IBM is a bit of an enigma these days. It has the art – some would say black magic – of financial engineering down pat, and its system engineering is still quite good. Big Blue talks about all of the right things for modern computing platforms, although it speaks a slightly different dialect because the company still thinks that it is the one setting the pace, and therefore coining the terms, rather than chasing markets that others are blazing. And it just can’t seem to grow revenues, even after tens of billions of dollars in acquisitions and internal investments over the past several years.

IBM has endured 21 straight quarters of revenue declines, and there is no sign that in the next couple of quarters it will see a rebound. If business lines are growing at IBM, there are always others that are shrinking, and by a bit more than the growth. This is no doubt frustrating to IBM’s top brass, who get paid for performance, and its employees, who are under the gun; it is downright depressing for Wall Street and is probably becoming a source of concern for IBM’s hundreds of thousands of enterprise customers around the world.

That said, only a fool counts Big Blue out in the $3 trillion IT market because it has undergone so many transformations in its more than ten decades of existence. And it still employs some of the smartest people in the technology sector and has long, established relationships with some of the most powerful corporations and governments in the world.

It would, however, be good for the company to pick up the pace in its systems business, which has been under pressure as it transitions to new z14 mainframes and Power9 iron, the latter now known as Cognitive Systems and the former, after the announcement last week known as System Z (it has a capital letter now) machines. The System Z mainframe using the z14 processor is an engineering marvel, as usual, and the mainframe is the quintessential I/O engine for enterprise applications (now with encryption embedded at every level). But it looks less and less like the distributed platforms that are by far the norm in the datacenter, and even if the economic and technical arguments can be made in its favor and even with thousands of large enterprises absolutely hooked on this technology, dependent like z/OS and its middleware stack is some kind of drug, the fact is that this is not a growing market, but a shrinking one. Five decades is a great run, and six decades of business is absolutely possible, but at some point, the revenues and profits derived from the IBM mainframe shrink to the point that sustaining the necessary level of investment is not possible. We don’t know where that point is, but we do know that IBM is a hell of a lot closer to it now than it was a decade ago.

The Power architecture was supposed to not only fill in the gap, but also grow so fast that IBM could make up for a declining Unix business as companies move mission critical workloads on relatively big NUMA systems to big X86 NUMA iron or distributed systems on cheaper and smaller X86 NUMA iron, usually running Linux but sometimes also Windows Server. Power has not filled in the gap, even though IBM’s OpenPower alliance has provided an alternative – if perhaps more intellectual than actual – to the Intel Xeon platform for the past several years. Now there is an actual alternative with AMD’s “Naples” Epyc chips, and the case for the future Power9 and Power10 is, by definition, weaker.

The Power9 processors will ship later this year in the “Summit” and “Sierra” supercomputers being built for the US Department of Energy, so technically speaking IBM will have made its promise of delivering these systems on time. But everyone expected for the Power9 systems to be commercially available around the same time that Intel was bringing its “Skylake” Xeons to market here in the summer, and that has not happened. This is not a good thing, particularly as IBM and its partners have been trying to court hyperscalers and HPC centers with the benefits that Power9 provides over Xeons in the datacenter. This has left IBM peddling its Power8 and Power8+ processor against the latest Intel iron. (IBM doesn’t use that latter name, but the chip with NVLink interconnect ports on it, which is very well suited to HPC, deep learning, and database workloads is really a plus chip even if IBM doesn’t want to admit it.)

It would have been better if the Power8+ chip was rearchitected to be a better competitor against the “Haswell” and “Broadwell” Xeons from 2014 and 2016, and that IBM had already built up a base of customers before the Skylake and Naples chips came to market. But that didn’t happen, and Power9 is in fact entering the field late and against some pretty good competition from ARM server chip suppliers Cavium and Qualcomm.

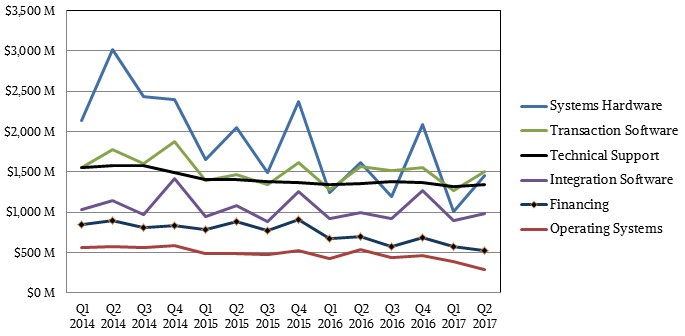

And so, IBM’s hardware revenues decline and they drag down all of the software and services revenues with them. In the second quarter ended in June, IBM’s overall revenues were $19.29 billion, down 4.7 percent, and net income fell by 6.9 percent to $2.33 billion.

The Systems business fell by 10.4 percent to $1.75 billion, with mainframe revenues down but profits up as many customers just activated dormant capacity in their existing machines as they awaited the z14 announcement. IBM chief financial officer Martin Schroeter bragged that IBM has added 91 new mainframe customers since the z13 launch a few years back, but he did not say how many mainframe shops it has lost. (Our guess is more than that.) Power systems sales grew sequentially from the first quarter, but were still down year-on-year as the market awaits Power9 machines. Sales of Power iron based on Power8 and Power8+ processors running Linux grew, and Schroeter says that IBM believes it gained market share in Linux systems. It would almost have to by definition, and by the way, a large portion of the mainframe capacity installed in the world is running Linux, not IBM’s homegrown operating systems of z/OS or z/VM or z/VSE, which are the most vintage platforms still in use today.

The real IBM systems business – including not just servers, operating systems, and storage, but also the middleware, database, and development tools for these platforms – is, as we have always pointed out, much larger than this. But it is still in decline, and that is IBM’s real problem. No amount of chanting Watson will fix that. Getting the Power9 platform into the field this summer, in volume, would have helped. And having it out late last year, as it should have been, would have been even better.