if it’s their most important segment, they better get on with it.

It all starts with good–and cheap by comparison–hardware. They did that with MI250X. We will see how MI300 does. But there had better be some MI300 discrete GPUs, and they better have some heft.

It sure would help also if AMD had a turnkey distribution of ROCm etc for the major linux distros.

AMD 2022 on financial on channel data;

AMD revenue per unit = $149.82

Less Fixed @ $102.07

Less Variable @ $29.89

Average Total Cost = 131.97

Net Take $17.85 on 157,525,123 units = $2.812 B

Note cost of sales per unit $17.48; mc = mc = sales pays for itself

Less ammonization acquisition related $1.448 B and change $1.492 B

Profit = $1.320 B

Data Center (Epyc primarily) = 6,708,038 units at net take $900

Specific DC GPU Vega and RDNA ll accelerators returned to the channel = 5.3% of Vega generation, 1.6% of RDNA ll generation and 0.08% of RDNA lll generation

Client desktop and mobile = 69,608,787 units at net $89

Gaming = 76,502,442 units at net $89 of which 60 M are console and remaining dGPU

Embedded = 4,705,656 units at $967.35 q2 through q4 2022

Mike Bruzzone, Camp Marketing