With each passing year, the phrase “The network is the computer,” coined in 1984 by John Gage, director of research and co-founder of Sun Microsystems, becomes more and more true. And it was certainly at its most truest in 2022 if you use Ethernet datacenter switching revenues as a gauge.

It has been a bumper year for switch sales, and it is not just the upgrade cycle for high end 200 Gb/sec and 400 Gb/sec Ethernet leaf and spine switches for the hyperscalers and cloud builders that is driving the market. Everybody has a need for more speed, and everybody is finally getting around to swapping out slower-speed devices for faster ones, up and down the span of Ethernet bandwidths.

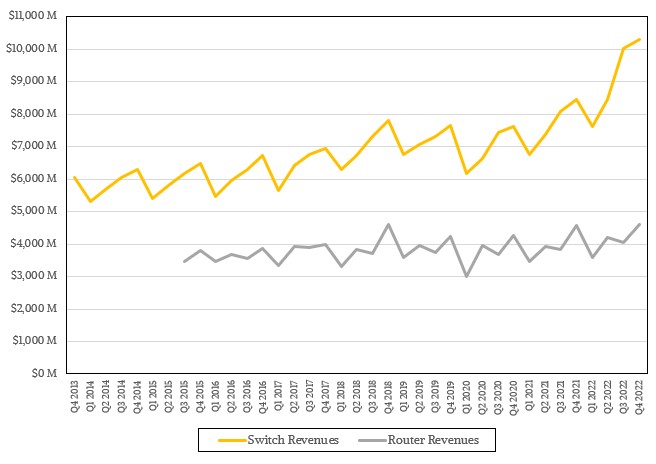

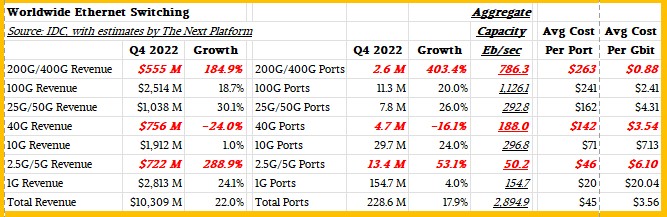

In the fourth quarter of 2022, according to market research performed by IDC, sales of Ethernet switches across all speeds rose by 22 percent to $10.3 billion, and routers pottered along as they have been doing for years, rising by a mere 7/10ths of a point to $4.6 billion worldwide.

We build a complicated model of the Ethernet switching and routing market from the quarterly public statements made by IDC, and as far as we can tell that means somewhere around an aggregate of 227.8 million Ethernet ports shipped in the fourth quarter, up 17.9 percent and comprising a 29.7 percent increase in devices that shipped with 10 Gb/sec or higher speeds.

We used to use 10 Gb/sec and higher networking as a proxy of sorts for datacenter switching investments, but as campus and edge networks are adopting 10 Gb/sec and even faster 100 Gb/sec devices. Luckily, starting a few quarters ago, IDC itself starting breaking out datacenter Ethernet switching sales separate from campus and edge revenues, allowing us to drill down into the datacenter market that is the mission of The Next Platform.

Based on statements from IDC in its quarterly snapshot and the model that we build to fill in the gaps, it looks like the datacenter portion of Ethernet switching revenues came to $4.53 billion, up 21.2 percent and comprising 44 percent of total sales and around 27.3 million ports, up 17.3 percent year on year. The campus and edge portion of the market rose by nearly the same rate at 22.6 percent to $5.78 billion, comprising 56 percent of total sales and driven by 200.6 million ports. The campus and edge market made up 88 percent of ports, compared to 12 percent of ports for the datacenter side of the Ethernet switching house.

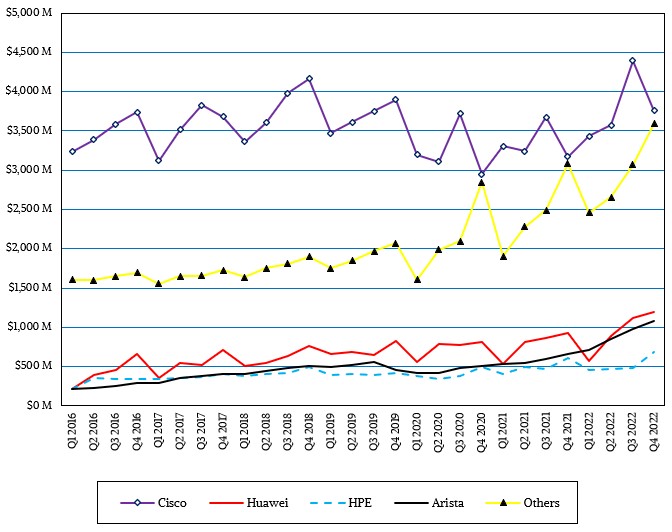

Sales of switches at the high end of the Ethernet bandwidth spectrum – 100 Gb/sec and above – are being driven predominantly by the hyperscalers and cloud builders with contributions from large enterprises and HPC centers whose applications compel them to stay close to the cutting edge of switching.

IDC said that revenues for the combined 200 Gb/sec and 400 Gb/sec segments of the market were only up 7/10ths of a percent sequentially from Q3 2022 but were up by more than a factor of 4X year on year. If you do some math and estimating on what IDC said, you might com up with 200 Gb/sec plus 400 Gb/sec Ethernet switch sales being up by a factor of 2.9X year on year to $555 million, and it will not be long before this category of the market breaks $1 billion a quarter in sales and stays at that level for a few years. The cost of a 200 Gb/sec port has already been halved and 400 Gb/sec ports are also coming down fast, too. On a cost per bit basis, you can’t beat the current crop of 400 Gb/sec Ethernet switches.

Sales of 100 Gb/sec devices got rolling very modestly in the middle of 2015 and broke through $100 million in sales as the 2015 year ended and broke through the $1 billion level three years later as 2018 was coming to a close. For the final two quarters of 2022, they hovered just a smidgen about $2.5 billion with the port counts going up as the cost per port inevitably goers down. At this point, the cost per gigabit on a 100 Gb/sec switch is 2.8X higher than on the blended costs of 200 Gb/sec and 400 Gb/sec ports, and the only reason that companies are even buying 100 Gb/sec devices – as they will do for a very long time – is because the capital outlay is a lot lower.

Sales of 25 Gb/sec and 50 Gb/sec devices, often used in top of rack switches in datacenters, broke above $1 billion in the last two quarters too, as far as we can tell, and we think that is probably the peak as the hyperscalers and cloud builders transition to 100 Gb/sec ports on their servers and 200 Gb/sec and 400 Gb/sec switches in their leaf and spine switches.

Sales of 40 Gb/sec devices seem to be choppy, with a lot sold some quarters and hardly none sold in others as best as we can reckon.

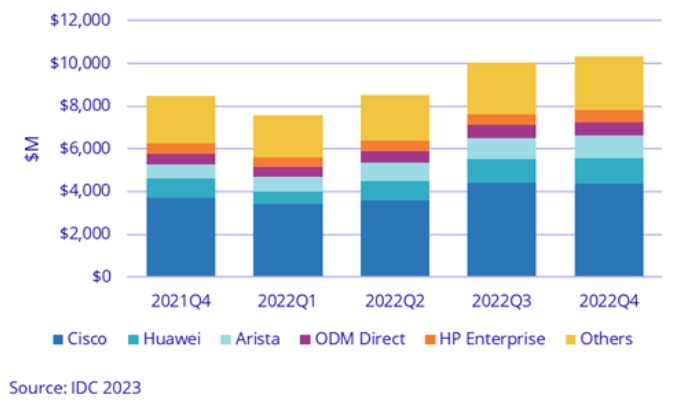

This is the table we really like to make, which brings the Ethernet switching quarter all together in a snapshot:

As usual, the items marked in bold red italics are estimates made by The Next Platform. As you can see, there is an amazing amount of networking capacity sold in a quarter. This Ethernet switching market just keeps climbing up and to the right, driven by competitive pressures brought to bear by the hyperscalers and cloud builders. The result is a tiered switching market that all companies can benefit from as they progress up the bandwidth ladder. But clearly, staying behind, as many companies do for good capital reasons, means paying more per bit shifted.

The Collaboration That Will Drive Ethernet Into The HPC And AI Future

Any time you can get a lot of companies with very technically adept and strongly opinionated people to work together on a problem, or a set of problems, then you know for a fact that there is a real problem. The many problems with Ethernet networking at scale caused the …

Cisco Starts To See Signs Of Datacenter Spending Recovery

If you look at the financial results for Cisco Systems over more than a decade, it is hard to tell one year from the other. The company has gone through many changes as the chief executive officer baton was passed from John Chambers to Chuck Robbins, and in many ways, …

The World Is Still Hungry For Servers – For Now

Two observations. One: When the world goes into recession, the server market has immediately followed. Two: The hyperscalers and cloud builders are big enough that their server spending, or lack thereof, can in and of itself create a server recession even when there is actually not an economic recession. With …

How many of the 100/200 Gbps ports are actually used with 4:1 breakout cables? IE packaging hack to get 25/50 Gbps.

Probably a lot of them.

Tim, knowing the switch data you follow, networks upgrade first, is the transport pipe sufficiently broad to add significant compute through the remainder of the year? Data Center on=line processing / network telecommunications up, flat, down in 2023? Mike Bruzzone, Camp Marketing

Hard to say, isn’t it? A lot of turmoil out there.