Being in the high performance computing business, as AMD most definitely is, has its ups and downs. Choppiness of revenues and profits was a way of life for Cray and Silicon Graphics as well as for the HPC divisions of IBM, Dell, and Hewlett Packard as well. But a trade war between the US and China has made the situation a bit more turbulent than we might have expected given this, which is evident in the datacenter business for AMD in its second quarter of 2025.

We were on holiday in northern Michigan with the family last week when AMD’s numbers for Q2 came out, and we are going to be playing a little Vacation Ketchup this week.

Perhaps it is a good thing we were on vacation a week ago, given the news that just came out today that both AMD and Nvidia are working out a deal with the Trump administration to hand over 15 percent of their AI chip revenues to the US Treasury in exchange for being able to sell their respective and similarly crippled “Antares” MI308 and “Hopper” H20 GPU accelerators to Chinese customers. Back in April, the Trump administration put these devices under export controls, which had a dramatic effect on datacenter sales for both companies. Nvidia had to write off $5.5 billion in inventory for works in process and AMD wrote off $800 million; sales of these products would have generated multiples of that writeoff over a couple of quarters, we reckon.

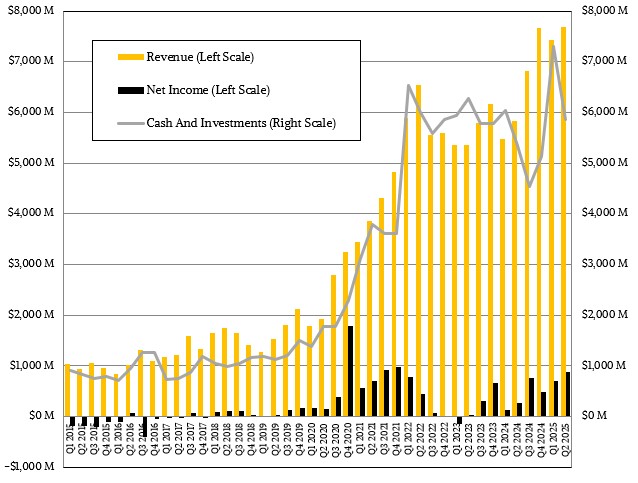

That $800 million writeoff at AMD actually pushed the company’s datacenter business into the red, which is clearly not something that chief executive officer Lisa Su wanted to have happen after working so hard over the past decade to get an Epyc CPU business that can beat Intel’s Xeons and an Instinct GPU business that can stand toe-to-toe with Nvidia.

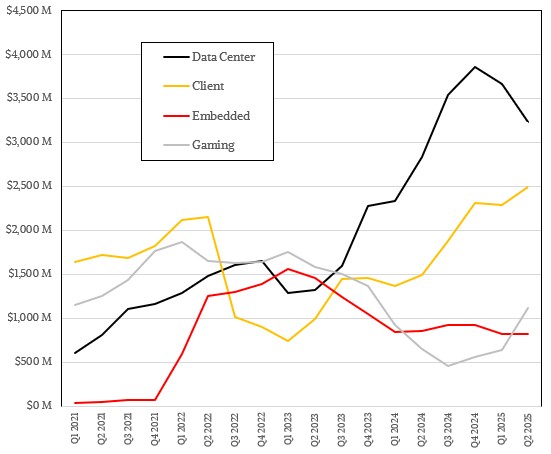

In the second quarter, AMD’s Data Center division had sales of $3.24 billion, up 14.3 percent but down 11.8 percent sequentially from Q1 2025. Without a doubt, the Q2 datacenter business was adversely impacted by the halting of sales of the MI308 GPU into China back in April. It is hard to say by how much because we suspect that Chinese customers were buying so many MI308s in late 2024 and in early 2025 because they knew that the trade war between the world’s two economic superpowers was going to heat up. Demand probably would not have tapered off for MI308s, but maybe it would have.

We will never know, but we will see if MI308 sales pick up again when and if AMD gets its licenses for export from the US Department of Commerce. The bump will be pretty obvious, like GPU sales for cryptocurrency mining a few years back.

The Data Center group had an operating loss of $155 million, and presumably would have had an operating profit of $645 million had it not been for the Chinese MI308 writeoff. That would have still been a 13.2 percent decline in operating income against a 14.3 percent gain in revenue for the Data Center group.

Investing in the future is expensive.

AMD said on the call with Wall Street analysts that the margins for datacenter GPUs are still trending lower than the margins for the company overall. If it were not for an $834 million tax benefit that AMD had in its back pocket for a rainy day, AMD would have been breakeven at best, but thanks to that tax bennie and $104 million in income from discontinued operations (which we presume is from ZT Systems) AMD posted a net income of $872 million in the June quarter.

The past two quarters have been a bit of a bummer for the Data Center group, which is why AMD has not provided guidance on GPU sales for 2025, we think. There are just too many moving parts, with the MI350X and MI355X coming out and, we presume, AMD not being sure how many companies will want to wait for the MI400 series GPUs and their “Helios” rackscale architecture in 2026.

Even with the MI308 woes, the numbers for AMD’s datacenter business were not bad, and Su & Company indicated that they would get a lot better in the second half, which is consistent with the model we did last quarter after the April China bomb dropped and that is almost exactly what happened in the second quarter.

Our model shows AMD did $1.17 billion in datacenter GPU sales in Q2, up 14.2 percent year on year and up a smidgen sequentially thanks to the uptake of the MI350X and the ramp of the MI355X. We are forecasting that AMD will do $1.9 billion in GPU sales in Q3 and another $2.1 billion in Q4, for around $6.3 billion for the year. This does not count any MI308 sales, which could be at least $800 million if AMD can kick its supply chain in gear and get the paperwork with the Trump administration done in a timely fashion. If that happens, AMD will boost GPU sales to $7.1 billion in 2025, up 41.4 percent from the $5.03 billion it sold in 2024. If it takes until Q1 2026 to get MI308s into China and onto the books, then datacenter GPU revenues will rise by 25 percent or so to reach that $6.3 billion level.

We have no problem believing that AMD can sell all of the GPUs it can get HBM memory for, and as far as we are concerned, that is the only practical gating factor to AMD’s business aside from software preferences. (The CUDA-X stack versus the ROCm stack.) All that AMD says is that it believes it can build an AI datacenter business that has “tens of billions of dollars in annual revenue,” as Su put it on the call.

“We are very excited about our next-generation MI400 series, which is another giant step forward on our roadmap and has been designed to deliver leadership performance at the chip, server, and rack levels,” Su explained. “Customer interest for the MI400 series is very strong, and we are actively engaging with an expanding set of customers to support large-scale deployments in 2026. We are in the early stages of an industry-wide AI transformation that will drive a step function increase in compute demand across all of our markets, positioning us for significant revenue and earnings growth over the coming years.”

Our model suggests that AMD sold $1.92 billion in Epyc datacenter CPU sales, and with maybe $95 million in Pensando DPU sales and $55 million in Xilinx datacenter FPGA sales.

If you drill down into the Epyc business, we think that sales of Epyc CPUs to hyperscalers and cloud builders grew by 17.5 percent to just under $1.4 billion, and that enterprises, telcos, service providers, government agencies, and academic institutions accounted for $528 million, up 8.9 percent. All of these segments were down sequentially but up year on year. The CPU business is still a tough one, and Intel is still competing even with one foundry arm tied behind its back. Moreover, there is the ever-present collection of homegrown Arm-based CPUs that are taking server share at the hyperscalers and cloud builders. Just because the server CPU compute pie is growing does not mean the X86 share of it is growing as fast.

Intel Delays “Sapphire Rapids” Server Chips, Confirms HBM Memory Option

It is a relatively quiet International Supercomputing conference on the hardware front, with no new processors or switch ASICs being announced from the usual suspects. While Trish Damkroger, general manager of Intel’s high performance computing division, gave the keynote opening up ISC 2021, providing a little more insight into the …

The Great Danes Get A Supercomputer For AI And Maybe HPC

To AI or to not AI, that is not even a question in 2024. And to need sovereign AI is also not a question. Which is the main reason that we see country after country, and large multinational companies, investing in AI infrastructure in a way that we never did …

The AMD “Aldebaran” GPU That Won Exascale

If you want to know how and why AMD motors have been chosen for so many of the pre-exascale and exascale HPC and AI systems, despite the dominance of Intel in CPUs and the dominance of Nvidia in GPUs, you need look no further for an answer than the new …

from 1.9b to 2.1b into q4 seems quite low given the ramp of mi355x, they announced an oracle 27k ai gpu node with mi355x and epyc turin, that should be about 216k gpus just for oracle alone. So i would assume larger revenue going into q4 and 2026