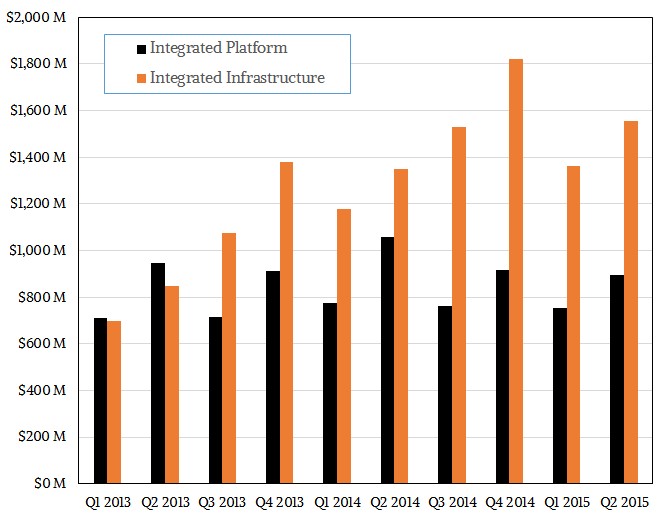

After a boisterous first couple of years when the concept was new, sales of so-called “engineered systems” or integrated platforms, as the box counters at IDC call them, were rising steadily alongside of the adjacent market for converged infrastructure. The integrated platforms are tuned to run specific databases and middleware, while integrated infrastructure is a bit less tuned up even though it does bring together servers, switches, and storage into a single system.

Two years ago, sales of these two types of integrated systems were about the same and both were growing much faster than the independent server, storage, and switching markets at large. But revenues from The Next Platform-style machines have slowed in recent quarters, and were a little in the red ink in the first quarter and went a bit deeper in the second, according to market statistics just released by IDC.

“The next platform market is acting like a mature market now, and is consolidating around the top three players,” Eric Sheppard, storage analyst at the firm, tells The Next Platform. “The growth and decline will tend to follow the market at large among large enterprises.”

In the quarter ended in June, IDC reckons that the world bought $894.8 million worth of these integrated platform systems, which include Oracle’s Exadata, Exalogic, and Exalytic lines, IBM’s PureApp and PureData appliances based on Power-based systems, Hewlett-Packard’s ConvergedSystem setups, Dell’s Active System gear, and a handful of similar stacks. That represented a 15.3 percent revenue decline year-on-year, which is a lot steeper than the 2.5 percent decline these engineered systems saw in the first quarter.

If the third quarter has the same decline as the second and the fourth quarter perks up a bit but is still down, sales of integrated platforms will still probably be north of $3 billion for the year. It is hard to forecast, and in fact, Sheppard says that IDC is working on a forecast right now. In a way, like the HPC and hyperscale markets, the number of deals for engineered systems is so thin that it is highly variable quarter to quarter. This doesn’t mean that the idea of an integrated platform is a bad idea or that some customers don’t want to invest in them. It just means the market will be somewhat volatile because of the nature of processor and storage roadmaps and IT budgets. These are not the kinds of machines that companies buy every quarter, or even every year, although the point is to have them scale out through clustering.

As has been the case since this market started taking off in 2010, Oracle continues to be the revenue leader for integrated platforms, accounting for $482.9 million in sales in the second quarter, down 16.7 percent. IBM’s integrated platform business has been struggling since it sold off its System x server business to Lenovo last October, and now is getting by only on platforms based on its Power Systems. IBM saw its integrated platform sales decline by 32.8 percent to $79.3 million in the second quarter. HP, however, saw a 70.2 percent rise, hitting $30.4 million. All other vendors of such platforms accounted for $302.2 million in the quarter, down 11.3 percent.

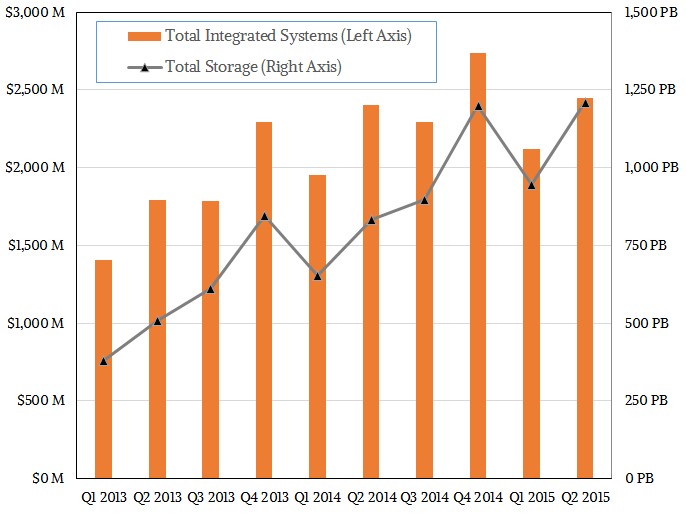

The revenues for integrated platforms were up sequentially by 18.4 percent, and the amount of capacity across all of The Next Platforms sold hit 227 PB in aggregate, according to IDC, up 23.1 percent from the first quarter. (We do not have the data for a year-on-year comparison.)

While integrated platforms are down, integrated infrastructure systems – the name IDC has for things like Cisco Systems’ Unified Computing System and similar converged systems made by Lenovo, Dell, HP, and others – continue to boom and outgrow the overall server and storage markets in terms of revenue growth. In the quarter, sales of these systems reached $1.55 billion, up 15.3 percent. Across all of the integrated infrastructure machines, customers bought 983 petabytes, which was a 29.2 percent sequential increase in storage from the first quarter. That is nearly twice the sequential growth rate of 15.6 percent for sales of integrated infrastructure systems from the first quarter. Storage is growing faster than revenues, which means customers are paying less and less for storage. This is good for the customers, and maybe not so good for the vendors.

Cisco continues to hold the lion’s share of the integrated infrastructure market, thanks to its partnerships with EMC (which now controls the VCE partnership originally set up and run by Cisco, EMC, and VMware) and NetApp. IBM also resells Cisco gear now and is in the others, but ignoring this, Cisco’s UCS machinery drove 67 percent of the revenue for integrated infrastructure machinery in the second quarter of this year.

Assuming that growth rates hold steady for integrated infrastructure systems for the remainder of the year, sales should hit $6.8 billion for this class of machines. That would bring the total integrated systems space to around $9.9 billion this year, which is (very roughly speaking) somewhere around 10 percent of the overall market for servers, storage arrays, and datacenter switches, we estimate. This is a big enough business to matter.

At the moment, IDC is preparing to weave the hyperconverged system market sales into its integrated systems forecast, which is natural enough given that these machines bring together servers, storage, and switching and have a virtual SAN and virtual machine infrastructure as their application. In effect, hyperconverged systems are just a particular style of integrated platform, one aimed at providing a generic platform for running software in virtual machines linked to virtual rather than external physical SANs. It will be interesting to see how IDC maps hyperconverged systems into its models, and get some data on how that explosive market is doing.

Why Did SoftBank Just Buy Ampere Computing?

The world is getting stranger, isn’t it? We understand, given the difficulties of selling Arm server chips to hyperscalers and cloud builders that are also designing and manufacturing their own Arm CPUs, why Ampere Computing, the only successful freestanding Arm server CPU supplier to even get its chips into its …

Cisco Surfs The Liquid Cooling Wave In The Datacenter

High performance systems have a long history of using water cooling, but advancements in semiconductor technology in the 1980s allowed for big iron to have a few decades of using air cooling. With the density of compute, memory, and storage on the rise, it was only a matter of time …

Pandemic Downtime Let Kraft Rebuild The IT Behind Patriots Football

In a lot of ways, the impact of the COVID-19 pandemic on The Kraft Group was no different than most other companies around the world. The organization – a holding company best known for its ownership of the New England Patriots football team and its home field Gillette Stadium – …

Be the first to comment