There has always been a tension in the datacenter between ever-advancing technology and the practical economic gravity of the company balance sheet.

All things being equal, some IT decision makers would be happy for servers to be used until they fail in the field, extending their useful life well beyond their economic life. Technologists, who are always eager to get the shiniest new gear to provide the best platform on which to run the company’s hundreds to thousands of applications and their databases and file systems, would probably prefer to be on a two year cadence that matches the server upgrade cycle at their OEM suppliers.

The correct cadence is somewhere in the middle. And in the past year and a half, with so much of the focus in the datacenter being on accelerated computing and generative AI, less attention has been paid to the much larger fleet of iron that is actually running the businesses of the world. Several million servers across enterprises of all sizes and industries are looking a little bit rusty, and there are several million more that need to be replaced for economic as well as technical reasons.

To take the pulse of the state of datacenter hardware and to try to figure out what the appropriate strategies are for modernizing those core infrastructure systems, we sat down with Robert Hormuth, who is in charge of architecture and strategy for the Data Center Solutions Group at AMD. Like us, Hormuth believes that we are at the cusp of a big upgrade cycle in the datacenter – and that this time, it has nothing at all to do with AI, but rather getting the oldest portions of the server fleet replaced with much more powerful servers – machinery that is much more energy efficient relative to the work it can do.

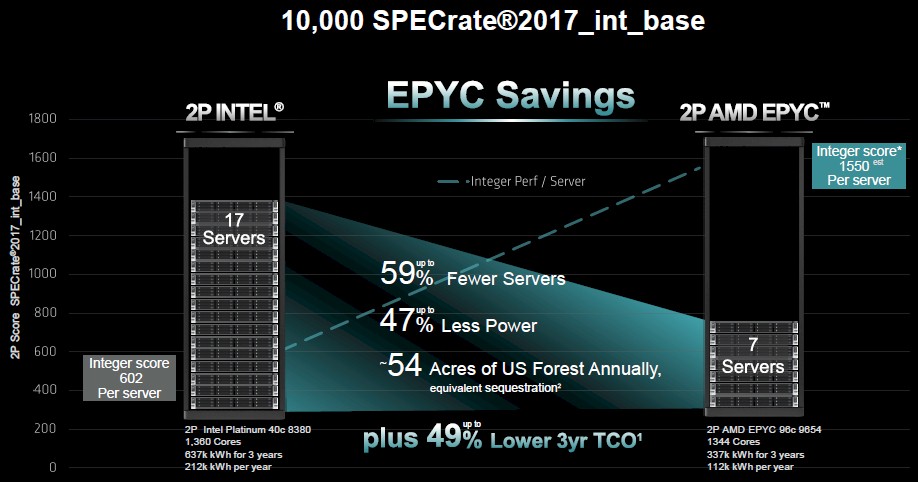

The server consolidation ratios that you can get today by moving to new iron are pretty big, as AMD pointed out in this chart:

Generally, if you compare 4th Gen AMD EPYC CPU-powered servers to even older servers using Intel “Cascade Lake” Xeon 8200s and “Skylake” Xeon 8100s, the server compression ratios can get even higher and the power consumption and TCO gaps can also get even larger. And in Europe, where electricity can be two or three times as expensive as in the United States, it is not hard to get math that shows replacing these older vintage systems will result in the TCO savings actually paying for the new machinery.

To learn more about AMD’s strategy for datacenter modernization, check out the video above.

This Next Platform installment needs some data to spice it up.

Very large installed base of server’s subject upgrade potential albeit the market is segmented by use base and application platform standards in increments of octa cores subject application optimization residing within various performance and price bands.

Xeon v2, v3/v4, Skylake/Cascade Lakes, Ice Lake, Rapids intermediate applied science projects entering Emerald that appears rejected waiting Granite Rapids Intel 3 and let’s see what happens with Sierra Forest.

On the AMD side Epyc Rome price-shopper and the Milan and Genoa and Bergamo primary markets.

Genoa has reached its peak production volume and this analyst expects run down volumes in a supply elastic price slide supporting OEMs offering a commodity enterprise ‘consumer surplus’ meaning channel extended shelf-life parallel Turin massive multi core producer’s ramp.

On platform generations and price bands there is large installed base of v2/v3/v4 if it works don’t fix it.

Skylake and Cascade Lakes price shopper market are similar waiting around for what to upgrade to and then there’s business of compute caught up in the newest platform generations waiting around for a commodity offering with stretch before OEMs will commit to producing large volumes which is the key to the enterprise market server resurgence; economies of manufacturing scale for low cost production.

Servicing end customers on every next producer’s ramp with the latest tech just won’t do on meager economies of production scale tied to every next accelerated platform generation eclipsed by the next meaning there is no stretch just the continuing ‘new applications’ applied computer science project or continued scale out cost optimizing.

The problem with the server market beyond business of compute is there’s no channel shelf life in the newest platform offerings.

Beyond containers and VMs running on massive multi-core the new compute paradigm of accelerated application specific specified workloads remains an applied science project.

VAR and broker serviced the primary candidate for commercial upgrade in relation v4/3/2 if it works don’t fix it low price segment, is Xeon Skylake and Cascades Lakes, the average court count is 13 and cores distribution over the long run;

4C = 7.49%

6C = 4.66%

8C = 22.89%

10C = 9.32%

12C = 14.97%

16C = 10.43%

18C = 6.97%

20C = 5.40%

22C = 1.65%

24C = 4.45%

26C = 1.75%

28C = 5.38%

For the 8/4/2-way split I leave to category;

Platinum = 8.6%

Gold = 57.1%

Silver/Bronze = 34.1%,

XCL U variants barely register

Subject processor workload optimized applications seen in supply it’s less than 28 cores, 32 to 64 cores and 64 cores and above that appears a concentrating platform market on the per-component core increase.

Q; what is AI?

A; to sell more servers

AMD Genoa and Bergamo long run supply the average core count is 60.

128 cores = 6.54%

112 = 2.07%

96 = 23.86%

84 = 3.50%

64 = 14.07%

48 = 6.25%

32 = 25.59%

24 = 8.14%

16 = 9.99%

The variant split;

2P = 65.32%

1P = 15.55% as hard as AMD tries to convince buyers of 1P cost effectiveness

F = 12.86%.

X = 6.27%

Sienna, averaging 7% of Genoa + Bergamo and in the month subject full line;

Sienna = 7.7%

Genoa = 71.1%

Bergamo = 21.2%.

For Milan now a VAR service market the average core count is 38 and 1P = 8.4%.

64C = 49.6%

56C = 7.5%

48C = 5.0%

32C = 15.7%

28C = 3.0%

24C = 10.4%

16C = 7.7%

8C = 0.68%

Rome is the AMD through VAR and secondary price shopper trading market similar legacy v4/3/2 and they’re all trading and still in use for the applications they were designed and optimized for if it works don’t fix it and just add too what you have seems mantra. Rome average core count is 33 and 1P = 15%.

64C = 22.3%

48C = 6.72%

32C = 26.6%

24C = 13.97%

16C = 16.6%

12C = 1.96%

8C = 11.06%

Back to Intel and Emerald Rapids finally fills the channel at sample volume within the last month, the average core count is 32.

64C = 3.64%

60C = 5.47%

56C = 0%

52C = 1.82%

48C = 18.91%

36C = 6.38%

32C = 17.7%

28C = 12.76%

24C = 5.92%

16C = 9.34%

12C = 8.88%

8C = 9.11%

Platinum = 29.8%

Gold = 56% where Intel tends to command 32C and less and AMD 64C and above.

Silver = 14%

Sapphire Rapids who’s trading perked up beginning q1 2024 and the average core count is 28.

Xeon Max in the channel at least, is rejected at 0.34% of all SR server.

60C = 6.49%

56C = 5.15%

52C = 6.53%

48C = 7.04%

44C = 1.03%

40C = 1.02%

36C = 0.83%

32C = 18.02%

28C = 1.82%

24C = 12.76%

20C = 5.12%

18C = 1.27%

16C = 9.13%

12C = 8.19%

10C = 3.24%

8C = 12.37%

Platinum = 33.1%

Gold = 47.1%

Silver/Bronze = 19.6%

Ice lake for its cost of manufacture, XCC/HCC yield hurdle, the LCC P < C slack and 36/32C mishmash of SKUs as the run progressed are trading. Average core count is 24.

40C = 2.22%

38C = 3.28%

36C = 6.76%

32C = 23.13%

28C = 10.25%

26C = 1.98%

24C = 7.34%

22C = 3.33%

20C = 3.69%

18C = 2.90%

16C = 13.99%

12C = 7.09%

10C = 0.26%

8C = 13.78%

Platinum = 29.6%

Gold = 47.1%

Silver/Bronze = 23.1%

Subject the number of servers, for Epyc AMD has produced 26,674,054 components plus whatever sales close incentive call it 30 M / 18 components per rack (you chose) let’s say 1.6 M racks of Epyc servers.

The overall server installed base, 20 M a year that’s an industry joke on all the v2/v3/v4 that escaped out of the back door between 2017 and 2021. Plus the Skylake and Cascade Lakes bundle deal that went unreported. There are easily 5.5 billion components produced back to v2 / by say 18 processors per rack = 305 M racks of servers of all Intel generations.

v2/v3/v4 = 78%

Skylake and Cascade Lakes = 18%

All else = 4%.

The upgrade question is fit for use, applied science projects moving to commodities offering channel shelf life and applications stretch, and competitive price in relation to secondary options and the salvage refurbish price shopper market. if it works don’t fix it?

Mike Bruzzone, Camp Marketing

Thanks, Mike.

Please don’t put auto playing videos in your articles OF ANY KIND!!!

Not my choice.

Good article! I like to sweat the assets but indeed on these high power consumption servers, you can easily save money just through the reduced power consumption.

How many “old” servers are cloud versus premise?

How many premise systems will move to cloud rather than own hardware?

Presume average age of cloud servers is younger than premise systems.

Is there any need to add GPUs to standard servers being bought for either cloud or premise today?

Is it even processors that need upgrading or just replacing any old SSDs or heaven forefend HDDs with newer SSDs/NVM/super-SANs?