The market for servers used to be a lot more predictable in the past, with a portion of the tens millions of companies worldwide buying machinery in their own cycles that more or less coincided with the global gross domestic product. Now, chip makers like Intel are enjoying the benefits of the vast amount of infrastructure investment that hyperscalers and cloud builders are doing, but when they pull back on the reins at the same time that enterprises also take a pause, this causes problems.

It is a good problem to have, especially if you look at how well Intel’s Data Center Group, which makes server processors, chipsets, motherboard, and sometimes systems, did in 2018 – despite a slight downtick in revenues and a flattening of profits in the final quarter of the year. With AMD bringing out its second generation “Rome” Epyc processors within a few months, and the “Cascade Lake” Xeon not generally available to enterprises until the first quarter was over, we were not expecting the first quarter to be a gangbuster one. People want to see what the future holds with the 10 nanometer “Ice Lake” Xeons that the hyperscalers and cloud builders, and perhaps a few HPC centers and large enterprises, will get their hands on before years end and they also want to see how the Rome Epycs will stack up. There are those who are also considering IBM Power9 processors and perhaps an Arm server chip from Ampere or Marvell.

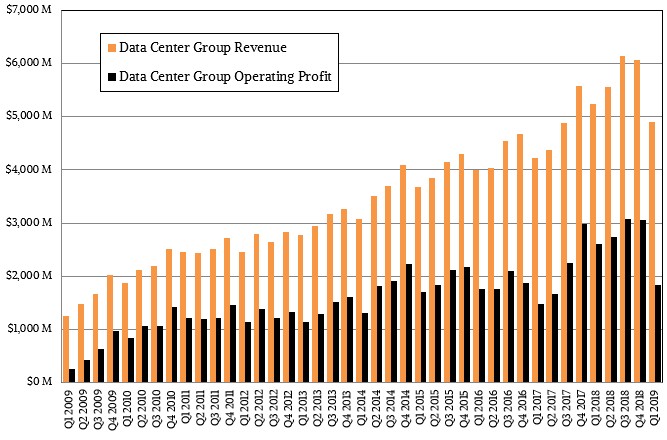

The is the first big decline in quarterly sales that Intel has endured since the first quarter of 2012, and that one was relatively small by comparison. Back then, the market was waiting for the delayed “Sandy Bridge” Xeon E5 processors, which launched on March 6 of that year, with only three weeks left in the quarter, and as now, the market took a pause. In this case, that pause pushed down Intel’s Data Center Group revenues by four-tenths of a percent to $2.45 billion and its operating profit down by 6.5 percent to $1.14 billion. This time around, only seven years later, the hyperscalers and cloud builders have doubled their share of Intel’s datacenter chip pie, and when they slow down, it hits Intel harder. But again, there is so much more money sloshing around that Data Center Group is a lot bigger, at $4.9 billion in sales and $1.84 billion in operating income.

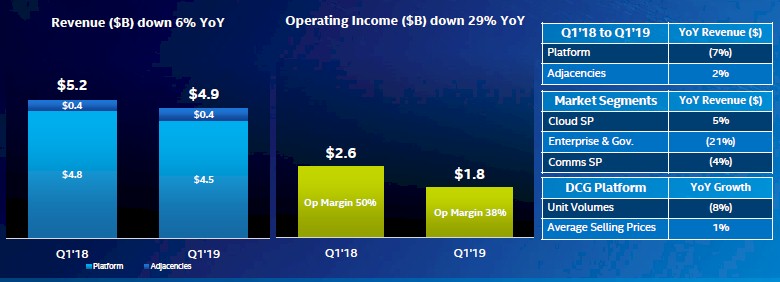

That doesn’t sound too bad until you do the math. In the first quarter of 2019 ended in March, Intel’s Data Center Group saw revenues drop by 6.3 percent – an order and a half magnitude more than back in 2012 with the pause going over Sandy Bridge – and operating income has dropped by a stunning 29.2 percent year on year. This is due to Data Center Group having to pick up some of the development and production costs associated with the 10 nanometer process that will be used to etch Ice Lake chips for clients, servers, and other devices. The clients are expected to get Ice Lake Core processors by the holiday season, and newly appointed chief executive officer Bob Swan, formerly the company’s chief financial officer, said in a conference call with Wall Street analysts last week that the first Ice Lake part would be qualified – meaning tested for commercial readiness – in the second quarter. Swan added that Intel was raising its production goals for its 10 nanometer chips for 2019, which is good news for the company if it can keep up with product demand – something it was not able to do with low-end PC parts at the tail end of the 14 nanometer era that was admittedly prolonged by years because of delays getting 10 nanometer manufacturing up to snuff.

The dip that Intel experienced was not just limited to its Data Center Group. Intel’s flash memory business was also impacted as both DRAM and flash memory prices are starting to come down, as they always do. So the data centric parts of Intel’s business – as opposed to its client centric parts where it sells chippery for desktop and laptop PCs as well as for other kinds of client devices – also took a hit. The situation was not helped by the low-grade trade war going on between the United States and China, which kit revenues across the board at the company.

“Our conversations with customers and partners across our PC and data centric businesses over the past couple of months have made several trends clear,” Swan explained on the call. “The decline in memory pricing has intensified. The datacenter inventory and capacity digestion that we described in January is more pronounced than we expected. And China headwinds have increased, leading to a more cautious IT spending environment. And yet those same customer conversations reinforce our confidence that demand will improve in the second half.”

Drilling down into the results for Data Center Group in the first quarter, volumes across CPUs, chipsets, and everything else Intel counts by units were down 8 percent year on year and off 17 percent sequentially from the fourth quarter of 2018. Intel had a 3 percent sequential decline in shipments the fourth quarter of 2018, but average selling prices were up 2 percent as customers inched up the SKU stack for Xeon processors. That sequential decline was noteworthy, but on an annual basis, unit volumes were up 9 percent and ASPs rose 1 percent, but that growth was less than the general sawtooth trend we have seen for years with Data Center Group.

In the first quarter, sales of core Data Center Group components were off 7.1 percent to $4.48 billion, while adjacent products, such as Ethernet adapter cards, Omni-Path network switches and adapters, silicon photonics, and we presume custom systems, rose by 2.4 percent to $420 million. Add it all up, and Data Center Group had $4.9 billion in sales, and as we already pointed out, off 6.3 percent year on year. Intel’s overall sales were flat at $16.06 billion, operating income was off 6.6 percent to $4.17 billion, and net income dropped by 10.8 percent to $3.97 billion. Just to give you a compared to what.

The drop in spending by enterprises and governments was dramatic. Not quite as bad as the 30 percent to 35 percent power dive we saw during the first few quarters of the Great Recession, but close enough to cause not just eyebrows but more than a few pulses to rise. While hyperscaler and cloud builder revenues – what Intel calls cloud service provider – grew by 5 percent, sales to communications service providers (meaning telecommunications companies and other Internet service providers) fell by 4 percent. Revenues from customers in the enterprise and government sector – meaning everyone that is not a service provider in some fashion, which Intel tracks diligently and thoroughly – fell by 21 percent. Here is to hoping that is not some sort of leading indicator. . . . That would be a bad one. For now, Swan and his team are attributing this to an inventory correction.

In the adjacent markets that are part of the broader data-centric business segments (whose products are aimed at client as well as datacenter devices), sales were mixed. The IoT Group actually grew by 8.3 percent to $910 million with operating profit of $251 million, up 10.6 percent. But the Non-Volatile Storage Group had a 12 percent decline to $915 million, and losses ballooned by a factor of 3.7X to 297 million. The Programmable Solutions Group, which makes FPGAs and related products, posted a 2.4 percent decline in sales, to $486 million and operating profits were off 8.2 percent to $89 million. At least this Altera business has been adding to the middle line for the past four years.

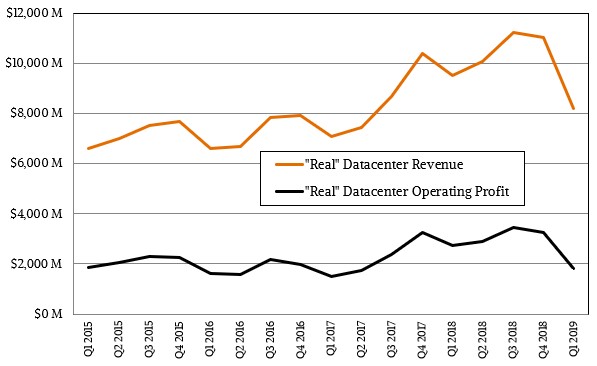

We like to try to suss out what Intel’s so-called “real” datacenter business looks like in terms of revenues and operating profits, and this includes the actual Data Center Group numbers plus the portions of the IoT, NSG, and PSG portions of Intel that we reckon are really going into the datacenter and not into client, mobile, and other devices. We only have data on this going back to 2015 because that was when Intel started providing more granularity on its adjunct businesses. Take a look:

By our estimates, Intel’s real datacenter business was down by 5.9 percent to $6.41 billion, and operating profits were down by 33.6 percent to $1.81 billion. The confluence of the flash downdraft, the 10 nanometer ramp, and the slowdown in chip buying for servers is hitting Intel pretty hard. And the competition has not really ramped up yet from AMD, IBM, Marvell, and Ampere on the server front. That is coming, though.

Looking ahead to the rest of 2019, Swan chopped Intel’s overall revenue projection to $69 billion, a 3 percent decline compared to 2018. The data centric parts of the business, which includes Data Center Group but is not limited to it, are anticipated to shrink in the “low single digits” and Data Center Group down “mid-single digits” year on year. So much for that 15 percent per year growth rate Intel was telling Wall Street only a few years ago. Data Center Group, said Swan, is being pushed down by a tough compare, continued weakness in China, capacity absorption (mainly by hyperscalers and cloud builders), and channel inventory. Swan added that he expected “incrementally more challenging” pricing for flash memory in 2019, too, adding to Intel’s woes.

That canary in the coal mine that is probably going to be fine, unless there is an actual recession. But that pretty little bird is no doubt feeling a little sleepy.