Server consumption is a pretty good proxy for how enterprises of all shapes and sizes feel about their particular business. And judging by the number of machines and the aggregate revenue they drove in the third quarter – despite all of the uncertainty in the world – they must be feeling pretty good.

Under normal circumstances, new iron comes in and it gets depreciated according to the prevailing accounting rules on a five year schedule. Sometimes, particularly for big iron NUMA machines that have a long lifespan and a relatively stable workload, the machines are used even beyond their full depreciation date. This was not the case in the early years of big iron, when the compute increases across generations was much smaller in the absolute even if the performance increases were jumping at the rate of Dennard scaling and Moore’s Law. Back then, one or two or three decades ago, system upgrades were more frequent, maybe on a three year span. Now, no one upgrades a system. They just throw it out and throw out the depreciation schedule along with it, writing down the latent value of the machine off their books because they have other more pressing issues, like how to support a billion users. At the major hyperscalers and cloud builders, it is no surprise then that every year they replace about a third of their fleet plus add incremental new capacity to support growing workloads.

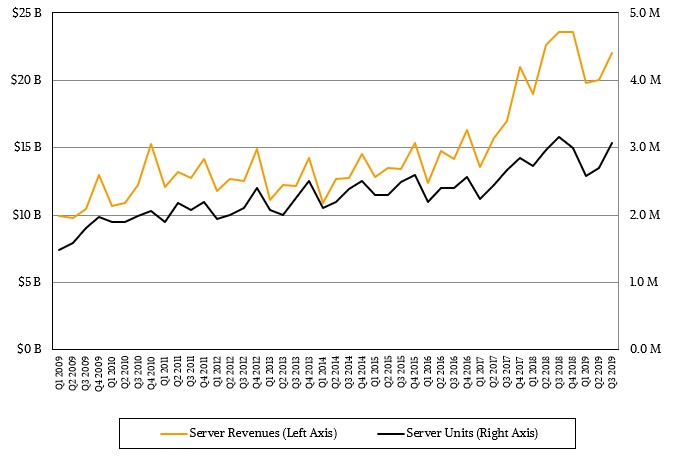

Here’s the funny bit: Even though the server market declined in the third quarter, sales and shipments were up sequentially and has turned in its second best third quarter in history, according to the market researcher IDC, with $21.99 billion in sales and 3.07 million machines shipped here in 2019. That is a 6.7 percent revenue decline against a 3 percent shipment decline, but probably more than half of the revenue decline can be attributed to increasing competition from AMD against Intel in the X86 server market at the same time that prices for main memory and flash have been coming down from ridiculous higher in the past two years. GPU prices have also been dropping as AMD has become more competitive against Nvidia, and that has an effect at the high end of the server market, too, and mitigates against the ever-higher core density that companies want with their systems. What we are saying here is that the compare of Q3 2019 against Q3 2018 is legitimately a very tough compare, and we expect the same thing to happen once again in the fourth quarter of this year. Depending, of course, on the appetite of the Super Eight – Google, Microsoft, Amazon, and Facebook in the United States and Alibaba, Baidu, Tencent, and JD.com in China – and the dozen or so large service providers who operate at megascale but not hyperscale.

It is important to remember that the thousands of large enterprises and tens of thousands of midrange enterprises of the world still represent the bulk of server shipments each quarter and there is no question whatsoever that whatever profits server makers can extract from deals with these enterprises are making up for the lack of profits of machinery sold to hyperscalers and cloud builders.

This is a tough business to be in, and as we have said before, we wish there was more profit in it for those who actually make the systems. But the bulk of the profits are still going to Intel, and it will take years of competition from the AMD and Arm to make a dent here, and it is not like profits will be shifted from Intel to them. It is far more likely that competition will wipe out a lot of that profit pool and no one will get very much when it is all over. This is exactly what happened when proprietary minicomputers came into the datacenter and whacked mainframes in the 1980s, when Unix servers whacked these proprietary machines and mainframes for good measure in the 1990s, and when the tag team of Linux and X86 iron whacked them all in the datacenters in the 2000s. We sure do wish that IDC had a way of tracking the profit in the server racket, but we suspect it would make everyone a little ill if we actually saw it.

The good news is that server makers seem to like building machinery for the up sell and cross sell opportunities, which are profitable. We think it is fine for companies to be in businesses that have razor thin margins – there is no shortage of those. (Publishing, retail, wholesale, the list goes on and on. . . . ) We do not, however, think it is healthy for all the profits to go to one or two vendors.

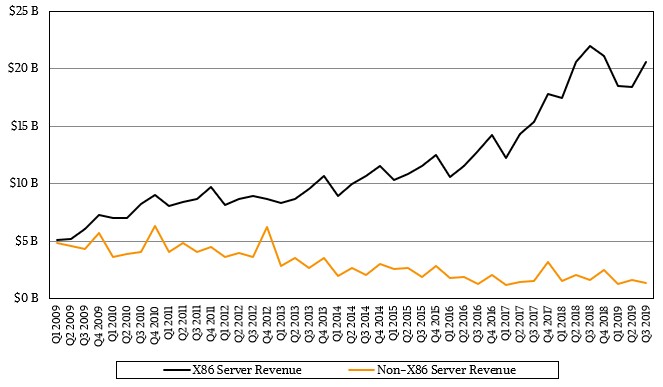

Revenues and shipments are good statistics, but we think we need a better measure of how much compute capacity is being consumed and at what price/performance. Since the X86 server dominates the datacenter almost completely these days, we have extracted the X86 revenues and shipments out and calculated an average selling price. First, just for the sake of illustration of how much the world has changed in the past decade, look at the split between revenues for X86 servers and revenues for non-X86 servers since the Great Recession. This one often gives me pause:

Back in the first quarter of 2009, when the fan was definitely being hit on a global basis, X86 servers comprised a $5 billion market and non-X86 servers also comprised a $5 billion market. Today, the market has expanded by a factor of 2.2X for both revenues and shipments, but non-X86 iron was down to $1.4 billion in the third quarter (a 70 percent contraction) and had shrunk by 13.1 percent on a year-on-year basis compared to Q3 2018. All of the RISC/Unix vendors excepting IBM are pretty much done, and Big Blue is only at the beginning of its next mainframe cycle, which should be pretty good in the fourth quarter.

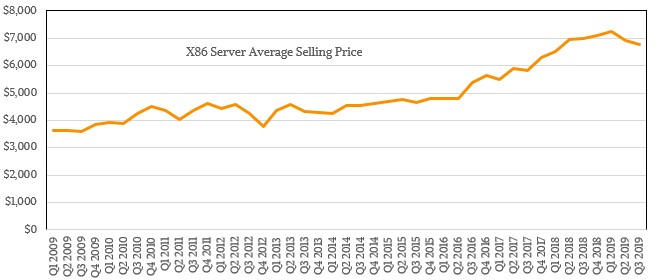

We know X86 server shipments and we know aggregate X86 server revenues, so we can figure out that average selling price:

As you can see, the ASP has indeed been coming down, although not by as much as you might expect. It peaked at $7,236 per machine in the first quarter, a number we have not seen since RISC/Unix machines dominated in the late 1990s and before the rise of X86 iron in the datacenter. Incidentally, the average selling price of all kinds of servers bounced between $5,000 and $6,000 until early 2017, when it also took off as RISC/Unix and mainframe shops mostly had fairly beefy machines and as more and more small and medium businesses started adopting cloud infrastructure – in many cases for software services where they only have a tiny slice of capacity. It would be interesting to see how the aggregate utilization of servers installed has changed over time – our guess is the average utilization has probably doubled or tripled up to somewhere in the range of 25 percent to 30 percent of CPU capacity, and that is because everyone has gotten better at driving the cores hard with virtualization, containers, and other techniques. Our point is this: One of the reasons why server revenues are not higher and vendors are not more profitable is that everyone has gotten better about using the iron they buy.

The converse, by the way, is not true. That doesn’t mean that the world would have consumed $44 billion in machines if they were half as efficient. There is no condition under which there is room in the IT budgets of the world to buy $180 billion in servers alone in a year. People would find ways of getting by without so much computing. Although looking ahead into the post-Moore’s Law future, as CPU cycles will eventually start getting more expensive rather than less so each year, we could see server revenues rise as processor costs rise. It certainly happened with memory and flash, so why not CPUs?

Here is the trend that we find really interesting: The aggregate compute capacity shipped each quarter and the relative cost of that capacity:

There is plenty of witchcraft in these numbers, we would be the first to admit. But we believe the shape reflects the reality of the X86 server market that has dominated in the past decade. This chart takes the number of sockets sold and the average number of cores per socket and the relative performance improvements due to architectural changes with each generation of server and comes up with an aggregate compute capacity relatively performance metric. In this chart, over the past decade, the aggregate amount of compute has grown by a factor of 28X between Q1 2009 and Q3 2019, but the average cost per unit of CPU compute – this is an integer rating, and does not include accelerators – has been decreased by a factor of 12X. This is a stunning demonstration in the power of semiconductor advances, and in this case, almost all of it is Moore’s Law and architectural improvements – Dennard scaling of clocks was already dead before the chart starts.

There are a few things to note in this chart. The first is that, as far as our estimates go, this has been a record quarter for aggregate compute capacity shipped, which is not reflected in the revenue or shipment numbers put out by IDC. We think the aggregate compute capacity shipped went up by 24 percent, in fact, due to a modest increase in instructions per clock and a pretty hefty increase in the average number of cores per socket. Second, we also think that the average cost per unit of compute has gone down by around 25 percent year on year, pitting Q3 2019 against Q3 2018, and that is a huge improvement in bang for the buck. The cost per server figures can’t show you this.

We realize these are just estimates, and we wish that IDC could get us all more accurate figure representing this kind of data. We’re just trying to point the way.

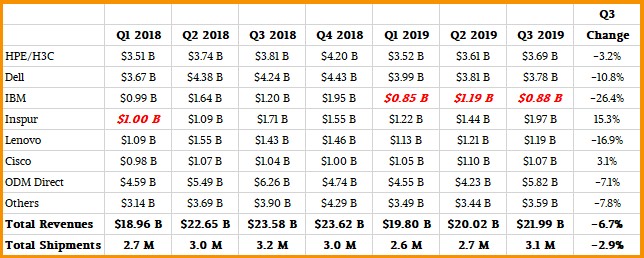

Now, back to the IDC numbers. We all like to keep score on how the vendors are doing, and the ODMs in particular since they are a proxy of sorts for what the hyperscalers and cloud builders are doing. So without further ado, here is the table of the top vendors plus the ODM group:

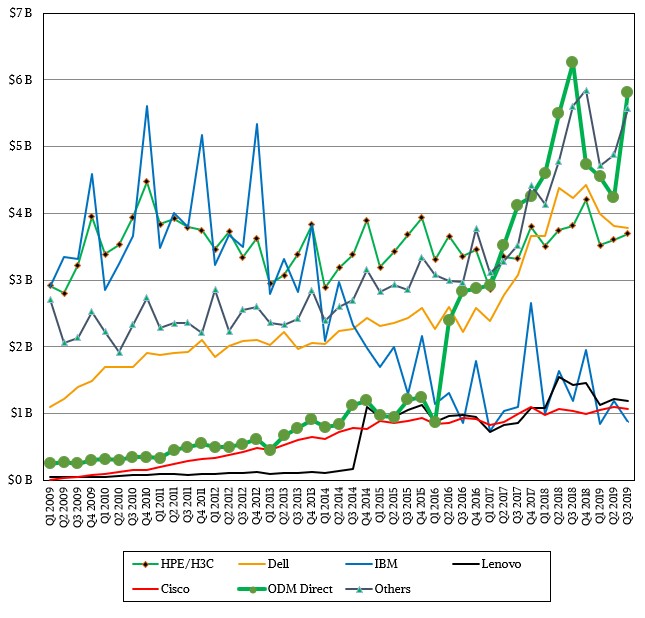

And for those who want to look at the long term data since the Great Recession, here is the larger dataset as a chart:

Dell’s revenues dropped by 10.8 percent, so much so that a declining Hewlett Packard Enterprise almost caught up (and this is obviously without much of a contribution from the new Cray acquisition). Inspur, including its Power systems unit, was the big grower, with sales up 15.3 percent to $1.97 billion. Lenovo and Cisco Systems round out the top five, and Cisco managed to grow its revenues by 3.1 percent as Lenovo declined by 16.9 percent. We have taken the liberty of estimating IBM’s server sales even though it did not make the top five cut and IDC did not talk publicly about how Big Blue was doing.

The ODMs, collectively, accounted for $5.82 billion in sales, or 26.5 percent of total server revenues in the period, the same percentage as they got in the same period a year ago. They had a few points lower share of the server pie in the first half of 2019 and also in the final quarter of 2018, and we suspect this pattern could hold in the final quarter of this year. We shall see.

Gigabyte Spins Off Server Division To Chase Datacenter Business

Gigabyte Technology’s enterprise server division has been spun off under a new logo: Giga Computing. While perhaps best known for its enthusiast, workstation, and gaming motherboard and graphics products, Gigabyte is no stranger to the server and datacenter arena. Alongside consumer-focused boards, Gigabyte also operates as an original design manufacturer …

The Interesting Years Ahead For Servers

By every measure we can get our hands on, 2022 was a bumper year for server shipments and server spending, which is good indicator for the appetite for new kinds of applications and the expansion of existing applications in the world at large. But what is going to happen this …

The Rest Of The World Can Finally Get Sapphire Rapids Xeon SPs

If you are thinking that you are having flashbacks as Intel is launching the “Sapphire Rapids” server CPUs – the company’s fourth generation in the Xeon SP family of server processors – you are not alone. We have been waiting for this launch for the better part of a year, …

Hi,

Thanks for the insight and evidence. Very good read. Would love to see this done for IP switching and routing equipment.