The way that systems are being built is changing, and the way that the winners and losers are tracked as they peddle their wares into the datacenter has to change to reflect that. While many companies still buy servers, storage, and switching as separate items, with different teams managing those silos, integrated systems that bring all of these elements together as a single item have taken hold in recent years for specific workloads and certain parts of the market.

Integrated systems are, of course, nothing new, and in fact harken back to the early days of the systems business when, by definition, companies bought products from a single vendor and these were integrated as a matter of course, from hardware all the way up through the systems software stack including operating systems, file systems, databases, and transaction monitors.

The System/360 mainframe from IBM that is now more than five decades old was, using this definition, an integrated system, and indeed, the main frame in the box where the processors were housed was surrounded by other frames of gear that included peripheral controllers and their peripherals, including disk and tape storage, terminals, networking, and other gear that comprised the complete system. The Digital Equipment VAX, the IBM System/36 and AS/400, and the Hewlett-Packard MP3000 were also integrated systems and provided customers with everything they needed to do work. More recently, Oracle’s various engineered systems, most importantly its Exadata database clusters, harkened back to the days of an integrated system, and so did the Unified Computing System from Cisco Systems and its partners. (To our way of thinking, by the way, you could argue that a supercomputing cluster is also a converged system in that it brings together servers, networking, and storage as a single system. But IDC is not including such machines in its converged systems data.)

What is old is new again, and in this particular case, according to statistics from IDC, so-called integrated systems are driving more than $10 billion a year in sales. This in a worldwide systems hardware market that consumes somewhere around $100 billion in server, storage, and switching gear each year. (Roughly speaking, servers account for $50 billion in sales, switching about $25 billion, and storage around $30 billion. There is some double counting between the servers and the storage, which makes it difficult to be precise. And by the way, that is our qualification of raw IDC data, not a precise number from IDC for any given year.) Any portion of the market that has this big of a slice – and that has the potential for growth – is one worth paying attention to.

For the past several years, IDC has been tracking sales of integrated platforms in a certain way, and it is now changing the way it talks about it to reflect new products and conditions. In the past, IDC counted up sales of what it called integrated infrastructure – which meant machines that bring the server, storage, and switching hardware together and aimed at generic workloads – and integrated platforms – which included machines with all of those pieces but aimed at specific jobs like database serving. Those integrated platforms did not include the software stack licenses, which utterly dwarf the hardware prices.

After a rethink, IDC is starting to track converged systems as a general group, distinct from raw servers, storage, and switching sold independently, and is carving this segment up into three broad pieces: integrated systems, certified reference systems, and hyperconverged systems. The integrated systems bring together all of the hardware together (usually from a single vendor), who sells it to the end user customer as a single SKU, while certified reference systems allow for the mixing and matching of different hardware and are generally sold through the channel to end user customers. The nascent – but fast-growing – hyperconverged systems market brings all of the hardware together, but uses the same server nodes to run distributed SAN software as well as offering virtualized compute on those same nodes. The integrated systems and certified reference systems include basic operating system, file system, and systems management software, and the hyperconverged systems include the distributed SAN software. In the latter case, the software represents the lion’s share of the cost of the system, so bear that in mind when you look at the stats.

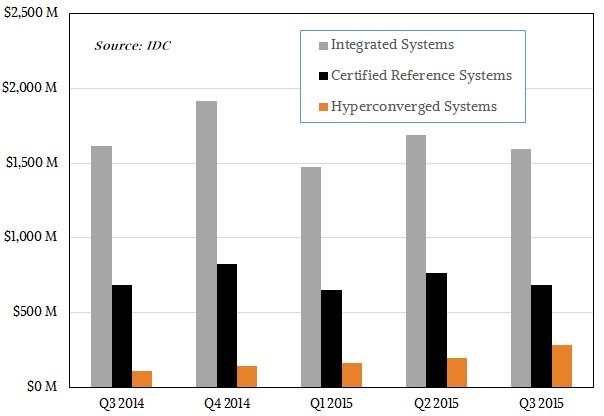

IDC has only released data on five quarters of converged systems sales, but as you can see, integrated systems and certified reference systems are both looking like fairly mature markets in that they are following the traditional seasonality cycle of the IT market overall, where the fourth quarter tends to be the strongest, the first quarter the weakest, and the other two anybody’s guess. That said, Kevin Permutter, senior research analyst for enterprise servers at IDC, tells The Next Platform that this is still a relatively new market and one that is subject to a certain amount of volatility as well as seasonality. IDC has cast its data backwards to categorize the converged systems market and is right now putting together forecasts looking our five years for all three segments and various subsegments including clusters for running databases, Web application servers, VDI, and other enterprise workloads.

Since IT vendors have not reported their financial results for the fourth quarter yet, which just ended a few days ago, the most recent data that IDC can give for the converged systems market is for the third quarter of 2015. In that period, integrated systems accounted for $1.59 billion in sales, down 1.4 percent from the year ago period. VCE, the former “Acadia” partnership between Cisco Systems, EMC, and VMware that initially sold integrated systems based on the UCS blade servers launched by the networking giant in 2009, is now controlled by EMC and is the market leader for integrated systems, with $443.8 million in revenues in the third quarter of last year, up 13 percent year-on-year. (The data initially released by IDC had an error in the VCE numbers, but it has just been corrected this morning.) Hewlett Packard Enterprise was the number two player in integrated systems, with $357.5 million in sales, up 13.8 percent, followed by Oracle, with $339.5 million in revenues, up 8.4 percent. All other vendors accounted for $451.5 million in integrated systems revenues in Q3 2015, and as a group they saw their sales decline by a stunning 24.1 percent. (If you want to know how these players did, you have to pay IDC for the full study.)

Our guess is that sales of integrated systems will fluctuate up and down for vendors and for the market as a whole, much as sales of hyperscale servers and supercomputers jump around depending on the large orders that organizations do. In the trailing twelve months, integrated systems drove $6.67 billion in revenues, which as we pointed out above, is a significant piece of the overall systems market in datacenters. Whether it can grow to be more than that remains to be seen. It all depends on the appetite for integration done by vendors rather than by the IT departments themselves.

The multi-vendor certified reference systems are a smaller portion of the market right now, and have been consistently throughout the period in the data divulged by IDC. Certified reference systems accounted for $683.9 million in sales in the third quarter of 2015, up a mere three-tenths of a point compared to a year ago. The Cisco/NetApp partnership accounted for 44.8 percent of sales, with $309 million in revenues, but only showed 1.2 percent growth. EMC, which is in the process of being taken over by Dell as part of a whopping $67 billion acquisition, was the second largest peddler, with $222.9 million in sales and a 2.7 percent decline. Hitachi ranked third, with $74.4 million and shrank by a half point, and all the other vendors in this part of the converged systems market accounted for only $77.6 million in sales, up 6.9 percent.

The most exciting part of the converged systems arena, that of hyperconverged systems from the likes of Nutanix, VMware, SimpliVity, EMC, Maxta, Pivot3, Scale Computing, and a few others. For now, IDC is just talking about the hyperconverged vendors as a group, but will provide detailed statistics based on vendor and geography in future reports along with forecasts. The hyperconverged market is still in its explosive growth phase, where the integrated systems market was back in 2009 through maybe 2012 when Cisco started off with the UCS iron and IBM, HPE, Dell, Hitachi, and others followed suit.

According to estimates from IDC, hyperconverged systems accounted for $278.8 million in revenues in the third quarter, up 155.3 percent year on year. The growth rate here is accelerating, not declining. In the fourth quarter of last year, sales were up 26.6 percent sequentially compared to the third quarter, and sequential growth was 18.8 percent and 19.5 percent, respectively, for the first and second quarters of 2015. But in the third quarter of 2015, sequential growth shot up to 42.2 percent. The question now is will growth accelerate further in the fourth quarter of 2015, both sequentially and annually? Permutter is tight lipped about forecasting for the hyperconverged space with the IDC forecasts still in the works, but clearly the investment activity in hyperconverged server-storage hybrids has been aggressive and companies are hoping to get a very tidy return on their investments.

Just after The Next Platform went on hiatus for the holidays, the flagship vendor of hyperconverged platforms, Nutanix, filed its S1 form with the SEC to go public. The company has raised $312.2 million in five rounds of venture funding and hopes to raise at least $200 million with its initial public offering, and has an estimated valuation of about $2 billion. Nutanix has 2,100 customers in total, with 226 of them being large installations at Global 2000 companies, and it will be pushing aggressively this year both directly, thanks to the funds raised through the IPO, and through its partnership with Dell, which started in June 2014, and Lenovo, announced last November, to increase its enterprise footprint. While Nutanix has grown fast, with revenues of $30.5 million in its fiscal 2013 year (ended in July) exploding to $241.4 million in its fiscal 2015 year, like most startups its losses have been large. The company lost $44.7 million against that $30.5 million in revenues in fiscal 2013, and closed the gap a bit with only $84 million in losses against $127.1 million in sales in fiscal 2014. Nutanix got closer to the black again in fiscal 2015, with $126.1 million in losses against that $241.4 million in sales.

It could take several years before Nutanix grows its base fast enough to get enough deals to be large and profitable. It took Cisco a few years to build UCS into a multi-billion dollar systems business, and based on current trends, Nutanix could break $1 billion in either 2018 or 2019, and be profitable, too. A lot depends on how much appetite customers have for relatively expensive and closed source distributed SAN software from Nutanix, VMware, and others. If EMC open sources its ScaleIO hyperconverged storage, as it very well could do, and if Dell succeeds in taking over EMC, then a Dell hardware and ScaleIO software combination could take the market by storm and undermine the Dell-Nutanix partnership. Particularly if Dell prices the ScaleIO software much more aggressively than Nutanix does with its Xtreme Computing Platform. Acquisitions have a habit of messing with partnerships, which is how EMC ended up taking over the VCE partnership from Cisco.

The main takeaway here is that as far as converged systems are concerned, it looks like hyperconverged systems are the main growth vehicle going forward. Whether they eat into sales of integrated systems or certified reference systems or into sales of plain vanilla servers, storage, and switching remains to be seen. It will be in the hands of each and every customer to decide.

One last tidbit. Across all three types of converged systems, companies bought a combined 1,261 petabytes of storage in the third quarter, an increase of 34.8 percent compared to the year-ago period. This suggests a few things. First, companies are probably loading up on flash with their hyperconverged setups, which would help drive up revenues at a much faster rate than storage capacity. We also think companies are probably also loading up on compute as they try to get these hyperconverged clusters to do more work.

How Much Can Dell Profit From The AI Wave?

For most of the generative AI revolution thus far, the big original equipment manufacturers, or OEMs, have been sidelined as Nvidia and now AMD have done direct allocations of their GPU compute engines to hyperscalers, cloud builders, and other lighthouse customers. But if the second AI wave is going to …

The University of Michigan Gets Serious About Supercomputing ROI

The University of Michigan is one of the top academic centers in the United States with over $1.5 billion in research expenditures in 2018. From discovering next-generation medical, sustainability, energy, transportation, and other innovations to supporting campus-wide general research efforts, the computational backbone has to be strong, well-organized, high performance, …

Embracing The Inevitable Move From Hardware To Services

When Amazon Web Services, Microsoft Azure, and other hyperscale public cloud providers started becoming a force in IT almost a decade ago, questions arose about what the future looked like for traditional datacenter hardware providers like Dell and Hewlett Packard Enterprise. The response was a sharp shift toward software and …

Be the first to comment