With every new technology that takes off in the IT sector, there is a somewhat predictable curve. The product grows by leaps and bounds in triple digit percentages per quarter, then settles down to triple digit growth year-on-year, and then hits a natural level in the market where it does less than doubling annually, and finally cools down to some natural growth rate, and if all works out and the product is eating market share from rivals, it grows faster than the market.

We say the curve is somewhat predictable because you can never tell how customers will react to new services and how competitors will fight to get a piece of the action. This, among other reasons, is why it is difficult to predict just how large Amazon Web Services will someday be. But just for fun we can bracket the possibilities and ponder the probabilities.

AWS has certainly not shown signs of slowing down, and in fact, its revenues from sales of infrastructure and platform cloud services accelerated in 2015 after a bit of a slowdown in 2014 that was due to a number of different factors, not the least of which was aggressive pricing to keep the heat on the cloud competition from Microsoft and Google and to a lesser extent from IBM, Rackspace Hosting, and a handful of others. Having broken through 1 million customers last year, AWS has not only been able to accelerate its revenue growth but to grow its operating profits at an even faster rate. Thanks to the overhead that all IT suppliers by necessity put into their product and service pricing (mostly due to their sales and delivery model, not because of nefarious purposes), the virtualized IT infrastructure market is a much richer target than generic retail these days for Amazon, which has struggled to turn a profit until AWS hit critical mass. That said, by the time Amazon and its competitors are done fighting over the cloud market some years hence, margins in the cloud could be razor thin, too. In fact, if you were going to guess how Amazon will play this, it will eventually reach a point where it has enough share that it can use low margins to keep competitors out of the market.

Amazon has not taken over the $3.5 trillion online retail world, although it is on its way to breaking $100 billion in revenues this year. At around $3.5 trillion, the IT market is, as we pointed out earlier this month, roughly the same size as the online retail market, and Amazon has aspirations to grow AWS to be as big as Amazon “in the fullness of time,” as senior vice president in charge of AWS Andy Jassy always puts it.

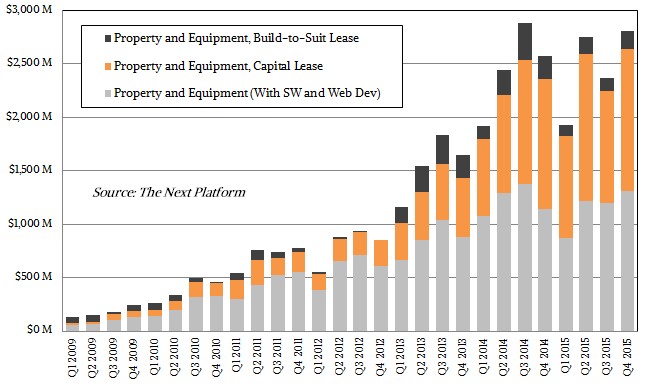

AWS is a great business for Amazon and well worth the massive investments it has taken to create the global IT infrastructure that runs the applications for those more than 1 million customers. Amazon spent very heavily in the past couple of years, doling out around $5 billion for datacenters and gear in 2013, $8.9 billion in 2014, and more than $9 billion last year. Amazon will be firing up five new regions in the near term (it has not said precisely when), with the one in South Korea being formally announced. But a new region does not cost that much, while expanding existing regions where AWS has lots of customers already, who buy more and different services, does.

These datacenter investments amortize over a long haul, but clearly it takes a lot of capital to make a global cloud that scales, and this kind of investment is not something many companies can do. And it is not something you can easily start doing now to try to play catch up.

It took the better part of nine years to reach those first million, and if the history of large markets ripe for upset and being overturned by upstarts is any guide, then the next 1 million customers should take about half as long and, depending on how the competition shakes out and the ever-broadening array of AWS services are deployed by existing customers, revenue could quadruple or quintuple – or explode even higher.

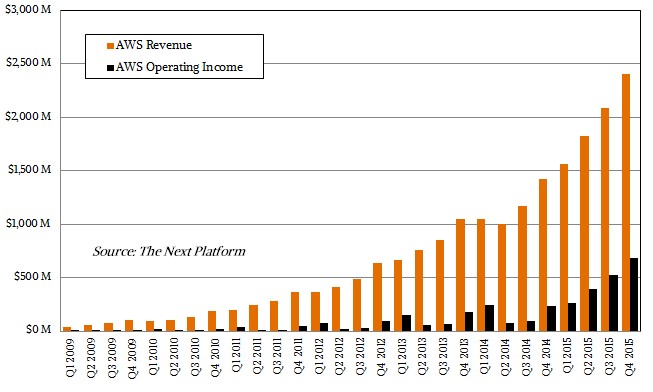

In the fourth quarter of 2015 ended in December, AWS brought in $2.51 billion in revenues, up 69.4 percent, and was able to post an operating profit of $687 million for the quarter. That operating profit was almost triple what AWS did in the final quarter of 2014 and represented 28.6 percent of the revenue – somewhere between the profit margins of an infrastructure hardware maker with skinny margins and a software maker with fatter ones (as you might expect). For the full year, AWS brought in $7.88 billion in revenues, up 69.7 percent, and operating income of $1.86 billion, up a stunning 182 percent year-on year and representing 23.7 percent of revenues.

Since it first came online in March 2006, based on our own estimates as well as recent financial figures supplied by Amazon for AWS, we reckon that the cloud arm of the online retailer has booked $19.8 billion in sales and $1.86 billion in operating profits – and most of that revenue and profit has some in the past two years.

In a conference call going over the financial results for the fourth quarter, Amazon CFO Brian Olsavsky said that the margin improvements for AWS came from a combination of purchase reductions for gear and efficiency gains from driving the assets that the company already has deployed. This is the same struggle that all IT shops face, but the difference is that AWS has some of the best minds on the planet figuring these issues out and it has a scale that allows it – rather than the vendors – to have the upper hand on component pricing for its IT systems. (These same factors hold true for Google and Microsoft, of course.) Another profit driver, oddly enough, is the fact that AWS buys its components in US dollars, but ships them around the world to other regions where this componentry would be more expensive if bought in local currencies. The other chunk of the operating profit increase comes from just driving more business through the Amazon cloud, of course. It is not always the case that a 1.7X jump in revenue will deliver a 2.8X increase in profits, mind you. This is quite an accomplishment.

What we wanted to ponder in analyzing the AWS figures is what the possible futures are for the world’s biggest public cloud in the next decade. There are a number of possible scenarios, and we have ginned up some numbers to present the floor and ceiling for these options as well as what we think are likely scenarios.

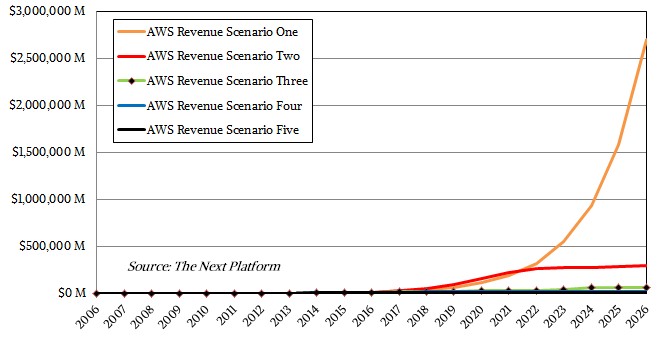

In the chart above, which shows annual AWS revenues from 2006 through 2015 and then forecasts out from 2016 through 2026, you can immediately see the bookends to where AWS can go. These are represented by Scenario One in orange and Scenario Five in black, which simply put, say AWS keeps growing exactly like it did in 2015 at 70 percent per year for the next decade or, conversely, grows a little bit more this year and then hits a wall and grows at the rate of gross domestic product in the Western economies, which we set at 2.5 percent for the fun of it, between 2017 and 2026. That GDP rate is important because enterprise IT spending, which reflects a mature market, tends to follow GDP. Someday, as hard as this is to believe, cloud will be mature and not be explosive anymore in terms of growth.

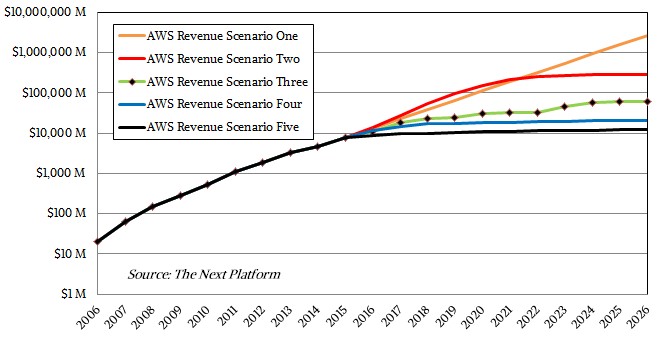

It is hard to see the middle ground scenarios there, so here is the same data presented with a logarithmic scale:

We do not think that either Scenario One or Scenario Five are the likely ones, for a few reasons. First, given that the entire IT community represented $3.5 trillion in spending across hardware, software, and services suppliers – and that key datacenter systems, enterprise software, and IT services represented around $1.39 billion of that according to research by IDC – we do not think that it is possible for Amazon to basically take over the bulk of IT spending in the world. Although we would admit that such a development would radically simplify the supply chain for infrastructure to support applications. Perhaps in a way that would invoke antitrust laws around the globe. The $480 billion in spending in datacenter systems and enterprise software is the pie that AWS can take a big bite out of, and ditto for some IT services, such as systems integration and consulting services that are much less necessary when all you have to do is subscribe to them.

Scenario Five is just plain stupid, we realize, but again, it sets a floor on how low AWS revenues can go. Assuming a mere 10 percent growth in 2016 and 2017, followed by only 5 percent growth in 2018 and 2019, then a dive to that hypothetical 2.5 percent GDP growth rate, AWS will still reach $12.5 billion in sales by 2026. In other words, with this kind of customer base and momentum, something truly awful would have to happen for AWS to lose the steam it has built up. Competitors would have to come up with some new technology and do something very dramatic to steal share and impact the growth at AWS.

Scenarios Two, Three, and Four are far more likely, and as you can see, they all fit within a relatively tight band that puts AWS between a little less than $300 billion and $21 billion within a decade.

With Scenario Two, shown in red, we forecast that AWS actually accelerates a bit from current growth rates before slowing down some and then settling down to that GDP growth rate in 2024. We are not saying that this will happen, except to point out that price cuts and a widening diversity of services plus a growing base can drive more growth – just as it did in 2015. Remember, AWS grew revenues at only 40 percent in 2014.

With Scenario Three, shown in green with the black diamonds, we assume that AWS gets aggressive about price cutting because of competition with Google and Microsoft and growth actually stalls a bit, but picks up again in 2017. Then, as the business reaches its natural – and still by far dominant – share of the cloud market and piece of the overall IT market, growth bounces between 5 percent and 25 percent depending on the stimulus AWS applies to its pricing. This is a kind of wiggle pattern that looks like is emerging from the most recent quarters and years at AWS, but as they say on Wall Street, past performance is not indicative of future performance. Interestingly, this pattern gets Amazon to north of $62 billion in revenues a year – a little smaller than Amazon minus AWS today – without anything looking like too crazy of a growth rate or too high of a slice of the IT market.

With Scenario Four, the growth slows a bit in the coming years and then sets in at that GDP growth rate that enterprise spending tends to track. This puts AWS at $21 billion in revenues by 2026, which on the face of it seems too small.

One thing that these scenarios do not take into account of is what happens during a recession. As we have pointed out many times, recessions tend to accelerate technology transitions if not cause a few of them outright. If we do fall into a global recession, it is far more likely that companies will shed IT gear and cut back on capital expenses for all but the most sentimental applications. This will perhaps bend those curves up some, but AWS could decide at the same time to eat market share to boost its base in the hopes of boosting its revenues down the road.

That is the tricky bit about all of this. AWS has a lot of different levers to pull, and so do the world’s many tens of millions of companies that buy the bulk of IT infrastructure and systems software. One thing that we expect for sure is that the economies of scale and scope that the biggest cloud builders have will make them all that more compelling to some, while others will want private clouds almost regardless of the cost. That latter group will be keen on Microsoft’s Azure Stack in their own shops if Windows Server is their dominant platform and on the combination of OpenStack and Linux if they prefer Linux. (You can support both Linux and Windows Server on either, of course.) What also seems obvious is that AWS is on its way to be a major IT supplier, top to bottom, making money selling its own infrastructure as well as getting a cut of the operating system and application software it sells on its cloud.

Fannie Mae Moves More Mission-Critical Mortgage Work to AWS

Fannie Mae is one of the largest financial institutions in the world with $4.2 trillion in mortgage volume. One-quarter of all single-family homes in the US was purchased or refinanced via Fannie Mae and the company is one the largest financers of the multi-family market. With that said, these mortgages …

AWS Plunks Down $10 Billion For Datacenters In North Carolina

When you drive around the major metropolitan areas of this great country of ours, and indeed in any most of the developed countries at this point, you see two things. One is giant warehouses the size of airplane hangars with zillions of loading bays evenly spaced along the outside. These …

Amazon Gives Anthropic $2.75 Billion So It Can Spend It On AWS XPUs

If Microsoft has the half of OpenAI that didn’t leave, then Amazon and its Amazon Web Services cloud division needs the half of OpenAI that did leave – meaning Anthropic. And that means Amazon needs to pony up a lot more money than Google, which has also invested in Anthropic …

Hi, would you mind sending me your data that you used to make the first chart of AWS revenue and operating margin? Also interested in how you made your interpretation of AWS revenue. Thanks!