The gradual trend of IT organizations spending more on dedicated or shared cloud infrastructure than they do on non-cloudy gear continues its inevitable, glacial transformation. But just because cloud is on the rise does not mean that spending on compute and storage to underpin traditional non-cloud systems is always on the decline.

In fact, in the third quarter of 2021, which is the most recent quarter for which the box counters at IDC have compiled data, spending on non-cloud infrastructure actually rose. That spending just did not rise as fast as for gear for cloudy infrastructure, and so the relative market share of non-cloud gear continued its decline.

Which just goes to show that you have to be careful when interpreting selected views of data – meaning, ones that you don’t get to select yourself. IDC changed its way of thinking about cloud and non-cloud last year – it used to look at private cloud, public cloud, and non-cloud as its three categories – but changed it to more accurately reflect the real differences in use cases – cloud and shared, cloud and dedicated, and non-cloud. The former looked at where the iron is located as well as whether or not it was virtualized, while the latter looks at how it is shared or not and whether or not it is virtualized. It is a subtle difference, but perhaps an important one where cloud outposts from the major cloud builders start going into IT organizations and consumption models like Hewlett Packard Enterprise’s GreenLake give customers a cloud-like utility price on gear that HPE retains ownership of and lets them use it wherever they want.

In any event, in the quarter ended in September 2021, non-cloud infrastructure sales rose by 7.3 percent to $14.6 billion, which IDC says was the third consecutive increase in quarterly spending after a period of steady decline that started in Q2 2019 for non-cloud iron.

Spending on shared cloud infrastructure – and let us be very precise here and point out that this is the money that the cloud builders invest to build their infrastructure for shared utilities, not the wholesale or retail revenue generated by these companies as they sell their capacity – rose by 8.6 percent to $13 billion, and that represented a 6.6 percent increase sequentially from Q2 2021. Just to give you a sense of how much of an effect the coronavirus pandemic had on IT spending among cloud builders, in Q2 2020, when the pandemic was really starting to spike demand for services online as many of us all worked and lived inside our homes, spending on infrastructure for shared clouds rose by an amazing 55.1 percent.

Spending on dedicated cloud infrastructure rose by 13.4 percent to $5.6 billion in Q3 2021, and that was the biggest year-over-year increase in spending on this type of gear since Q1 2019. In the September 2021 quarter, 45.5 percent of the dedicated cloud infrastructure purchased was deployed on customer premises, not hosted by a service provider. (We presume this means either a company’s own datacenter or in a co-location facility that they pay for and control access to as if it was their own – at least for the cages where they stuff their racks.)

Add it up, and cloud infrastructure – both dedicated and shared – together comprised $18.6 billion in sales, up 10 percent flat (the IDC figures say it was up 6.6 percent, but that math doesn’t work), after a 1.9 percent decline in Q2 2021 as cloud builders and IT organizations took a break and consumed the capacity they acquired. Across both types of cloud spending, Q2 2020 represented a 38.4 percent rise, which means that spending on dedicated cloud infrastructure did not increase all that much.

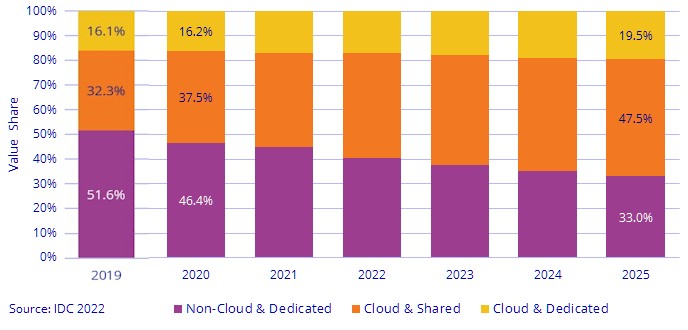

Here’s the trend line and forecast for infrastructure spending across these three broad categories of compute and storage. We tacked on the 2019 data from last year to give you a longer run of data:

Again, this shows the share slices of each category, but it masks whether or not each category is growing or shrinking individually. Sometimes there is shrinkage, and sometimes one category is just losing share because it is growing slower. We prefer the raw data when we can get it, of course.

The forecast at this point for 2021 (which is over but the counting is not) is for spending on infrastructure for dedicated clouds will rise by 10.7 percent to $22.2 billion while spending on infrastructure for shared clouds will grow by 7.2 percent to $49.7 billion. Spending on non-cloud infrastructure will grow by 1.9 percent to $58.4 billion for all of 2021.

If you do the math on that and subtract the first three quarters of 2021 from the 2021 full year forecast, and apply the growth rates above, you can build a full two-year profile from the three statements that IDC has put out so far using this new spending model. Like this:

What sticks out when you do all of this math is that spending on infrastructure for shared clouds cooled off considerably in the fourth quarter of 2020 after what were historical spending binges, and having consumed a lot of the capacity bought in the middle of 2020, the cloud builders and hyperscalers spent a record $14.5 billion on infrastructure, a 44 percent increase according to the forecast put out by IDC. And while non-cloud infrastructure spending is set to increase sequentially to $16.9 billion in Q4 2021, it is apparently not going to be as impressive as the $18 billion spent in Q4 2020.

Datacenter Infrastructure Report Card, Q3 2023

It is hard to keep a model of datacenter infrastructure spending in your head at the same time you want to look at trends in cloud and on-premises spending as well as keep score among the key IT suppliers to figure out who is winning and who is losing. And …

Inside Amazon’s Graviton3 Arm Server Processor

The Graviton family of Arm server chips designed by the Annapurna Labs division of Amazon Web Services is arguably the highest volume Arm server chips the datacenter market today, and they have precisely one – and only one – customer. Well, direct customer. These two facts inform the design choices …

Stacking Up Intel Gaudi Against Nvidia GPUs For AI

Updated: Here is something we don’t see much anymore when it comes to AI systems: list prices for the accelerators and the base motherboards that glue a bunch of them together into a shared compute complex. But at the recent Computex IT conference in Taipei, Taiwan, Intel, which is desperate …

Be the first to comment