You can have a strategy, but you can’t buy one.

Nothing illustrates this principle more than the networking buying binges that both Intel and AMD went on nearly a decade ago, which did not really amount to much in the end but which made some sort of sense in the middle of it all happening. Let’s review a bit of extremely relevant history as we ponder the rumors coming out of the Wall Street Journal and Bloomberg that AMD is reportedly in talks to buy FPGA maker Xilinx for a stunning $30 billion.

AMD had some issues in its Opteron server processor line as the Great Recession was starting up, and it lost a key deal to supply supercomputer maker Cray with processors. Seeing the obvious benefits of the Opteron processor and its HyperTransport interconnect, Cray tightly coupled its “SeaStar” and “Gemini” interconnects to the Opteron design. And when AMD was late in delivering several generations of Opteron chips, once because of a bug and once because of issues at process ramps at GlobalFoundries, Cray had second thoughts about this tight coupling between processors and interconnects and backed off to the PCI-Express bus so it could use any processor it wanted in its future “Cascades” systems, which debuted a few years later. Interestingly, Intel essentially mimicked the Opteron design with the “Nehalem” Xeon 5500s launched in March 2009, a little more than a year into the Great Recession, and Cray could have linked to the QuickPath Interconnect that is analogous to AMD’s HyperTransport. But the lesson was learned, and with important ramifications for both AMD and Intel. AMD basically walked away from not only HPC, but servers once the Nehalems took off, and they did mostly because server OEMs and ODMs had only the resources to back one server CPU horse starting in 2009, and that one horse was Xeon.

Then, in early 2012, seeking to find a new niche and a new strategy, AMD caught microserver and interconnect fabric religion at almost exactly the same time that Intel caught HPC interconnect religion because Intel was trying to take on the IBM-Nvidia tag team in accelerated computing. This was right before the GPU-accelerated AI wave really got rolling that would truly change the nature of high performance computing in the most general sense of those words. AI didn’t cause Intel’s strategy, but AI workloads and therefore Intel’s future growth were both positioned to benefit from this focus on the HPC market.

Intel started the networking buying binge, buying low-latency Ethernet switch chip maker Fulcrum Microsystems for an undisclosed amount in July 2011 and then snapping up the InfiniBand networking business of QLogic in January 2012 for $125 million. In April 2012, Intel bought the “Gemini” XT and “Aries” XC supercomputing interconnect businesses from Cray for $140 million, and the QLogic InfiniBand and Cray Aries technologies formed the basis of the Omni-Path interconnect that Intel paired mostly with its “Knights” Xeon Phi parallel processors. As we well know, that did not work out as planned, with the Xeon Phi line discontinued in July 2018 and the Omni-Path networking business, including all of that QLogic and Cray intellectual property, was just last week spun out of Intel into a new company, called Cornelis Networks, founded by people who worked at QLogic and Intel.

In the time between the Intel QLogic and Cray interconnect deals, AMD bought microserver maker SeaMicro in February 2012 for $334 million, which was a lot of money for the company at the time, and did so mostly to get its hands on the “Freedom” 3D torus interconnect and composability middleware that SeaMicro had created to create somewhat malleable microserver systems. This strategy did not coalesce right, and AMD found itself not able to sell the Freedom interconnect to partners alongside its Opteron CPUs and it ended up trying to sell SeaMicro systems against its partners. And so, after Lisa Su took the helm of the company and saw this wasn’t working, AMD wrote the whole thing off in early 2015.

You can have a strategy, but you can’t buy one and you can’t sell one, either. But you can mimic one, perhaps, and we wonder what AMD is seeing in the FPGA market that Intel clearly saw when it shelled out $16.7 billion in June 2015 – more than five years ago, mind you – to acquire FPGA maker Altera.

As readers of The Next Platform know full well, we like FPGAs and we think there are many places where they make sense in the datacenter and at the edge. We question, however, the very nigh price that Intel paid for Altera, which is the main reason that AMD will have to pay even more to buy Xilinx should this deal come to pass. As we talked about several months before the Intel deal to buy Altera went down, which was the same month that The Next Platform itself launched, all we could think was this: Seeing the adoption of SmartNICs at Microsoft based on FPGAs and the performance of FPGAs on machine learning inference, it foresaw a tremendous amount of Xeon compute not going into future datacenters, and it would be better to pay a lot for FPGA compute and preserve at least some of that compute with an Intel brand on it rather than see that money go to a rival.

As it turns out, widespread adoption of FPGAs in the datacenter is yet to be realized, even though there are certainly more FPGA sales into the glass house now than there was five or ten years ago to be sure. Which brings us to the real point we all have to ponder right now: What is AMD seeing in the future that makes it want to buy Xilinx?

There is no reason to question why AMD is considering any acquisition at this moment. By gaining around 10 percent market share in server CPUs with its Epyc processor line, by having a very credible lineup against Intel in PCs, by owning the game console chip business for second generation, and by running the table along with Cray (now a unit of Hewlett Packard Enterprise) on exascale systems in the United States for its CPU-GPU hybrid architecture, AMD is definitely at a local maxima in terms of its perceptions in the market and therefore its market capitalization is huge, even after taking a 4 percent or so hit from rumors of the Xilinx deal. Even with that hit, AMD’s market capitalization is $101.6 billion, a huge increase compared to the low of $1.45 billion set in August 2015, when AMD’s strategy was in question and president and chief executive officer Lisa Su took control and got AMD back on track.

Just like Nvidia is spending mostly newly issue stock to buy Arm Holdings for $40 billion, AMD can spend mostly stock to buy Xilinx. In fact, with only $1.78 billion in the bank in the quarter ended in June, it will have to issue shares to buy Xilinx and that will dilute the value of AMD shares until Wall Street believes. Nvidia’s stock has risen between now and the time it announced the Arm Holdings deal a month ago to cover the stock dilution that will happen should the deal close. AMD could hope for the same, and probably does. It’s all funny money – right up to the moment it isn’t.

Just because things go wrong sometimes does not mean that things can’t go right. It comes down to vision and execution and synergy and resonance with customers. So if Su is indeed leading the charge to have AMD buy Xilinx – and she knows more about the semiconductor business than most people alive at this point – then we take it as a matter of faith that Su is intelligent and sees something important in the future. AMD has CPUs and GPUs, and to complete the set, if that is indeed a goal at all, it needs FPGAs and some kind of neuromorphic device while we are at it. Networking would be good. And that is why we have been suggesting that maybe buying Achronix for FPGAs and Innovium for networking was a good idea for AMD. Start small and innovate fast.

But if AMD is taking a run at Xilinx, and putting $30 billion on the table to scare off potential rivals, then AMD wants something else more than an FPGA business. It wants an ecosystem and a partner channel and a customer base, something that upstarts like Achronix and Innovium have yet to fully develop.

At this point, we should look at the Xilinx business and the AMD business carefully, and because this is The Next Platform, we care about the datacenter and the edge.

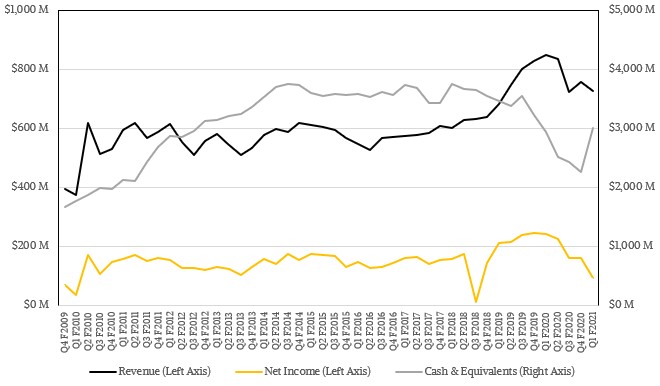

In its most recent quarter ended in June (which is its first quarter of fiscal 2021), Xilinx posted sales of $727 million, down 14.1 percent, and net income of $94 million, down 61.1 percent. The trailing twelve months is probably a better indicator of how Xilinx is doing given the nature of its business, which has its own customer product cycles that have to line up to the Xilinx rollouts, which take a long time. (The FPGA market is slower moving than the server CPU market, even if the FPGAs are on the advanced nodes and can sport the fastest memories and interconnects.) In the trailing twelve months, Xilinx had revenues of $3.04 billion, down 5.7 percent, with net income of $645 million, down 31.5 percent. The company ended the June quarter with a hair under $3 billion in the bank.

As you can see from the chart above, Xilinx has expanded revenues in recent years, but profits did not rise by the same amount because Xilinx is doing more sophisticated devices and coming up against more competition, particularly in the datacenter and at the edge where it has aspirations.

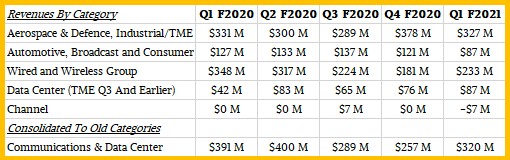

Unlike a lot of chip makers, Xilinx gives great financial, and it actually gives Wall Street a sense of how its different industry sectors are doing and what old and new products are selling and to what degree. The categories have changed a bit over time, but we have normalized them as best we could going all the way back to the Great Recession. This is a summary table of the sales by segment for the past five quarters:

We like data that goes further back than a readable table can show, so here is the same information in a chart going back to 2009:

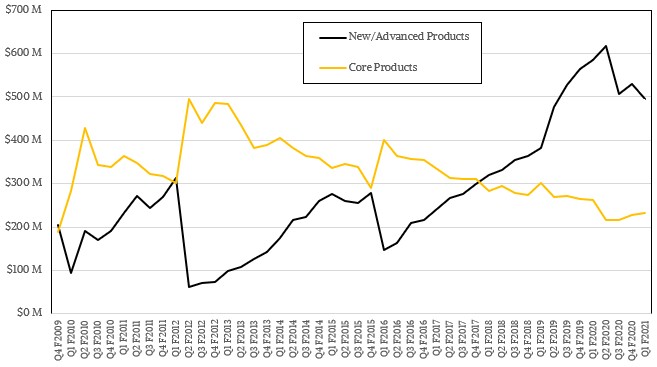

One more chart, and we will talk about them all together. This one shows the sales of core, established products at Xilinx and the new, hot stuff that is fairly recent:

That one is fascinating, and we will start there. Clearly, it takes some time for an FPGA generation to find its footing among Xilinx customers, but in general, they are moving to the newer stuff faster than in the past. It is hard to say what has made the shift, but we think it has a lot to do with the FPGAs being installed at hyperscalers and cloud builders for compute workloads as well as for offload functions for search acceleration and machine learning inference as Microsoft does with its SmartNICs on the Azure cloud and Alibaba does with its own domain specific processors atop FPGAs for inference.

But there is probably more to the shift to newer FPGA iron at Xilinx than just some of the Super 8 doing big rollouts. First, the Vitis environment for programming FPGAs from Xilinx has made it easier to deploy them as industry-specific and application-specific offload engines, and with the slowdown in Moore’s Law, there is greater need to do something. Both the GPU and the FPGA have emerged as a new kind of general-purpose offload engine, and the FPGA is getting its share here.

That said, the datacenter FPGA business at Xilinx is nascent if growing, and we think to make a fair comparison across time you have to roll datacenter and telco/communications into a single customer set. If you do that, then Xilinx had $1.27 billion in sales for the trailing twelve months, but it was down 18.7 percent, and we think largely due to product transitions – customers are absorbing the gradual rollout of the “Everest” Versal FPGAs, which are based on 7 nanometer processes and made by Taiwan Semiconductor Manufacturing Corp.

Now, let’s consider the datacenter business at AMD. In the trailing twelve months, we estimate that AMD had $265 million in GPU sales, down 3.7 percent, and $1.03 billion in CPU sales, up 1.3X; combined, the overall datacenter business was up 79.9 percent in the past year to $1.29 billion. So basically, buying Xilinx allows it to double its datacenter business and grow from there – plus it gets entry into all of those other markets where a CPU or GPU can be sold alongside an FPGA.

While all of this sounds interesting what AMD needs is a coherent software development environment, something that is broader than the Radeon Open Compute (ROCm) hybrid CPU-GPU environment that AMD created several years ago and improved radically in recent years. ROCm now offers a CUDA runtime so applications compiled to offload to Nvidia GPU accelerators can run on hybrid systems using AMD GPUs, and improving this software is a key aspect of the “Frontier” exascale system that AMD is working with HPE/Cray to build for Oak Ridge National Laboratory. But what AMD probably needs if it is indeed going to add Xilinx to its fold is something that looks and smells like Intel’s oneAPI environment, which allows data parallel C++ code to be written once and compiled for CPUs, GPUs, or FPGAs as the system dictates. The Xilinx Vitis environment compiles C and C++ code with OpenCL hooks to communicate to the FPGA accelerator and offload parallel routines to it.

It is not clear how AMD and Xilinx might rectify these programming models, ROCm and Vitis, but what seems clear to us is that the market is not going to have much of an appetite for something we might call twoAPIs. Unless the whole oneAPI approach leads to poorly performing code, of course. And then it is like now: every API for itself. In that case, no one is any worse off than they are today, and the only problem is they are not better off.