As you might expect, we believe in the strength, resilience, and utility of platforms and we carefully watch as companies emerge and try to commercialize them. And like many industry observers, we have taken a keen interest in the hyperconverged server-storage hybrid that was conceived of by the founders of Nutanix way back in 2009, which dropped out of stealth in 2011 and shipped its first product virtualizing both compute and storage a year later.

The word on the street – and that would be Wall Street we are talking about – is that Nutanix is “exploring a sale after receiving takeover interest,” and that private equity and industry players are either poking around or being shopped the idea.

Perhaps someone poked and a whole bunch of others are being shopped to get the best price possible. What we know is that Wall Street already owns Nutanix, which has been public since September 2016, and that it can be taken over by an aggressive buyer any time they want to take dump trucks full of cash down to Wall Street and start buying up shares.

This seems like an odd time for a third party to want to buy Nutanix, but a year ago it had a market capitalization in excess of $9 billion, which bottomed out at $3.1 billion back in June of this year. That market cap climbed back up to $5 billion before the acquisition rumors were swirling late last week, and as we go to press today it is kissing $6 billion. Just a few days of rumors added 20 percent to the asking price, and waiting only three months has doubled it.

That’s almost as bad as trying to buy a car these days. . . .

Anyway, if there is a deal in the works, it should have happened back in June and it is getting more expensive by the day for no good reason other than the fact that Nutanix has been able to rein in its losses somewhat in recent quarters and everybody seems to be expecting some sort of deal. This is a silly reason for the company’s stock to move so much, but that’s Wall Street for you. Or maybe it’s Numberwang. No, it’s definitely Numberwang….

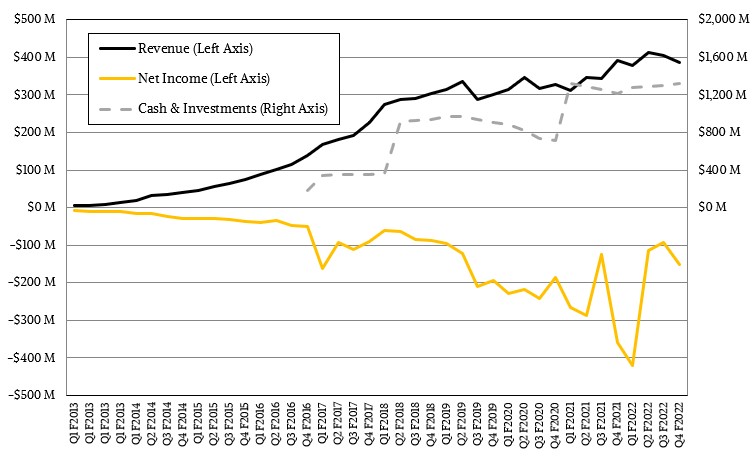

If Nutanix actually made revenue grow and broke even for four consecutive quarters and was on the way to consistent profitability, that would be a good reason to be worth maybe $6 billion, especially for a company that has $1.32 billion in cash in the bank.

As you can see, the financials at Nutanix are improving, but it also looks like sales are getting a bit wiggly, and the company just laid off 4 percent of its workforce, too. Everyone is jumpy right now, and Nutanix is no exception, even with all of that cash in the bank.

In the trailing twelve months, Nutanix had $1.58 billion in sales, up 13.4 percent, and chopped its annual net loss by a quarter to $778 million. But that is still a huge loss, and there is no way to get around that. In the prior nine years that we have financial data, Nutanix has brought in $8.29 billion in revenues and booked a staggering $4.48 billion in losses.

Nutanix is a good company with a polished product that, as we have pointed out before, should be a platform akin to the DEC VAX of the 1980s, the IBM AS/400 of the 1990s, and the Microsoft Windows Server of the 2000s. Meaning, given so many small and medium businesses that want virtualized compute and storage that is resilient and easy to manage, and that can scale by just popping a few more servers onto the network, you would expect for Nutanix to have 200,000 customers – or maybe even 2 million customers – by now, not the 22,600 it ended its fourth quarter of fiscal 2022 with back in July.

For whatever reason – and we think it is simply the price of the Nutanix stack is too high even though the value is great for the kinds of customers for which this is most useful – the Nutanix base is smaller than we thought it would be and not growing very fast anymore.

The Nutanix customer base would be organizations with at least three servers running the normal set of infrastructure, all the way up to hundreds or thousands of nodes. Nutanix has been able to scale its hyperconverged infrastructure to thousands of nodes for years, and even has some customers that do that and that also spend millions of dollars per year on licenses and support. Which is why we cared about Nutanix at all. There was always a chance that this pyramid would be quite large and scale, in production, like many other distributed computing platforms we follow.

To make that pyramid base larger, we suggested this time last year that maybe IBM should buy Nutanix. Big Blue doesn’t have a broadly appealing systems business anymore — the Power Systems and System z businesses are good and profitable, but niche — that the combination of Red Hat and Nutanix might make some sense, and even help sell some Power iron. But since then, IBM has actually separated Red Hat from its Gluster and Ceph storage businesses — funny, the storage business has become disaggregated as well as the storage itself — and merged these into the Storage division of its Systems group. Maybe IBM is thinking this. Maybe the IBM Cloud could differentiate itself this way.

Nutanix also represented a polar opposite to the approach taken by the hyperscalers and cloud builders, who disaggregate storage from compute, using massive Clos networks running at Layer 3 of the network to interconnect everything together in a massive cluster spanning 50,000 to 100,000 nodes that offer reasonably deterministic performance. In the battle of hyperconverged compute and storage, with a shared hypervisor substrate running over Layer 2 networks, versus disaggregated compute and storage as embodied by Amazon Web Services, Google, Microsoft, and Facebook, it was not clear which one would win out in the enterprise.

Maybe the issue holding back Nutanix really is the price, and that means with the right cloud underneath it, that cloud can amortize that cost at the same time as giving their enterprise customers something that feels like their own private compute-storage cluster in the cloud. A new kind of logical partition, but at the cluster level, not a fractional node level.

Maybe one of the reasons why a lot of customers are still computing and storing on premises, at both small and large scale, is that the cloud is just too different. And maybe, just maybe, a big cloud – that means you, AWS, Microsoft, or Google – could take the Nutanix stack and add it as an overlay to their disaggregated infrastructure to give customers not a hodgepodge of interlinked services, but something that looked and smelled and was secured like a distinct system. That might attract who knows how many tens of thousands to millions of customers to the cloud, pulling their infrastructure out of on premises datacenters. But only if that acquiring cloud took a very long view on how it was going to get all of that money back.

Nutanix might be a quick and dirty way to get a hybrid cloud setup going across enterprises, governments, and academic institutions, allowing them to run their Windows Server and Linux applications “as is” but on that virtualized server-storage substrate that makes it feel like a distinct system. They would probably pay a premium for such a comfort level – but almost certainly not what Nutanix is charging today. And that includes its ongoing transition from selling software licenses and support contracts to selling subscriptions that span multiple years.

But only a company with deep pockets in proprietary software, or advertising, or cloudy infrastructure (or a mix of these in some cases) can take that long view. And frankly, as thought experiments go, we admit this one is pretty weak. But so is the idea that some private equity firm is going to buy Nutanix for a premium over its current market cap and despite its limited growth and continuing losses, take a hatchet to the payroll, make it profitable, and then sell it for a 1.5X or 2X multiple of what they paid for it.

It can happen, and it might even happen, but that doesn’t mean it actually makes any sense. But maybe what we suggest above could make sense. Maybe.

IBM Starts Walking The Hybrid Cloud And AI Talking

If Big Blue is going to talk the hybrid cloud and AI talk, as it seems to do incessantly, then the company has to walk it. And perhaps the most interesting thing that was said as part of the company’s discussion of its first quarter 2023 financial results was its …

IBM Bets Big On Native Inference With Big Iron

Everyone knows that machine learning inference is going to be a big deal for commercial applications in the years ahead, but no one is precisely sure how much inference is going to be needed. There is, however, an increasing consensus that for enterprise customers – as distinct from hyperscalers, cloud …

Hyperconverged Server-Storage Hybrids Land New, Modern Workloads

Hyperconverged infrastructure came out of fairly humble beginnings almost a decade ago. And while it has not taken over the datacenters of the world as many predicted, these virtualized server-storage hybrid platforms now sport virtual networking and management software integrated into a single appliance and they have found their place. …

ARM shops (maybe Ampere; maybe HPE …) might benefit from being able to offer a hyperconverged (integrated) software/infrastructure solution such as this (on top of their hardware). I don’t know if Nutanix works on ARM though … Real-world successes of Apple’s M1/M2 and Fujistsu’s A64FX suggest that ARM has reached practical useability, but availability of enterprise software may still be lagging (hence the great opportunity, especially with Altras, Mystiques, Graces, and the likes, soon to come online hardware-wise).

Nutanix isn’t growing because HCI just does not make sense. HCI provide for scaling compute and storage incrementally. But for a large enterprise or cloud provider that is not necessary and SMB should just go the the cloud where the advantages are numerous.

I don’t know where the product is now, having gotten out of the physical appliance business and pushing their own AHV hypervisor, but in the 3yrs I was a customer (2016-19), it was a decent product with good support but was really fragile, resource inefficient, and pretty expensive. It doesn’t surprise me at all that their customer numbers aren’t what some would expect. They were a first-mover in the hyperconverged space, but these days are they really unique enough to be a good takeover target?

Private equity is drowning in undeployed cash which is what has driven deal values so high. That has not changed. And rather than the cloud guys, think about tech companies that sell to large enterprises. Oracle for example. Put Nutanix’ decent product in the hands of Oracle’s sales team and Oracle can instantly claim to be in the cloud game in a big way.

Amazing article with great information to everyone!