Any company making any kind of box – a server, a switch, a storage array – has three battles they need to fight here in 2022, one of which they did not have to worry about very much before the coronavirus pandemic and which is of prime importance these days.

There is always the technical battle of designing a best-of-breed product, and the economical one of selling and supporting it at a good price. But locking down the supply chain – which has parts delays on the order of 52 weeks to 70 weeks right now – while at the same time getting commitments from customers a year or more in advance is the determinant of who will be a winner and who will be a loser in any competitive battle.

The mastery of its supply chain, and the ability to shell out of $2.8 billion in parts commitments, is a differentiator that is allowing Arista Networks to aggressively expand from the core Ethernet datacenter switching market into campus switching, datacenter routing, edge routing and switching, and datacenter interconnect. The commitments from key partners and key suppliers are so good that here in mid-February, Arista Networks is declaring that it will have $3.85 billion in sales in all of 2022, which represents a growth rate of 30.6 percent for the year – and in a networking market that is lucky to grow at maybe 5 percent per year.

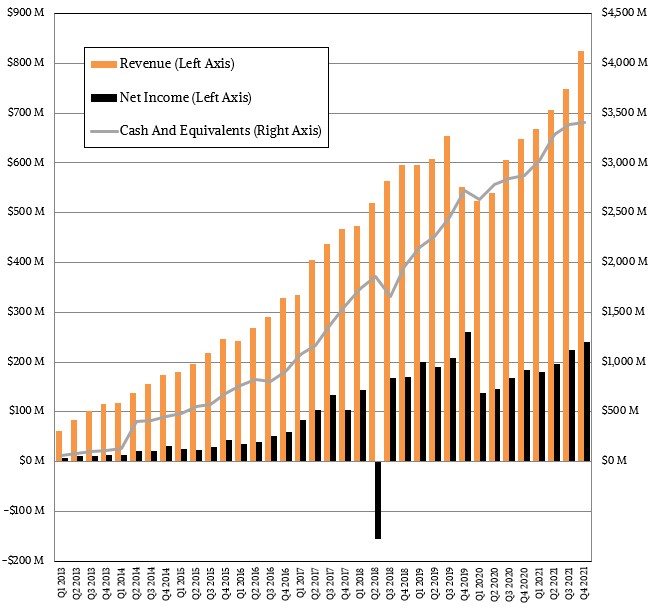

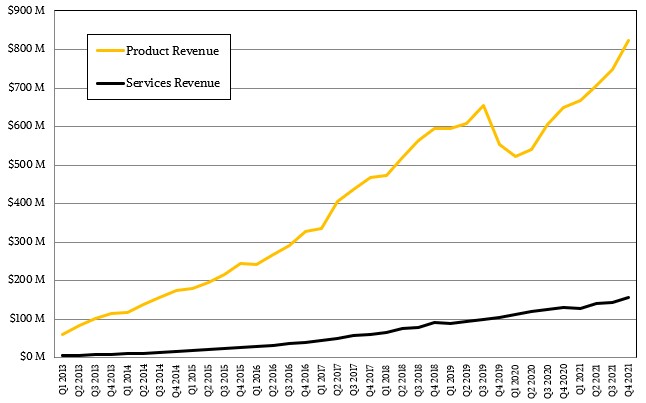

That projection, which we will drill down into in a second, comes after Arista Networks has turned in a very good year, with product revenues up 28.9 percent to $668 million, and services revenues of $156.5 million, up 20.2 percent. Add it up, and total revenues for the quarter were $824.5 million, up 27.1 percent, and $293.3 million dropped to the bottom line, a rise of 30.8 percent. Some of that revenue increase is due to price increases that are passed on, and despite increasing component prices Arista Networks has been able to keep profit growth ahead of revenue growth for all of 2021. (Some might say because of the price increases …)

For the full year, Arista Networks had $2.95 billion in sales, up 27.2 percent, and net income of $841 million, up 32.5 percent, essentially matching the growth rates for product and services for the fourth quarter across the entire year, and leaving the company with a cash pile that is nearly $3.5 billion high – yes, that is close to a year’s worth of forward-looking revenues – sitting in the bank an in investments made on Wall Street.

As you can see in the charts above, the stall in switch and router equipment sales that hit in 2019 and early 2020, which had nothing to do with the coronavirus pandemic but due to a pullback in spending by hyperscalers such as Facebook (now Meta Platforms), which decided to sit out the 200 Gb/sec generation of products in its networks, and to a certain extent Microsoft, which we think has not been cutting spending on switching so much as enjoying the regular cadence of performance doubling in switch and router ASICs from Broadcom.

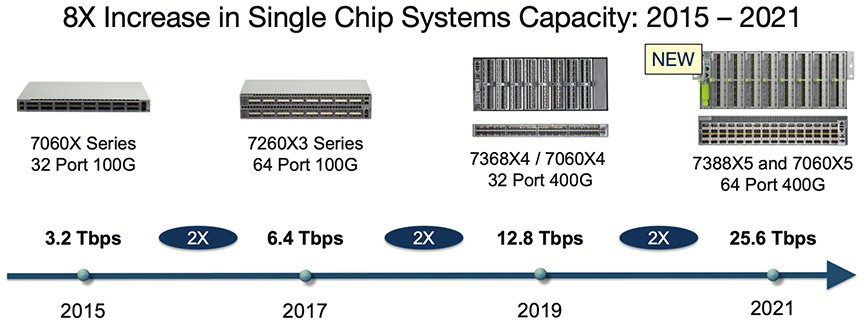

In fact, although Arista Networks doesn’t talk about this, we think a big portion of network revenue is impacted from that doubling of switch and router ASIC capacity.

Each time that happens, it takes one-sixth the number of ASICs to implement a certain number of ports at a high speed. (Inside each switch is a hierarchy of interconnected ASICs that provide non-blocking interconnect for 32, 64, or 128 ports. When a new chip comes out, what used to take six chips in a high density line card now takes one chip, and if datacenter operators keep the port speeds constant – say at 100 Gb/sec – then they can eliminate a lot of layers in their networks to connect 50,000 or 100,000 endpoints together at datacenter scale.

Ditto for single chip fixed port switches, as this chart shows:

With the ASICs on the far right, you can use cable splitters to create a 128-port switch at 200 Gb/sec or a 256-port switch at 100 Gb/sec, all on a single ASIC. Even if the resulting switch costs twice as much, it has four times the port count compared to a 64-port switch from four years ago and that eliminates a whole bunch of switches in a Clos network – as well as some network hops between leaf and spin switches, too, which cuts down on latency.

So hyperscalers and cloud builders have been able to push the price of a port down inside of a switch and also flatten their networks with fewer devices – but the network budget doesn’t compress fully down because datacenter operators build larger and larger networks and spend on datacenter interconnects and routing, too. And they are building more and more datacenters as well as adding regions. Port costs come down and cost per bit shifted comes down, too, but the switches have more ports and the switch cost still goes up a bit. And to grow like Arista Networks is doing, you have to make it up in volume with the existing customers as they build out more datacenters and add more customers as well.

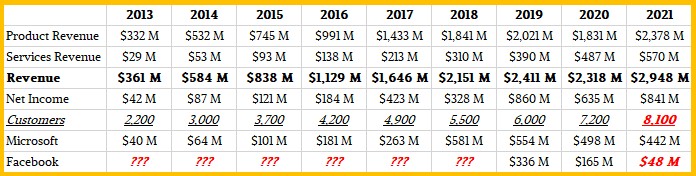

And that has been happening, as you can see in this table:

The move into campus networks and routing has added new customers – about half of the companies investing in these products are new to Arista Networks, according to Jayshree Ullal, chief executive officer of the company, who was speaking to Wall Street analysts about the fourth quarter numbers.

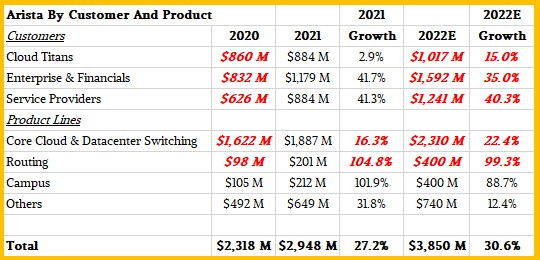

On the call, Ullal provided a little color on some of the financials to give Wall Street a better sense of who is buying and what they are buying at Arista Networks. The characterization for the fourth quarter was not all that useful, but for the full year results it was, and when coupled with the comments that Ullal made a year ago, we can actually start building a pretty good model of revenues by type for Arista. In the call she said that the cloud titans – what we call hyperscalers and cloud – comprised about 30 percent of revenues in 2021, with the combined enterprise and financial sectors comprising around 40 percent, and other service providers about 40 percent.

Microsoft represented 15 percent of revenues in 2021 – SEC rules make it so that any customer representing over 10 percent of revenues has to be disclosed – and according to Ullal, Meta Platforms (mostly Facebook) did not make that cut but would in 2022. Facebook co-designed Arista Networks’ 7388X5 modular switch, which we told you all about back in November. Facebook sat out the 200 Gb/sec generation of Ethernet, but is eager to start rolling out 400 Gb/sec Ethernet, as we explained in detail at the time. That ramp, as well as a similar one at Microsoft, is just beginning. We estimated that Meta Platforms probably accounted for 2 percent of revenues in 2021, and have no idea what it might be before 2019, but there was some sales in there to Facebook. (We saw some of the Arista iron with our own eyes in the North Carolina datacenter back in 2014.)

That table above outlines the past in a broad sense, but given what Arista Networks has said on past calls and shown in past presentations, we have estimated revenues by customer group and by product line. This is a first pass model, with some wide error bars here and there. It would be best if companies just provided such insight and didn’t make us resort to spreadsheet work, but it keeps us off the streets at night. This table is much more interesting in that we are casting it forward into 2022:

The cloud titans put Arista Networks on the map, and now the trickle down of technologies that The Next Platform chronicles time and again is at work as the company’s technologies spread into the enterprise, move deeper into financials, and push out into more service providers. The customer count at Arista Networks is accelerating too, and is now around 8,100 and we think might go up by another 1,000 this year to drive that $3.85 billion revenue target.

Look at that change in campus switching, which we largely don’t care about except that it is almost certainly a more profitable bit of business than sales of switches to hyperscalers and cloud builders – and is derivative to the work Arista Networks was already doing. That business is doubling every year and so is the routing business, which we calculate is about the same size based on what Ullal and Ita Brennan, the company chief financial officer, has said on the current as well as prior calls.

Arista Networks has had its ups and downs, and its trials and tribulations with rival Cisco Systems, over the past decade and more. But it has stuck to its network fabric knitting, gradually expanded its product lines and addressable market, and just keeps eating share. Cisco is fighting back with its Silicon One ASICs, and it will be interesting to see if Arista Networks might some day adopt Cisco’s network ASICs for routers and switches and use them against Cisco in its own gear. Meta Platforms is pitting homegrown switches using Silicon One against co-designed Arista Networks gear based on Broadcom ASICs already, and it is only one small step to have two key ASIC suppliers within Arista Networks. Stranger things have happened, but this would be truly ironic.

Inside The Infrastructure That Microsoft Builds To Run AI

Like the rest of the world, we have been watching Microsoft’s increasing use of foundation models as it transforms its services and software. It is hard to say for sure, but with hundreds of thousands of GPUs deployed across the dozens of regions, Microsoft has probably amassed the largest pool …

Lining Up The “El Capitan” Supercomputer Against The AI Upstarts

The question is no longer whether or not the “El Capitan” supercomputer that has been in the process of being installed at Lawrence Livermore National Laboratory for the past week – with photographic evidence to prove it – will be the most powerful system in the world. The question is …

Upstart Xsight Labs Raises Up The Programmable Switch Banner High

The best minds in networking spent the better part of two decades wrenching the control planes of switches and routers out of network devices and putting them into external controllers. We called this software-defined networking, or SDN, and it gave network operating centers a holistic view of the network and …

Be the first to comment