IBM is a bit of an enigma these days. It has the art – some would say black magic – of financial engineering down pat, and its system engineering is still quite good. Big Blue talks about all of the right things for modern computing platforms, although it speaks a slightly different dialect because the company still thinks that it is the one setting the pace, and therefore coining the terms, rather than chasing markets that others are blazing. And it just can’t seem to grow revenues, even after tens of billions of dollars in acquisitions and internal investments over the past several years.

IBM has endured 21 straight quarters of revenue declines, and there is no sign that in the next couple of quarters it will see a rebound. If business lines are growing at IBM, there are always others that are shrinking, and by a bit more than the growth. This is no doubt frustrating to IBM’s top brass, who get paid for performance, and its employees, who are under the gun; it is downright depressing for Wall Street and is probably becoming a source of concern for IBM’s hundreds of thousands of enterprise customers around the world.

That said, only a fool counts Big Blue out in the $3 trillion IT market because it has undergone so many transformations in its more than ten decades of existence. And it still employs some of the smartest people in the technology sector and has long, established relationships with some of the most powerful corporations and governments in the world.

It would, however, be good for the company to pick up the pace in its systems business, which has been under pressure as it transitions to new z14 mainframes and Power9 iron, the latter now known as Cognitive Systems and the former, after the announcement last week known as System Z (it has a capital letter now) machines. The System Z mainframe using the z14 processor is an engineering marvel, as usual, and the mainframe is the quintessential I/O engine for enterprise applications (now with encryption embedded at every level). But it looks less and less like the distributed platforms that are by far the norm in the datacenter, and even if the economic and technical arguments can be made in its favor and even with thousands of large enterprises absolutely hooked on this technology, dependent like z/OS and its middleware stack is some kind of drug, the fact is that this is not a growing market, but a shrinking one. Five decades is a great run, and six decades of business is absolutely possible, but at some point, the revenues and profits derived from the IBM mainframe shrink to the point that sustaining the necessary level of investment is not possible. We don’t know where that point is, but we do know that IBM is a hell of a lot closer to it now than it was a decade ago.

The Power architecture was supposed to not only fill in the gap, but also grow so fast that IBM could make up for a declining Unix business as companies move mission critical workloads on relatively big NUMA systems to big X86 NUMA iron or distributed systems on cheaper and smaller X86 NUMA iron, usually running Linux but sometimes also Windows Server. Power has not filled in the gap, even though IBM’s OpenPower alliance has provided an alternative – if perhaps more intellectual than actual – to the Intel Xeon platform for the past several years. Now there is an actual alternative with AMD’s “Naples” Epyc chips, and the case for the future Power9 and Power10 is, by definition, weaker.

The Power9 processors will ship later this year in the “Summit” and “Sierra” supercomputers being built for the US Department of Energy, so technically speaking IBM will have made its promise of delivering these systems on time. But everyone expected for the Power9 systems to be commercially available around the same time that Intel was bringing its “Skylake” Xeons to market here in the summer, and that has not happened. This is not a good thing, particularly as IBM and its partners have been trying to court hyperscalers and HPC centers with the benefits that Power9 provides over Xeons in the datacenter. This has left IBM peddling its Power8 and Power8+ processor against the latest Intel iron. (IBM doesn’t use that latter name, but the chip with NVLink interconnect ports on it, which is very well suited to HPC, deep learning, and database workloads is really a plus chip even if IBM doesn’t want to admit it.)

It would have been better if the Power8+ chip was rearchitected to be a better competitor against the “Haswell” and “Broadwell” Xeons from 2014 and 2016, and that IBM had already built up a base of customers before the Skylake and Naples chips came to market. But that didn’t happen, and Power9 is in fact entering the field late and against some pretty good competition from ARM server chip suppliers Cavium and Qualcomm.

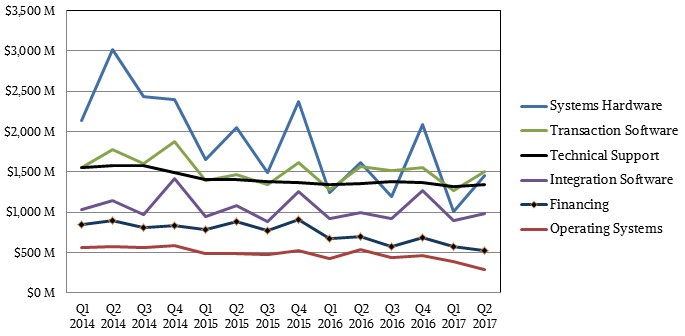

And so, IBM’s hardware revenues decline and they drag down all of the software and services revenues with them. In the second quarter ended in June, IBM’s overall revenues were $19.29 billion, down 4.7 percent, and net income fell by 6.9 percent to $2.33 billion.

The Systems business fell by 10.4 percent to $1.75 billion, with mainframe revenues down but profits up as many customers just activated dormant capacity in their existing machines as they awaited the z14 announcement. IBM chief financial officer Martin Schroeter bragged that IBM has added 91 new mainframe customers since the z13 launch a few years back, but he did not say how many mainframe shops it has lost. (Our guess is more than that.) Power systems sales grew sequentially from the first quarter, but were still down year-on-year as the market awaits Power9 machines. Sales of Power iron based on Power8 and Power8+ processors running Linux grew, and Schroeter says that IBM believes it gained market share in Linux systems. It would almost have to by definition, and by the way, a large portion of the mainframe capacity installed in the world is running Linux, not IBM’s homegrown operating systems of z/OS or z/VM or z/VSE, which are the most vintage platforms still in use today.

The real IBM systems business – including not just servers, operating systems, and storage, but also the middleware, database, and development tools for these platforms – is, as we have always pointed out, much larger than this. But it is still in decline, and that is IBM’s real problem. No amount of chanting Watson will fix that. Getting the Power9 platform into the field this summer, in volume, would have helped. And having it out late last year, as it should have been, would have been even better.

Injecting Machine Learning And Bayesian Optimization Into HPC

No matter what kind of traditional HPC simulation and modeling system you have, no matter what kind of fancy new machine learning AI system you have, IBM has an appliance that it wants to sell you to help make these systems work better – and work better together if you …

Bending The Supercomputing Cost Curve Down

One of the recurring themes at the recent HPC Day event that we hosted ahead of the SC19 supercomputing conference in Denver was that capability class supercomputers are getting more and more expensive. While it is good that these machines can be deployed to run two different kinds of workloads …

IBM Starts Walking The Hybrid Cloud And AI Talking

If Big Blue is going to talk the hybrid cloud and AI talk, as it seems to do incessantly, then the company has to walk it. And perhaps the most interesting thing that was said as part of the company’s discussion of its first quarter 2023 financial results was its …

IBM is going to be toast in the next decade. Watson gamble hasn’t played off as other players have surpassed IBM in the ML/AI sector already. IBM was late to jump on the DNN/RL bandwagon to manifest its position. So IBM no longer is seen as pioneer here.

IBM has also left the FAB business so they have no edge and compete against all the other players out there for capacity on existing FABs. Power architecture looks to me like a dead end it is moving too slow simply as IBM as a whole does.

Their cloud business is also falling behind the other major players by relying too much on their own hardware architecture after selling off the x86 server business

IBM really hasn’t changed much of its mindset which is still based on screwing over their big customers with ludicrious contracts.

Other than that they still can’t make their mind up if they want to be a software, a service or a hardware company. And they failed to install a wide spanding platform outside their core financial and DOW-100 market business.

“Watson gamble hasn’t played off as other players have surpassed IBM in the ML/AI sector already”.

The ML/AL sector is still in it’s infancy and whilst others are still in the proof of concept stage, IBM is out in the market with commercial offerings, with both on and off-premise solutions and have pretty much sewn up the healthcare space, whilst the pretenders are still at the starting gate.

Their health lead will not last very long as they concentrated on the wrong end of the stick (the US health care suppliers) instead of were the real money is the US health insurance. Google with their UK division Deepmind is aggressively going down that path just because there is not much public disclosure and news on this don’t be fooled that they are already way in there.

I’m at a US health insurer, and they’ve been aggressively courting us. We were already doing some work with Truven, and considering Explorys – they purchased both companies.The clinical data model,and EHR integration is a pretty good offering (acquisitions), and their Watson sales team has done a solid job on the senior leadership.

To me it is time to replace the CEO as it has been for a long time. Ginni has always been focused on touting the PWC acquisition but leaving the core of what IBM can do from the System and software side to take a back seat to a vision that has provided little rewards. The systems and software teams have been struggling for years now to get a real leader with a centervision and guts to move the ball forward even though the she can see it in front of her own eyes. Time for Ginni to step down and retire or the IBM major shareholders are just out of their minds. IBM possess a strong brand with really talented people but are being led by a leader who ignores the trends and is unwilling to adapt, a serious flaw for any leader. BIg Blue better make a change or face greater losses. It is a shame Big Blue chose her. I blame Sam for not having the balls to say she was not the right fit. Many saw trhis and brought the concerns up, but they were ignored. Big Blue better get it together.

Shareholders, time to review what your paying for. It does not make sense what Ginni is paid given for the losses in performance. God forbid you continue with this plan with results that lack any merit to the pay she receives and years of losses. Give me a break, wake up and get rid of the dead wood and make a new direction. The results by far do match pay and increases she has received. Thanks, I am a shareholder, but now, I am out. A vote of no confidence is clear and should be rendered.

NVlink is only linked to Nvidia’s proprietary GPU solutions where OpenCAPI can and will be used by AMD/Others that are, along with IBM, founding members of the OpenCAPI Consortium, as well as those that are only associate members of OpenCAPI. The Power9 processor comes in two different designs one SMT4 and the other SMT8. So that SMT4 Power9 design with its top end 24 cores is more inline with some of the larger Intel x86 core SKUs offerings, while the SMT8 12 core design is more similar to the previous power8/8+ generation. IBM has apparently chosen the SMT4 version to go head to head with Intel’s large die 24+core SKUs that only provide SMT2 and many of the server markets workloads are tuned for Intel’s x86 designs more so than IBM’s Power9 designs currently.

AMD’s Epyc platform will offer up some of Intel’s greatest competition in more than a decade and both IBM’s and Intel’s higher margin business models will take a the biggest hit relative to what they both have had in the past decade where high margin Intel only had to compete with high margin IBM in the server hardware market. That little Advanced Micro Devices engineering train has puffed back up that steep engineering gradient and produced a Zen micro-architectural and Modular Zeppelin(Server First) Die design that AMD and its fab partner GlobalFoundries can produce with very high die/wafer yields(Above 80%). And AMD has utilized the vary same Zeppelin die in a scalable fashion to create with ease all of its current Zen based consumer(Ryzen Threadripper) desktop PC as well as Epyc workstation/server SKU market offerings.

AMD’s economy of scale under that very scalable Zen/Modular Zeppelin die can not currently be matched by Big Blue, or Team Blue Intel, who both are currently wedded to their inefficient to produce and lower Wafer/Die yielding large monolithic die CPU designs. AMD has come back from so near to insolvency in a dramatic fashion this time around and is so very lean, out of necessity more than any other managerial reason. And AMD can and will forgo any short term profits for that necessary market share growth over the next few years. That AMD can and will compete with Intel’s best by default means that AMD will also be a pain in IBM’s server market growth ambitions as AMD seeks and obtains more of that Intel x86 market share that IBM was after with its power9 SMT4 design.

Those that also think of only Epyc’s relatively smaller 128 bit AVX instructions as a disadvantage relative to Intel’s larger AVX512 have not taken the time to notice AMD’s GPU accelerator IP that can be brought to task for any heavy duty FP workloads in the HPC market. And those smaller Zen/Epyc AVX units have an advantage for power/die space savings for any server workloads that do not necessarily need AVX 512 ability. So AMD will rely on its GPU/GPU AI IP for any heavily HPC encumbered FP/AI workloads. And AMD’s Infinity Fabric protocol will be spoken across Epyc to any Vega GPU micro-architecture based GPU FP/AI accelerators for a similar to Nvidia’s NVlink functionality via AMD’s fully coherent Infinity Fabric interface CPU to CPU, CPU to GPU and GPU to GPU across all of AMD’s new and future processing products.

AMD’s inter-processor cache coherency takes a hit in the latency metric for that scalability advantage offered but so does Intel’s new Mesh Designs that are also a tradeoff with the cache latency for a more scalable future. But Intel will have to go towards the same smaller modular die designs if Intel wishes to benefit from any the better fabrication die/wafer yields that AMD gets via that Zeppelin Modular die design. IBM is nowhere to be found currently trying to create any designs that will lend themselves to a more affordable fabrication solution. And the market forces are going to be severe towards any and all cost savings as more competition takes its toll on any high margin business models for the server/workstation/HPC markets that will be under the most severe competitive pressures not seen in over a decade, if not ever in these markets.

I thought this blog was about technology, not about opnionated views of a company. Please, explain to us the novelty or the lack of the new z14 or power9 platforms , but not about comoany strategy forecast. Only time will tell.