Did people complain – and by people, we mean Wall Street – as the world’s largest bookseller invested huge amounts of money to transform itself into an alternative to driving to Wal-Mart? Or, better still, did Wall Street complain when that same online retailer, Amazon, started up an IT utility so it could sell that like socks and books and dedicated even more capital to building out a global computing and storage infrastructure?

The honest answer is yes, sometimes Wall Street did. And here we sit in 2025, with Amazon still the heavy weight in both online retailing and cloud computing, with enormous media and advertising businesses that give the company additional and huge revenue streams and the ability to pull different levers in an ever-changing economy as the quarters tick by.

Oracle is similarly diversified across its database, middleware, and application software businesses, and it has become a rising star among the cloud builders because of its unique capabilities in delivering unique and fungible hardware for driving generic and AI compute and the databases that feed into it. But Oracle is different in one important way from Amazon: Oracle’s expected stupendous cloud growth is largely dependent on the ability of one company – OpenAI – to get the money it needs to buy more than a trillion dollars in infrastructure and services wrapped around it.

And that, despite all of the smarts the new Oracle management team has and the calm calculation that Larry Ellison, the company’s co-founder as well as its chief technology officer and chairman, brings to the negotiating table, still has Wall Street worried.

Which is why Clay Magouyrk and Mike Sicilia, the new co-CEOs at Oracle, and Doug Kehring, the new chief financial officer feeding them numbers, spent a lot of time trying to explain during the conference call with Wall Street going over the financials results for the second quarter of fiscal 2026 that while Oracle’s revenue backlog was dominated by OpenAI, if the AI model maker’s plans change, Oracle will still be fine.

Kehring got right into at the top of the Wall Street call:

“The vast majority of our capex investments are for revenue-generating equipment that is going into our datacenters and is not for land, buildings, or power that collectively are covered via leases. Oracle does not pay for these leases until the completed datacenters and accompanying utilities are delivered to us. Rather, the equipment capex is purchased very late in the datacenter production cycle, allowing us to quickly convert cash spent into revenues earned as we provision cloud services to our contracted and committed customers.”

“In terms of funding our growth, there are a variety of sources available to us throughout our debt structure in public bond, bank, and private debt markets. In addition, there are other financing options through customers that may bring their own chips to be installed in our datacenters and suppliers who may lease their chips rather than sell them. Both of these options enable Oracle to synchronize our payments with our receipts and borrow substantially less than most people are modeling. As a foundational principle, we expect and are committed to maintaining our investment-grade debt rating.”

And later in the opening statement, Kehring added this:

“While we continue to experience significant and unprecedented demand for our cloud services, we will pursue further business expansion only when it meets our profitability requirements, and the capital is available on favorable terms.”

Wall Street heard all of that, but still let some of the air out of Oracle’s stock just the same because the company raised its guidance for capital equipment spending for fiscal 2026 by $15 billion as it was able to pull forward some of its backlong, which will add $4 billion earlier in its fiscal 2027 year but not materially change its forecast for revenues for fiscal 2026, which is another way of saying that it is going to take five or six months to get this $15 billion of infrastructure deployed and making money.

The way we do the math, $15 billion in infrastructure capex yielding $4 billion in revenues means it takes nearly four years for it to pay for itself, but in years five, six, and seven, there is revenue to cover power costs and still yield somewhere around $10 billion in operating income. Oracle is committed to 30 percent to 40 percent gross margins for its Oracle Cloud Infrastructure cloud business, and while it looks tight, it is doable. It is hard to say what the operating margins might be, but that is what really counts as far as we are concerned. Both kinds of margins assume, we think, a useful life of seven years for the iron with OpenAI only renting it for five of those years.

If you want to run any business, you have to make assumptions. But the only way to accurately predict the future is to live it, and that is precisely what has Wall Street worried that $300 billion of its $523.3 billion revenue backlog is for OpenAI. The good news is that $223.3 billion of that backlog is not for OpenAI. It is important to remember that.

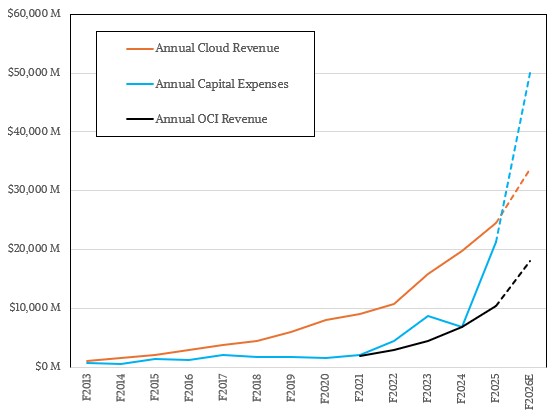

But assuming revenue growth for Oracle’s overall cloud business and the OCI business inside of that goes as we expect, and Oracle keeps investing to support that growth, here is what the plots look like out through the end of fiscal 2026:

That’s pretty severe looking, with Oracle spending $50 billion in capex against what will probably be around $18 billion in OCI revenues and maybe $33.75 billion in overall cloud revenues, which includes hardware and systems and application software sold under cloud pricing models. That is a pretty big gap, $50 billion in capex against $18 billion in cloud infrastructure revenues, and the gap just got a lot larger. But, some of that cloud backlog got pulled in forward as well, and that shifts the larger curve a little:

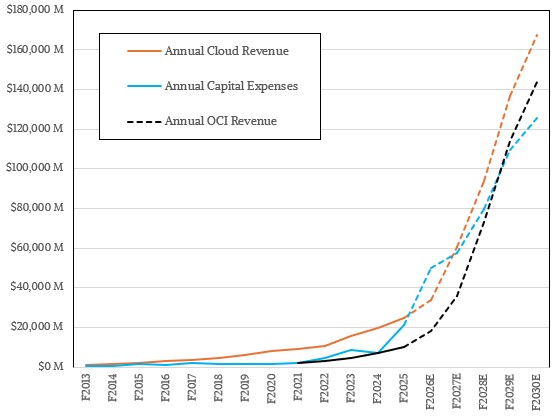

That is our forecast for Oracle capex across all of its customers, not just OpenAI, and where we expect that capex to drive revenues for Oracle overall cloud and OCI infrastructure business. Sometime in late fiscal 2028 or rarely fiscal 2029, Oracle will cross over, making more OCI revenues than it is investing in capex, and by fiscal 2029 it will drive about as much revenues in OCI as AWS is expected to do in calendar 2025. That is a little more than a three year gap in revenue scale for a company that only started to take cloud seriously a few years ago.

It is easy to plot out such lines, but it is hard to actually do the business to make it so. We shall see.

With that, let’s talk about Oracle’s Q2 F2026 in some detail.

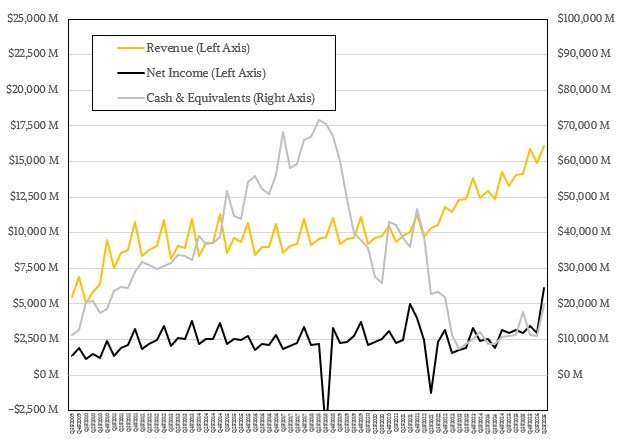

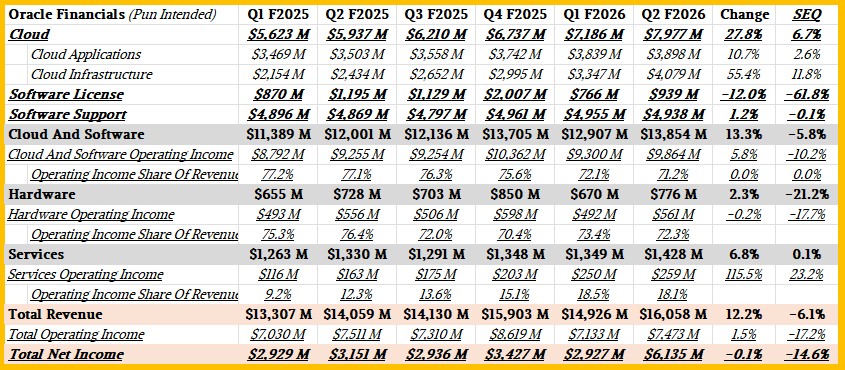

In the quarter, Oracle posted sales of $16.06 billion, up 14.2 percent year on year. Operating income was 4.73 billion, up 12.1 percent. After a $2.7 billion pretax gain on the sale of its 34 percent stake in Ampere Computing to SoftBank, Oracle had a $6.14 billion net income and ended the quarter with $19.77 billion in the bank. The company has $108.1 billion in debt on the balance sheet, which is causing Oracle a certain amount of grief but which is necessary to build out the vast infrastructure that companies like OpenAI want to rent because they can’t afford to buy it.

Aside from the massive debts and the cost of the AI buildout, Wall Street was also annoyed that Oracle missed consensus estimates for growth in the cloud business.

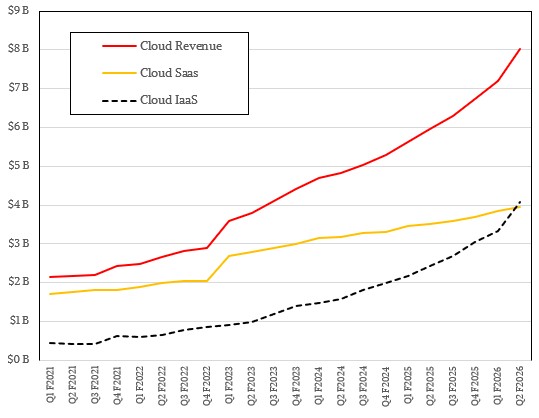

Oracle’s infrastructure cloud business had $4.1 billion in sales, up 68.2 percent year on year and up 21.7 percent sequentially. This seems pretty good for a cloudy HPC-style business with a database and app cloud infrastructure business. Speaking of which, Oracle’s cloud SaaS business – meaning the software it rents on the cloud or for private clouds – accounted for $4 billion in revenues, up 12.9 percent. The rest of the money came from perpetual software licenses and support contracts and professional services.

Here is how it all breaks down over the past six quarters that Oracle has been using this financial presentation:

Looking ahead, Oracle says to expect cloud revenues to grow by 40 percent to 44 percent and overall revenues will grow by 19 percent to 21 percent in fiscal Q3. That’s $19.27 billion in revenues at the midpoint for overall revenues and $11.33 billion for all kinds of cloud sales at the midpoint.

While there is a lot of talk about OpenAI and Oracle’s dependence on it, Ellison has a much bigger target that he is after and is using companies like OpenAI to build out the infrastructure that will support that vision:

“Training AI models on public data is the largest, fastest-growing business in history. AI models reasoning on private data will be an even larger and more valuable business.”

“Oracle databases contain most of the world’s high value private data. Oracle applications also hold huge amounts of exceptionally valuable private data. The Oracle Cloud includes all the top AI models – OpenAI, ChatGPT, xAI Grok, Google Gemini, and Meta Llama. Oracle’s new database and AI data platform, plus the latest versions of Oracle applications enables, all of those AI models to do multistep reasoning on your database and application data while keeping that data private and secure.”

“All our database and application customers want to do this. Because for the first time, they get a unified view of all of their data. AI models can respond to a single inquiry by reasoning across all your databases, all of your applications. By treating all of your data holistically, the combination of AI models plus the Oracle AI database and AI data platform breaks down the walls that isolate and fragment your data. The Oracle AI data platform makes all your data – all your data – accessible to AI models, not just the data in Oracle databases and Oracle applications, but data from other databases, cloud storage from any cloud, even data from your own custom applications are accessible to AI models using the Oracle AI data platform.”

“Using our AI data platform, you can unify all your data and reason on all of your data using the very latest AI models. This is the key to finally unlocking all the value in all your data. Very soon, through the lens of AI, you will be able to see everything happening in your business as it happens.”

Bringing this kind of AI to enterprises may note drive as much revenue as the big AI model builders right now, but we are pretty damned sure that it will for enterprises in the long run – and at a much higher level of profitability to boot.

Oracle Still Hanging In There With Exadata Engineered Systems

It may not seem like it, but Oracle is still in the high-end server business, at least when it comes to big machines running its eponymous relational database. In fact, the company has launched a new generation of Exadata database servers, and the architecture of these machines shows what is …

OpenAI Lays Out The Principles Of Global-Scale Computing

If AI is to become pervasive, as the model builders and datacenter builders who are investing enormous sums of money are clearly banking on it to be, then it really goes have to be a global phenomenon. And as such, it will require global-scale computing that looms much larger than …

Picking Apart AMD’s AI Accelerator Forecasts For Fun And Budgets

Given two endpoints and a compound annual growth rate between those two points over a specific amount of time is not as useful as it seems. Not when you are trying to figure out what is happening at all of the points in between. And that is necessarily so because …

Be the first to comment